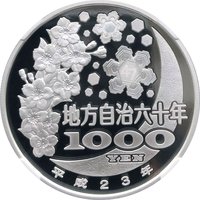

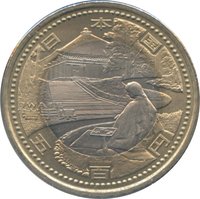

1000 Yen (Local Autonomy Law) – Japan

Non-circulating coins

Commemoration: 60th anniversary of Local Autonomy Law

Japan

Context

Year: 2011

Japanese - Heisei era Year: 23

Issuer: Japan

Ruler: Heisei

Currency:

(since 1871)

Total mintage: 100,000

Material

Diameter: 40 mm

Weight: 31.1 g

Silver weight: 31.07 g

Thickness: 3.5 mm

Shape: Round

Composition: 99.9% Silver

Standard: Silver ounce

Magnetic: No

Alignment: Medal alignment

flip

References

Y: #Click to copy to clipboard182

Numista: #123663

Value

Exchange value: 1000 JPY = $6.41

Bullion value: $90.12

Inflation-adjusted value: 1147.20 JPY

Obverse

Reverse

Edge

Slanted reeding right

Mints

| Name | Mark |

|---|---|

| Japan Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2011 | — | 100,000 | Proof |

Historical background

In 2011, Japan's currency situation was dominated by the historic and complex challenge of the yen's sharp appreciation, which reached post-World War II highs against the US dollar. This surge, driven by global risk aversion following the European debt crisis and the US credit rating downgrade, was severely exacerbated by the Great East Japan Earthquake and Fukushima nuclear disaster in March. The catastrophic events triggered massive repatriation of overseas assets by Japanese insurers and corporations, a typical "safe-haven" flight to the yen, pushing the USD/JPY rate toward 76—a level that threatened to cripple Japan's export-dependent economy by making its products more expensive abroad.

The Japanese government and the Bank of Japan (BOJ) responded with unprecedented and coordinated interventions. In March, the G7 nations jointly intervened to sell yen for the first time in over a decade, providing temporary relief. The BOJ also aggressively expanded monetary easing, establishing a ¥10 trillion asset purchase program and later increasing it, while committing to maintain a zero-interest-rate policy. Despite these efforts, the yen's strength persisted through much of the year, prompting a second, massive unilateral intervention by Japan's Ministry of Finance in October, selling an estimated ¥8 trillion yen in a single day to weaken the currency.

The persistent strength of the yen throughout 2011 highlighted the profound structural dilemmas facing Japan's economy. It occurred against a backdrop of prolonged deflation and weak domestic demand, forcing policymakers to balance currency stability with broader economic stimulus. The situation set the stage for the more radical "Abenomics" policies that would follow in 2012-2013, which explicitly targeted yen depreciation through ultra-aggressive monetary easing. Thus, 2011 was a pivotal year where traditional tools struggled, underscoring the need for a new, more forceful policy paradigm to address Japan's entrenched economic stagnation.

The Japanese government and the Bank of Japan (BOJ) responded with unprecedented and coordinated interventions. In March, the G7 nations jointly intervened to sell yen for the first time in over a decade, providing temporary relief. The BOJ also aggressively expanded monetary easing, establishing a ¥10 trillion asset purchase program and later increasing it, while committing to maintain a zero-interest-rate policy. Despite these efforts, the yen's strength persisted through much of the year, prompting a second, massive unilateral intervention by Japan's Ministry of Finance in October, selling an estimated ¥8 trillion yen in a single day to weaken the currency.

The persistent strength of the yen throughout 2011 highlighted the profound structural dilemmas facing Japan's economy. It occurred against a backdrop of prolonged deflation and weak domestic demand, forcing policymakers to balance currency stability with broader economic stimulus. The situation set the stage for the more radical "Abenomics" policies that would follow in 2012-2013, which explicitly targeted yen depreciation through ultra-aggressive monetary easing. Thus, 2011 was a pivotal year where traditional tools struggled, underscoring the need for a new, more forceful policy paradigm to address Japan's entrenched economic stagnation.

💎 Very Rare