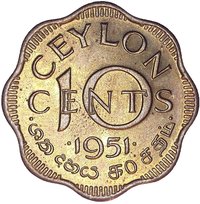

10 cents – Ceylon

Add to wishlist

Sri Lanka

Context

Material

Diameter: 23 mm

Weight: 4.21 g

Thickness: 1.31 mm

Shape: Scalloped

Composition: Nickel brass

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #5497

Obverse

Description:

Crowned left-facing bust.

Inscription:

KING GEORGE THE SIXTH

Translation:

KING GEORGE THE SIXTH

Language: English

Engraver: Percy Metcalfe

Reverse

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Royal Mint (Tower Hill) | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1951 | — | 150 | Proof | |

| 1951 | 1951-1962 | 34,760,000 |

Historical background

In 1951, Ceylon (present-day Sri Lanka) operated under a sterling exchange standard, with its currency, the Ceylon Rupee, pegged to the British Pound Sterling. This meant the island's monetary system and foreign reserves were deeply integrated with the United Kingdom's. The economy was heavily dependent on the export of three primary commodities: tea, rubber, and coconut products. The year 1951 was marked by exceptional prosperity due to the Korean War boom, which created soaring global demand and record-high prices for rubber and, to a lesser extent, tea. This resulted in a substantial balance of payments surplus and a significant accumulation of sterling reserves in London.

However, this apparent prosperity masked underlying vulnerabilities. The currency system meant that Ceylon's wealth was effectively held in sterling assets, subject to British monetary policy and the strength of the UK economy. While reserves grew, the colonial-era structure limited autonomous monetary control. Furthermore, the economy's extreme reliance on a few volatile export commodities made it susceptible to sudden shifts in terms of trade. The windfall from the Korean War was already recognized as temporary, prompting discussions about the need for economic diversification and the potential for establishing a central bank to better manage the nation's finances.

The situation in 1951, therefore, was a paradoxical blend of immediate fiscal strength and long-term structural fragility. The currency peg provided stability but at the cost of economic sovereignty. The tremendous export earnings filled the reserves but highlighted a dangerous over-specialization. This context set the stage for major financial reforms later in the decade, most notably the establishment of the Central Bank of Ceylon in 1950, which began its operational life in this period of plenty, and the subsequent shift to a managed currency system in 1952 as the post-Korean War slump began to expose the system's inherent risks.

However, this apparent prosperity masked underlying vulnerabilities. The currency system meant that Ceylon's wealth was effectively held in sterling assets, subject to British monetary policy and the strength of the UK economy. While reserves grew, the colonial-era structure limited autonomous monetary control. Furthermore, the economy's extreme reliance on a few volatile export commodities made it susceptible to sudden shifts in terms of trade. The windfall from the Korean War was already recognized as temporary, prompting discussions about the need for economic diversification and the potential for establishing a central bank to better manage the nation's finances.

The situation in 1951, therefore, was a paradoxical blend of immediate fiscal strength and long-term structural fragility. The currency peg provided stability but at the cost of economic sovereignty. The tremendous export earnings filled the reserves but highlighted a dangerous over-specialization. This context set the stage for major financial reforms later in the decade, most notably the establishment of the Central Bank of Ceylon in 1950, which began its operational life in this period of plenty, and the subsequent shift to a managed currency system in 1952 as the post-Korean War slump began to expose the system's inherent risks.

Series: 1951 Ceylon circulation coins

🌱 Very Common