10 Yuan (Taiwan) – Taiwan

Circulating commemorative coins

Commemoration: 50th Anniversary of Taiwan Restoration

China

Context

Year: 1995

Chinese republican Year: 84

Country: China

Issuer: Taiwan

Period:

(since 1949)

Currency:

(since 1949)

Total mintage: 30,000,000

Material

References

Y: #Click to copy to clipboard555

Numista: #10246

Value

Exchange value: 10 TWD

Inflation-adjusted value: 20.78 TWD

Obverse

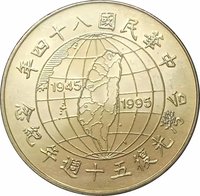

Description:

Globle map of Taiwan and outlying islands.

Inscription:

年四十八國民華中

1945 1995

念紀年週十五復光灣台

1945 1995

念紀年週十五復光灣台

Translation:

48th Year of the Republic of China

1945 1995

Commemorating the 50th Anniversary of the Recovery of Taiwan

1945 1995

Commemorating the 50th Anniversary of the Recovery of Taiwan

Language: Chinese

Reverse

Description:

Legend in seal script, central value.

Inscription:

灣台大営経同共

圓 拾

10

體同共命生的共與戚休聚搏

圓 拾

10

體同共命生的共與戚休聚搏

Translation:

Jointly Managed Taiwan Military Camp;

Ten Dollars;

Shared Destiny, United in Life and Death, Gathering and Striving Together Through Weal and Woe

Ten Dollars;

Shared Destiny, United in Life and Death, Gathering and Striving Together Through Weal and Woe

Language: Chinese

Edge

Reeded

Categories

| Map |

Mints

| Name | Mark |

|---|---|

| Central Mint of Taiwan | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1995 | — | 30,000,000 |

Historical background

In 1995, Taiwan's currency, the New Taiwan Dollar (NTD), operated within a managed float system overseen by the Central Bank of the Republic of China (Taiwan). The period was characterized by relative stability and strength, driven by Taiwan's robust export-led economic growth, which generated consistent trade surpluses and substantial foreign exchange reserves. This economic vitality, coupled with high domestic savings and controlled inflation, provided a solid foundation for the currency. The central bank actively intervened in the foreign exchange market to smooth out excessive volatility, generally allowing the NTD to appreciate gradually against the US dollar to help manage imported inflation and moderate the cost pressures on its vital export sector.

However, the currency environment was not without significant external pressures. The mid-1990s saw escalating tensions in the Taiwan Strait, notably following China's military exercises and missile tests in 1995-1996. This geopolitical uncertainty created episodic periods of financial market nervousness, leading to potential capital outflow pressures and downward speculation on the NTD. The central bank was therefore tasked with a delicate balancing act: maintaining currency stability to ensure economic confidence while holding sufficient foreign reserves to defend the NTD against speculative attacks driven by political risks.

Ultimately, the sound fundamentals of Taiwan's economy proved resilient. The central bank's substantial war chest of foreign reserves, which continued to grow throughout the period, acted as a powerful deterrent against sustained speculative pressure. Consequently, while the Strait crisis caused temporary financial market jitters, the NTD emerged from 1995 without a major devaluation crisis, reflecting the underlying strength of Taiwan's economic model and the proactive, stability-focused management of its monetary authorities during a time of both economic success and political uncertainty.

However, the currency environment was not without significant external pressures. The mid-1990s saw escalating tensions in the Taiwan Strait, notably following China's military exercises and missile tests in 1995-1996. This geopolitical uncertainty created episodic periods of financial market nervousness, leading to potential capital outflow pressures and downward speculation on the NTD. The central bank was therefore tasked with a delicate balancing act: maintaining currency stability to ensure economic confidence while holding sufficient foreign reserves to defend the NTD against speculative attacks driven by political risks.

Ultimately, the sound fundamentals of Taiwan's economy proved resilient. The central bank's substantial war chest of foreign reserves, which continued to grow throughout the period, acted as a powerful deterrent against sustained speculative pressure. Consequently, while the Strait crisis caused temporary financial market jitters, the NTD emerged from 1995 without a major devaluation crisis, reflecting the underlying strength of Taiwan's economic model and the proactive, stability-focused management of its monetary authorities during a time of both economic success and political uncertainty.

🌱 Common