1 dinar – Tunisia

Add to wishlist

Tunisia

Context

Material

Diameter: 28 mm

Weight: 10 g

Thickness: 2.08 mm

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #

Numista: #1204

Value

Exchange value: 1 TND

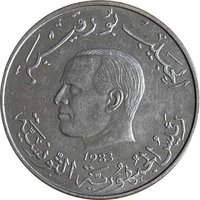

Obverse

Reverse

Description:

A woman harvesting olives with wheat, a tractor, and a palm tree behind her.

Inscription:

البنك المركزي التونسي

ELMEKKI

دينار 1 واحد

ELMEKKI

دينار 1 واحد

Translation:

Central Bank of Tunisia

ELMEKKI

1 One Dinar

ELMEKKI

1 One Dinar

Script: Arabic

Engraver: Hatem El Mekki

Edge

Plain

Categories

| Organization> FAO |

| Transportation> Truck or tractor |

Mints

| Name | Mark |

|---|---|

| Monnaie de Paris | — |

| VDM Metals / Vereinigte Deutsche Metallwerke | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1976 | — | 12,000,000 | ||

| 1983 | — | 4,000,000 |

Historical background

In 1976, Tunisia's currency situation was characterized by stability under a managed exchange rate regime, with the Tunisian dinar (TND) pegged to a basket of currencies. This system, overseen by the Central Bank of Tunisia, provided a predictable environment for trade and investment, which was crucial for the country's development strategy. The dinar's value was maintained through conservative fiscal and monetary policies, supported by revenues from key exports like phosphates, olive oil, and a growing tourism sector. This relative strength reflected the broader economic planning of the era, which emphasized state-led industrialization and social development.

However, underlying pressures were beginning to emerge. The global economic shocks of the 1970s, including the 1973 oil crisis, had a mixed impact; while Tunisia was a modest oil exporter, it also faced higher import costs for machinery and manufactured goods. Furthermore, the ambitious public investment programs of the 1970s, funded partly by external borrowing, started to contribute to a widening trade deficit and growing external debt. These factors subtly strained the managed currency regime, foreshadowing the balance of payments challenges that would become more pronounced in the following decade.

Consequently, 1976 represents a point of relative calm before a period of adjustment. The currency's stability was a point of pride and a tool for economic planning, yet the model was increasingly vulnerable to external imbalances. The government's response in the late 1970s and early 1980s would shift toward economic liberalization and seek structural adjustment loans, setting the stage for eventual devaluations of the dinar to improve competitiveness and address the mounting economic pressures that were quietly building during this time.

However, underlying pressures were beginning to emerge. The global economic shocks of the 1970s, including the 1973 oil crisis, had a mixed impact; while Tunisia was a modest oil exporter, it also faced higher import costs for machinery and manufactured goods. Furthermore, the ambitious public investment programs of the 1970s, funded partly by external borrowing, started to contribute to a widening trade deficit and growing external debt. These factors subtly strained the managed currency regime, foreshadowing the balance of payments challenges that would become more pronounced in the following decade.

Consequently, 1976 represents a point of relative calm before a period of adjustment. The currency's stability was a point of pride and a tool for economic planning, yet the model was increasingly vulnerable to external imbalances. The government's response in the late 1970s and early 1980s would shift toward economic liberalization and seek structural adjustment loans, setting the stage for eventual devaluations of the dinar to improve competitiveness and address the mounting economic pressures that were quietly building during this time.

🌱 Very Common