1 dinar – Tunisia

Add to wishlist

Standard circulation coins

Commemoration: FAO

Tunisia

Context

Material

Diameter: 28.06 mm

Weight: 9.85 g

Thickness: 2.08 mm

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #

Numista: #1205

Value

Exchange value: 1 TND

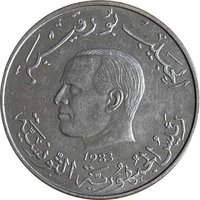

Obverse

Reverse

Description:

Woman in field, text above and below.

Inscription:

البنك المركزي التونسي

ELMEKKI

1

دينار واحد

ELMEKKI

1

دينار واحد

Translation:

Central Bank of Tunisia

ELMEKKI

1

One Dinar

ELMEKKI

1

One Dinar

Language: Arabic

Engraver: Hatim El Mekki

Edge

Plain

Categories

| Agriculture |

| Organization> FAO |

| Map |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1988 | — | — | ||

| 1990 | — | 8,000,000 |

Historical background

In 1988, Tunisia's currency situation was characterized by a tightly controlled and overvalued dinar, managed under a fixed exchange rate regime pegged to a basket of currencies. This system, overseen by the Central Bank of Tunisia, was a legacy of the post-independence statist economic model and aimed to ensure monetary stability and control inflation. However, it created significant distortions. The official exchange rate did not reflect market realities, leading to a thriving black market for foreign currency where the dinar traded at a much weaker rate, highlighting a lack of confidence and a growing imbalance in supply and demand for hard currency.

The overvaluation masked deeper economic troubles, including a persistent and growing current account deficit, declining competitiveness of exports, and a heavy reliance on foreign borrowing. The economy was struggling under the weight of inefficient state-owned enterprises and falling prices for key exports like phosphates and oil. Consequently, foreign exchange reserves were under pressure, limiting the government's ability to finance imports and service its external debt. This precarious position was unsustainable and signaled the need for structural adjustment.

Recognizing these crises, the government of President Zine El Abidine Ben Ali, who had taken power the previous year, began to chart a new course. While major currency liberalization would come later in the 1990s, 1988 was a pivotal year of transition. It set the stage for negotiations with the International Monetary Fund (IMF), which would culminate in a 1989 agreement. This agreement laid the groundwork for a structural adjustment program that included a commitment to eventual dinar convertibility and a move toward a more flexible exchange rate, marking the beginning of Tunisia's shift away from a rigid, state-controlled financial system.

The overvaluation masked deeper economic troubles, including a persistent and growing current account deficit, declining competitiveness of exports, and a heavy reliance on foreign borrowing. The economy was struggling under the weight of inefficient state-owned enterprises and falling prices for key exports like phosphates and oil. Consequently, foreign exchange reserves were under pressure, limiting the government's ability to finance imports and service its external debt. This precarious position was unsustainable and signaled the need for structural adjustment.

Recognizing these crises, the government of President Zine El Abidine Ben Ali, who had taken power the previous year, began to chart a new course. While major currency liberalization would come later in the 1990s, 1988 was a pivotal year of transition. It set the stage for negotiations with the International Monetary Fund (IMF), which would culminate in a 1989 agreement. This agreement laid the groundwork for a structural adjustment program that included a commitment to eventual dinar convertibility and a move toward a more flexible exchange rate, marking the beginning of Tunisia's shift away from a rigid, state-controlled financial system.

🌱 Very Common