1 Salung – Thailand

Thailand

Context

Years: 1901–1908

Issuer: Thailand

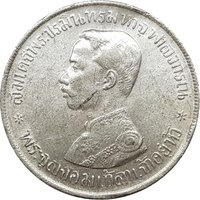

Ruler: Phra Chula Chom Klao

Currency:

(1869—1897)

Subdivision: 1 Salung = ¼ Baht

Demonetized: Yes

Total mintage: 1,360,000

Material

References

Y: #Click to copy to clipboard33a

Numista: #12235

Value

Bullion value: $10.03

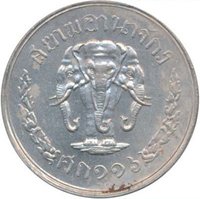

Obverse

Reverse

Edge

Categories

| Symbols> Coat of Arms |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1901 | — | — | ||

| 1902 | — | 560,000 | ||

| 1903 | — | 340,000 | ||

| 1904 | — | 190,000 | ||

| 1906 | — | — | ||

| 1907 | — | — | ||

| 1908 | — | 270,000 |

Historical background

In 1901, Thailand, then known as Siam, operated under a complex and transitional monetary system. The nation was not yet unified under a single national currency, leading to a circulation of diverse mediums of exchange. The primary unit was the baht, a silver bullet coin known as photduang, but its value and physical form were inconsistent. Alongside this, a multitude of foreign silver trade coins, particularly Mexican and later British Trade Dollars, circulated widely, especially in port cities and for international commerce. This created a de facto bimetallic system where both silver and gold (in the form of foreign coins and bullion) were used, with exchange rates fluctuating based on the volatile global silver market.

This monetary fragmentation posed significant challenges to King Chulalongkorn's (Rama V) modernizing agenda. The lack of a standardized, state-issued currency hindered domestic trade, complicated taxation, and was seen as an impediment to asserting full sovereignty and economic control. The falling global price of silver in the late 19th century further destabilized government finances and the value of the silver baht. In response, the government had already taken initial steps toward reform, establishing the first modern mint in 1860 and issuing flat, machine-struck silver coins. However, by 1901, these modern coins coexisted with the older bullet money and foreign coins, indicating an incomplete transition.

Therefore, 1901 represented a critical juncture just before a major monetary revolution. The foundational work for a centralized system was underway, with the government preparing to move decisively. The following year, in 1902, the government would demonetize the old bullet money and foreign coins, and in 1908, it would establish the Currency Act, adopting the tical (baht) as the decimalized national unit and moving the country toward a gold exchange standard. Thus, the currency situation in 1901 was one of lingering tradition amidst deliberate and impending modernization.

This monetary fragmentation posed significant challenges to King Chulalongkorn's (Rama V) modernizing agenda. The lack of a standardized, state-issued currency hindered domestic trade, complicated taxation, and was seen as an impediment to asserting full sovereignty and economic control. The falling global price of silver in the late 19th century further destabilized government finances and the value of the silver baht. In response, the government had already taken initial steps toward reform, establishing the first modern mint in 1860 and issuing flat, machine-struck silver coins. However, by 1901, these modern coins coexisted with the older bullet money and foreign coins, indicating an incomplete transition.

Therefore, 1901 represented a critical juncture just before a major monetary revolution. The foundational work for a centralized system was underway, with the government preparing to move decisively. The following year, in 1902, the government would demonetize the old bullet money and foreign coins, and in 1908, it would establish the Currency Act, adopting the tical (baht) as the decimalized national unit and moving the country toward a gold exchange standard. Thus, the currency situation in 1901 was one of lingering tradition amidst deliberate and impending modernization.

💎 Very Rare