1 dollar – Zimbabwe

Add to wishlist

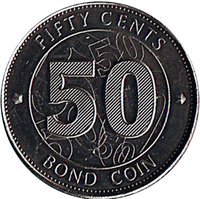

Zimbabwe

Context

Material

Diameter: 28 mm

Weight: 9.06 g

Thickness: 2 mm

Shape: Round

Techniques: Latent image, Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #97295

Value

Exchange value: 1 ZWL

Obverse

Reverse

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| South African Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2016 | — | — | ||

| 2017 | — | — |

Historical background

By 2016, Zimbabwe was entrenched in a severe multi-currency crisis, operating without its own sovereign currency. Following the catastrophic hyperinflation of the Zimbabwean dollar, which was officially abandoned in 2009, the country had adopted a basket of foreign currencies, primarily the US dollar. This "dollarization" initially brought stability and curbed inflation, but it created a new set of structural problems. As a global commodity price slump hit exports and government spending remained high, physical US dollar notes became critically scarce. The economy suffered from deflation, liquidity constraints, and a collapse in banking sector confidence, leading to long queues at banks and strict withdrawal limits that stifled business and daily life.

In response to the cash shortage, the Reserve Bank of Zimbabwe (RBZ) introduced a controversial surrogate currency in November 2016: bond notes. Officially pegged at 1:1 to the US dollar, these notes were intended to circulate alongside the US dollar and other currencies within the multi-currency system. The government insisted they were backed by a $200 million African Export-Import Bank loan, but the public, haunted by the memory of hyperinflation, was deeply skeptical. This move failed to resolve the underlying crisis of confidence and instead set the stage for a divergence between the official peg and market reality.

Consequently, a thriving black market for foreign currency emerged, where US dollars traded at a significant premium to bond notes. This created a three-tier pricing system: prices in real US dollars, prices in bond notes (often higher), and even higher prices for electronic money (RTGS balances), which had also begun to trade at a discount due to fears of future conversion risks. Thus, 2016 marked the beginning of the unravelling of the multi-currency system, as the introduction of bond notes eroded trust and sowed the seeds for the return of a de facto local currency and the inflationary pressures that would follow in subsequent years.

In response to the cash shortage, the Reserve Bank of Zimbabwe (RBZ) introduced a controversial surrogate currency in November 2016: bond notes. Officially pegged at 1:1 to the US dollar, these notes were intended to circulate alongside the US dollar and other currencies within the multi-currency system. The government insisted they were backed by a $200 million African Export-Import Bank loan, but the public, haunted by the memory of hyperinflation, was deeply skeptical. This move failed to resolve the underlying crisis of confidence and instead set the stage for a divergence between the official peg and market reality.

Consequently, a thriving black market for foreign currency emerged, where US dollars traded at a significant premium to bond notes. This created a three-tier pricing system: prices in real US dollars, prices in bond notes (often higher), and even higher prices for electronic money (RTGS balances), which had also begun to trade at a discount due to fears of future conversion risks. Thus, 2016 marked the beginning of the unravelling of the multi-currency system, as the introduction of bond notes eroded trust and sowed the seeds for the return of a de facto local currency and the inflationary pressures that would follow in subsequent years.

🌱 Fairly Common