½ Guinea – United Kingdom

United Kingdom

Context

Material

References

KM: #Click to copy to clipboard608

Numista: #13157

Value

Bullion value: $641.94

Obverse

Description:

King George III facing right, legend encircling.

Inscription:

GEORGIVS III DEI GRATIA·

Script: Latin

Engraver: Lewis Pingo

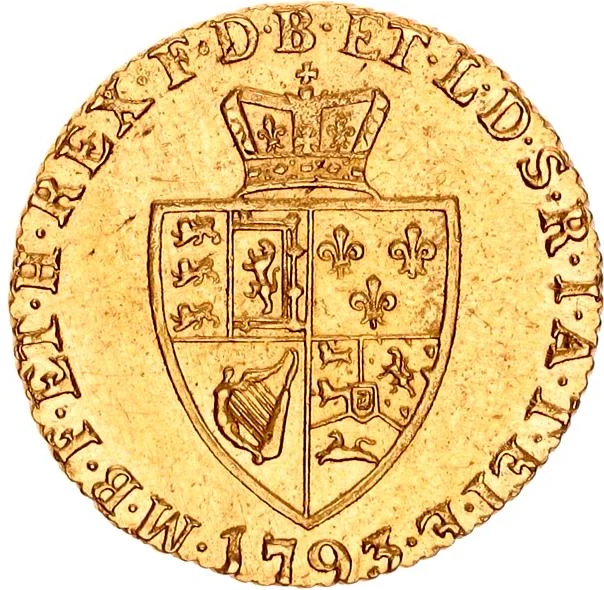

Reverse

Description:

Quartered shield in spade shape, legend around, date below.

Inscription:

·M·B·F·ET·H·REX·F·D·B·ET·L·D·S·R·I·A·T·ET·E·

1793

1793

Script: Latin

Engraver: Lewis Pingo

Edge

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1787 | — | — | ||

| 1787 | — | — | Proof | |

| 1788 | — | — | ||

| 1789 | — | — | ||

| 1790 | — | — | ||

| 1791 | — | — | ||

| 1792 | — | — | ||

| 1793 | — | — | ||

| 1794 | — | — | ||

| 1795 | — | — | ||

| 1796 | — | — | ||

| 1797 | — | — | ||

| 1798 | — | — | ||

| 1800 | — | — |

Historical background

In 1787, the United Kingdom operated under a bimetallic standard, where both gold and silver coins were legal tender. The foundational unit was the pound sterling (£), with the gold guinea, valued at 21 shillings (£1.05), being the dominant high-value coin for major transactions and trade. Smaller denominations, like shillings and pence, were silver, facilitating everyday commerce. However, the system was strained; a fixed legal ratio between gold and silver failed to match fluctuating market values, leading to the gradual disappearance of full-weight silver coins as they were exported for profit, leaving the circulation deficient in small change.

This scarcity of official coinage was a critical economic problem. To bridge the gap, a wide array of unofficial tokens, promissory notes from provincial banks, and worn, clipped, or counterfeit coins circulated alongside the official mint issues. The Royal Mint itself was largely dormant, having struck little new coinage for decades due to outdated practices. Consequently, public confidence in the currency was low, hindering efficient business and wage payments. The situation was particularly acute for the working poor, who struggled to be paid in trustworthy coin for their labour.

The year 1787 fell within a period of mounting pressure for comprehensive reform. While the Great Recoinage of 1816 would ultimately establish the gold standard, the groundwork was being laid. Economists and statesmen, influenced by the recoinage debates following Isaac Newton's tenure as Master of the Mint earlier in the century, increasingly recognised that a reliable, uniform currency was essential for the nation's burgeoning industrial and commercial expansion. Thus, the currency situation in 1787 was one of a fragile and chaotic system on the cusp of being recognised as untenable, setting the stage for the monumental monetary reforms of the following decades.

This scarcity of official coinage was a critical economic problem. To bridge the gap, a wide array of unofficial tokens, promissory notes from provincial banks, and worn, clipped, or counterfeit coins circulated alongside the official mint issues. The Royal Mint itself was largely dormant, having struck little new coinage for decades due to outdated practices. Consequently, public confidence in the currency was low, hindering efficient business and wage payments. The situation was particularly acute for the working poor, who struggled to be paid in trustworthy coin for their labour.

The year 1787 fell within a period of mounting pressure for comprehensive reform. While the Great Recoinage of 1816 would ultimately establish the gold standard, the groundwork was being laid. Economists and statesmen, influenced by the recoinage debates following Isaac Newton's tenure as Master of the Mint earlier in the century, increasingly recognised that a reliable, uniform currency was essential for the nation's burgeoning industrial and commercial expansion. Thus, the currency situation in 1787 was one of a fragile and chaotic system on the cusp of being recognised as untenable, setting the stage for the monumental monetary reforms of the following decades.

⭐ Somewhat Rare