10 fen – Republic of China

Add to wishlist

Standard circulation coins

Series: 2nd Series

China

Context

Years: 1936–1939

Country: China

Issuer: Republic of China

Period:

(1912—1949)

Currency:

(1912—1948)

Demonetized: Yes

Total mintage: 238,203,000

Material

References

Y: #

Numista: #9381

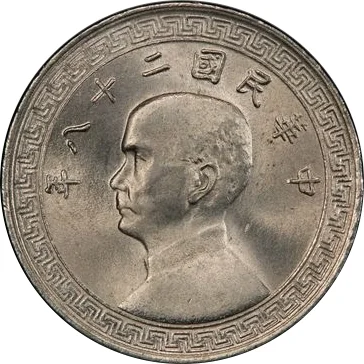

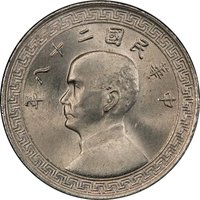

Obverse

Reverse

Description:

Ancient Chinese spade coin with one ideogram per side within a decorative border.

Inscription:

分拾

貝齊

貝齊

Translation:

Twenty Catties of Cowrie Shells.

Script: Chinese

Language: Classical Chinese

Edge

Plain

Categories

| Currency> Coin depiction |

| Person> Politician |

Mints

| Name | Mark |

|---|---|

| Münze Österreich | A |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1936 | — | 60,000,000 | ||

| 1938 | — | 110,203,000 | ||

| 1939 | — | 68,000,000 |

Historical background

In 1936, the currency situation in the Republic of China was in a state of fragile and contested unification under the Fabi (法幣) system, introduced by the Nationalist (Kuomintang) government in November 1935. This reform, driven by Finance Minister H.H. Kung, aimed to end the chaotic circulation of silver and various banknotes issued by multiple domestic and foreign banks. The government centralized note-issuing authority in three state-controlled banks—the Central Bank of China, the Bank of China, and the Bank of Communications—and decoupled the currency from silver, making the Fabi a managed fiat currency. This move successfully halted a severe deflationary crisis caused by the U.S. Silver Purchase Act, which had drained silver from China.

However, the system's stability was inherently precarious. The Fabi was nominally linked to foreign exchange reserves, particularly the British pound and U.S. dollar, but the government lacked sufficient bullion and hard currency reserves to fully back the currency, leading to latent inflationary pressures. Furthermore, the authority of the Nanjing government was not absolute; regional warlords and the Chinese Communist Party in Yan'an issued their own competing currencies, while Japanese-controlled Manchuria and their encroachments in North China actively undermined the Fabi through the issuance of military notes and the establishment of puppet banks, aiming to destabilize the Chinese economy.

Thus, on the eve of the full-scale Second Sino-Japanese War (1937-1945), the Fabi system represented a critical but vulnerable step toward modern monetary sovereignty. Its success depended entirely on public confidence in the government and the maintenance of political stability—conditions that would be shattered within a year. The coming war would force the Nationalist government to resort to excessive currency printing to finance its deficits, leading to the hyperinflation that ultimately destroyed the Fabi's value in the following decade.

However, the system's stability was inherently precarious. The Fabi was nominally linked to foreign exchange reserves, particularly the British pound and U.S. dollar, but the government lacked sufficient bullion and hard currency reserves to fully back the currency, leading to latent inflationary pressures. Furthermore, the authority of the Nanjing government was not absolute; regional warlords and the Chinese Communist Party in Yan'an issued their own competing currencies, while Japanese-controlled Manchuria and their encroachments in North China actively undermined the Fabi through the issuance of military notes and the establishment of puppet banks, aiming to destabilize the Chinese economy.

Thus, on the eve of the full-scale Second Sino-Japanese War (1937-1945), the Fabi system represented a critical but vulnerable step toward modern monetary sovereignty. Its success depended entirely on public confidence in the government and the maintenance of political stability—conditions that would be shattered within a year. The coming war would force the Nationalist government to resort to excessive currency printing to finance its deficits, leading to the hyperinflation that ultimately destroyed the Fabi's value in the following decade.

Series: 2nd Series

🌱 Common