1 Peseta – Spain

Spain

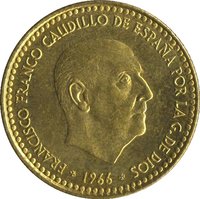

Obverse

Description:

Franco facing right.

Inscription:

FRANCISCO FRANCO CAUDILLO DE ESPAÑA POR LA G.DE DIOS

✠ 1966 ✠

✠ 1966 ✠

Translation:

Francisco Franco Caudillo of Spain by the Grace of God

✠ 1966 ✠

✠ 1966 ✠

Script: Latin

Language: Spanish

Engraver: Manuel Marín Jimeno

Designer: Juan de Ávalos Taborda

Reverse

Description:

Coat of arms with yoke and arrows.

Inscription:

🟌 UNA 🟌 PESETA

UNA GRANDE LIBRE

PLUS ULTRA

UNA GRANDE LIBRE

PLUS ULTRA

Translation:

One Peseta

One Great Free

Further Beyond

One Great Free

Further Beyond

Script: Latin

Engraver: Manuel Marín Jimeno

Edge

Reeded

Categories

| Person> Military leader |

| Person> Politician |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Royal Mint of Madrid | (🟌) |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1967 | — | 59,000,000 | ||

| 1968 | — | 120,000,000 | ||

| 1969 | — | 120,000,000 | ||

| 1970 | — | 75,000,000 | ||

| 1971 | — | 115,270,000 | ||

| 1972 | — | 30,000 | Proof | |

| 1972 | — | 106,000,000 | ||

| 1973 | — | 25,000 | Proof | |

| 1973 | — | 152,000,000 | ||

| 1974 | — | 23,000 | Proof | |

| 1974 | — | 181,000,000 | ||

| 1975 | 🟌 | — | ||

| 1975 | — | 75,000 | Proof | |

| 1975 | — | 227,580,000 |

Historical background

In 1967, Spain's currency situation was defined by the peseta operating under a tightly controlled and overvalued fixed exchange rate regime, managed by the Franco dictatorship's economic authorities. The official rate was pegged at 60 pesetas to the US dollar, a rate maintained since 1959 as part of the Stabilization Plan that had initially opened Spain's autarkic economy. However, this official rate was largely symbolic for international trade, as a complex system of multiple effective exchange rates (MERs) was used to subsidize essential imports and tax non-essential ones, creating a distorted and bureaucratic financial environment.

Economically, this period was one of growing strain. The so-called "Spanish Miracle" of rapid industrialization and tourism-led growth was fueling inflation and a significant trade deficit. The overvalued peseta, combined with rising domestic costs, made Spanish exports less competitive and encouraged an outflow of foreign currency reserves. This pressure exposed the underlying weakness of the fixed parity, as the regime struggled to balance the need for economic liberalization with its desire for strict control.

Consequently, 1967 sat on the precipice of a major devaluation. The government attempted one last measure to avoid a formal parity change: in November 1967, it introduced a "parallel market" for certain financial transactions, effectively creating a dual exchange rate. This was a stopgap measure that acknowledged market pressures without abandoning the official peg. It failed to resolve the fundamental imbalances, however, setting the stage for the inevitable and substantial devaluation of the peseta that would follow in 1968, when the official rate was adjusted to 70 pesetas per dollar.

Economically, this period was one of growing strain. The so-called "Spanish Miracle" of rapid industrialization and tourism-led growth was fueling inflation and a significant trade deficit. The overvalued peseta, combined with rising domestic costs, made Spanish exports less competitive and encouraged an outflow of foreign currency reserves. This pressure exposed the underlying weakness of the fixed parity, as the regime struggled to balance the need for economic liberalization with its desire for strict control.

Consequently, 1967 sat on the precipice of a major devaluation. The government attempted one last measure to avoid a formal parity change: in November 1967, it introduced a "parallel market" for certain financial transactions, effectively creating a dual exchange rate. This was a stopgap measure that acknowledged market pressures without abandoning the official peg. It failed to resolve the fundamental imbalances, however, setting the stage for the inevitable and substantial devaluation of the peseta that would follow in 1968, when the official rate was adjusted to 70 pesetas per dollar.

🌱 Very Common