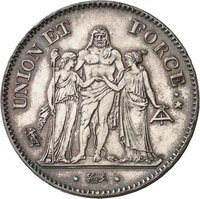

Obverse

Description:

Long-haired head in Phrygian cap; "Dupré" in cursive below, encircled by dotted border.

Inscription:

REPUBLIQUE FRANÇAISE

· Dupré ·

· Dupré ·

Script: Latin

Engraver: Augustin Dupré

Reverse

Description:

Face value "A CENTIM" in letters, with vintage, marks, and workshop letter below. "TEST PIECE" may appear only on some year 6 coins.

Inscription:

UN

CENTIME

L'AN 7·

A

CENTIME

L'AN 7·

A

Script: Latin

Engraver: Augustin Dupré

Edge

Plain

Categories

| Symbol> Phrygian cap |

Mints

| Name | Mark |

|---|---|

| Monnaie de Paris | A |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1797 | A | — | ||

| 1797 | — | — | ||

| 1798 | — | 48,778,486 | ||

| 1799 | — | 4,126,459 |

Historical background

By 1797, the financial experiment of the French Revolution had reached a crisis point. The revolutionary government, facing bankruptcy and war with much of Europe, had abandoned the old royal currency in 1789 and issued paper money known as assignats, backed by the value of confiscated church lands. Initially successful, this system collapsed under the weight of massive over-printing to fund wars and government operations. As public confidence evaporated, the assignats underwent hyperinflation, becoming virtually worthless and leading to severe economic dislocation, hoarding of goods, and a return to barter in many parts of the country.

The Directory, the ruling executive body, attempted a drastic solution. In February 1796, it introduced a new paper currency called the mandat territorial, which was also supposedly backed by national lands. However, this was essentially a disguised currency conversion that failed to address the core issue of public trust and fiscal discipline. The mandats suffered the same fate as their predecessors, losing most of their value within months. By 1797, both paper currencies were discredited, and the economy was in a state of paralysis, crippling government credit and exacerbating social unrest.

Faced with this untenable situation, the Directory took a decisive and conservative turn. In July 1797, it passed a law demonetizing all paper currency, effectively declaring a bankruptcy of the state's paper money system. This "territorial mandate liquidation" forced a painful return to hard currency—primarily silver and gold coinage. While this restored monetary stability and ended hyperinflation, it also caused widespread hardship, as those holding paper assets were ruined and the state struggled to pay its debts and soldiers, setting the stage for the political and financial reforms that would later be consolidated under Napoleon.

The Directory, the ruling executive body, attempted a drastic solution. In February 1796, it introduced a new paper currency called the mandat territorial, which was also supposedly backed by national lands. However, this was essentially a disguised currency conversion that failed to address the core issue of public trust and fiscal discipline. The mandats suffered the same fate as their predecessors, losing most of their value within months. By 1797, both paper currencies were discredited, and the economy was in a state of paralysis, crippling government credit and exacerbating social unrest.

Faced with this untenable situation, the Directory took a decisive and conservative turn. In July 1797, it passed a law demonetizing all paper currency, effectively declaring a bankruptcy of the state's paper money system. This "territorial mandate liquidation" forced a painful return to hard currency—primarily silver and gold coinage. While this restored monetary stability and ended hyperinflation, it also caused widespread hardship, as those holding paper assets were ruined and the state struggled to pay its debts and soldiers, setting the stage for the political and financial reforms that would later be consolidated under Napoleon.

🌱 Very Common