5 jiao – People's Republic of China

Add to wishlist

China

Context

Years: 1991–2001

Country: China

Issuer: People's Republic of China

Period:

(since 1949)

Currency:

(since 1955)

Material

References

KM: #

Numista: #1163

Value

Exchange value: 0.5 CNY

Inflation-adjusted value: 1.63 CNY

Obverse

Description:

China's emblem features Tian'anmen, the "Gate of Heavenly Peace" of the Forbidden City, under five stars, encircled by the text "People's Republic of China."

Inscription:

ZHONGHUA RENMIN GONGHEGUO

中华人民共和国

2000

中华人民共和国

2000

Translation:

People's Republic of China

2000

2000

Language: Chinese

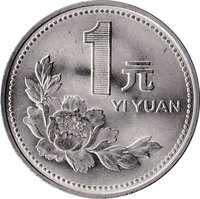

Reverse

Description:

Prunus mume blossom (Chinese plum/Japanese apricot), value in Chinese and Pinyin.

Inscription:

5 角

WU JIAO

WU JIAO

Translation:

FIVE JIAO

Language: Chinese

Edge

Alternating reeded and smooth segments (6 sets of 8 reeds)

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1991 | — | — | ||

| 1991 | — | — | Proof | |

| 1992 | — | — | ||

| 1992 | — | — | Proof | |

| 1993 | — | — | ||

| 1993 | — | — | Proof | |

| 1994 | — | — | ||

| 1994 | — | — | Proof | |

| 1995 | — | — | Proof | |

| 1995 | — | — | ||

| 1996 | — | — | ||

| 1996 | — | — | Proof | |

| 1997 | — | — | ||

| 1997 | — | — | Proof | |

| 1998 | — | — | ||

| 1998 | — | — | Proof | |

| 1999 | — | — | ||

| 1999 | — | — | Proof | |

| 2000 | — | — | ||

| 2000 | — | — | Proof | |

| 2001 | — | — |

Historical background

In 1991, the People's Republic of China operated under a complex dual-track currency system, a legacy of its incremental economic reforms. The official currency, the Renminbi (RMB), was strictly controlled by the People's Bank of China with a fixed, overvalued exchange rate pegged to a basket of currencies, heavily favoring the US dollar. This official rate was used for planned economy transactions, state-owned enterprise imports of key materials, and government accounting. However, alongside this existed a more market-driven "swap rate" available at Foreign Exchange Adjustment Centers (later known as Foreign Exchange Swap Centers), where enterprises could trade foreign exchange certificates (FECs) and foreign currency at a significantly depreciated rate. This secondary market reflected a truer scarcity value of foreign exchange, creating a substantial gap between the official and swap rates.

This bifurcated system was a pragmatic, though inefficient, solution to the pressures of China's transition from a command to a "socialist market economy." It aimed to shield the fragile state-owned industrial sector from external shocks while gradually introducing market mechanisms. The overvalued official rate subsidized critical imports for priority sectors, but it also discouraged exports, created a black market for foreign currency, and distorted economic decision-making. The existence of FECs, originally designed for foreign visitors to circumvent currency restrictions, further complicated the landscape, as they often traded at a premium to RMB in domestic markets.

The situation in 1991 was one of mounting pressure for unification. The success of export-oriented industries, particularly in Special Economic Zones, was generating growing foreign exchange reserves, increasing the strain and irrationality of the dual-track system. Policymakers were actively debating and planning for reform, viewing currency convertibility as a long-term goal essential for deeper global integration. Thus, 1991 represented a late stage in this transitional monetary framework, setting the stage for the pivotal unification of exchange rates and the landmark reforms of 1994, which abolished the swap market and FECs, moving decisively towards a single, managed floating rate system.

This bifurcated system was a pragmatic, though inefficient, solution to the pressures of China's transition from a command to a "socialist market economy." It aimed to shield the fragile state-owned industrial sector from external shocks while gradually introducing market mechanisms. The overvalued official rate subsidized critical imports for priority sectors, but it also discouraged exports, created a black market for foreign currency, and distorted economic decision-making. The existence of FECs, originally designed for foreign visitors to circumvent currency restrictions, further complicated the landscape, as they often traded at a premium to RMB in domestic markets.

The situation in 1991 was one of mounting pressure for unification. The success of export-oriented industries, particularly in Special Economic Zones, was generating growing foreign exchange reserves, increasing the strain and irrationality of the dual-track system. Policymakers were actively debating and planning for reform, viewing currency convertibility as a long-term goal essential for deeper global integration. Thus, 1991 represented a late stage in this transitional monetary framework, setting the stage for the pivotal unification of exchange rates and the landmark reforms of 1994, which abolished the swap market and FECs, moving decisively towards a single, managed floating rate system.

🌱 Very Common