5 Hryven – Ukraine

Ukraine

Context

Year: 2012

Issuer: Ukraine

Issuing organization: National Bank of Ukraine

Period:

(since 1991)

Currency:

(since 1996)

Total mintage: 20,000

Material

References

KM: #Click to copy to clipboard645

Numista: #97270

Value

Exchange value: 5 UAH

Bullion value: $44.11

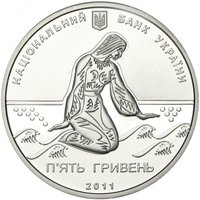

Obverse

Description:

The obverse features Ukraine's Small Coat of Arms above "НАЦІОНАЛЬНИЙ БАНК УКРАЇНИ." Within an ornamental pattern are the face value "5 ГРИВЕНЬ" and the year 2012. Below are the specifications Ag 925, 15.55 g, and the Mint's logotype.

Inscription:

НАЦІОНАЛЬНИЙ БАНК УКРАЇНИ

5 ГРИВЕНЬ

2012

5 ГРИВЕНЬ

2012

Translation:

NATIONAL BANK OF UKRAINE

5 HRYVEN

2012

5 HRYVEN

2012

Script: Cyrillic

Language: Ukrainian

Engraver: Volodymyr Atamanchuk

Reverse

Description:

A dragon, depicted in a cheap popular print style within a vegetable ornament, features an eye made of a 1.5 mm orange zirconia. Contour figures of all 12 Oriental zodiac symbols appear above and below this composition.

Engraver: Volodymyr Atamanchuk

Edge

Reeded

Categories

| Mythology> Fantastic animal |

| Astrology> Chinese calendar |

Mints

| Name | Mark |

|---|---|

| National Bank of Ukraine Banknote Printing and Minting Works | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2012 | — | 20,000 | Proof |

Historical background

In 2012, Ukraine's currency, the hryvnia (UAH), operated under a managed floating exchange rate regime, pegged loosely to the U.S. dollar within a narrow band set by the National Bank of Ukraine (NBU). The year was characterized by relative stability on the surface, with the official exchange rate hovering around 7.99-8.00 UAH per USD for much of the period. This stability was artificially maintained by the NBU through significant market interventions, utilizing the country's foreign currency reserves to support the hryvnia and meet International Monetary Fund (IMF) targets under a suspended standby agreement.

However, this apparent calm masked mounting underlying economic pressures. The economy was heavily dependent on steel and chemical exports, which suffered due to falling global commodity prices. Simultaneously, the cost of Russian gas imports remained cripplingly high, creating a persistent current account deficit. Furthermore, excessive government spending ahead of the October 2012 parliamentary elections, including populist measures like raising pensions and public sector wages, fueled inflation and increased budget deficits. These fundamental weaknesses created a growing overvaluation of the hryvnia, with a widening gap between the official rate and the weaker rate in the limited unofficial market.

Consequently, by the end of 2012, Ukraine was in a precarious position. The NBU's interventions to defend the currency had depleted international reserves to dangerously low levels, leaving the country vulnerable to external shocks. The IMF program was stalled due to the government's unwillingness to implement necessary austerity measures, such as raising domestic gas prices. While a full-scale currency crisis did not erupt until 2014 following political upheaval and the loss of Crimea, the unsustainable policies of 2012—artificial exchange rate stability, dwindling reserves, and lack of structural reforms—laid the crucial groundwork for the severe financial turmoil that would follow.

However, this apparent calm masked mounting underlying economic pressures. The economy was heavily dependent on steel and chemical exports, which suffered due to falling global commodity prices. Simultaneously, the cost of Russian gas imports remained cripplingly high, creating a persistent current account deficit. Furthermore, excessive government spending ahead of the October 2012 parliamentary elections, including populist measures like raising pensions and public sector wages, fueled inflation and increased budget deficits. These fundamental weaknesses created a growing overvaluation of the hryvnia, with a widening gap between the official rate and the weaker rate in the limited unofficial market.

Consequently, by the end of 2012, Ukraine was in a precarious position. The NBU's interventions to defend the currency had depleted international reserves to dangerously low levels, leaving the country vulnerable to external shocks. The IMF program was stalled due to the government's unwillingness to implement necessary austerity measures, such as raising domestic gas prices. While a full-scale currency crisis did not erupt until 2014 following political upheaval and the loss of Crimea, the unsustainable policies of 2012—artificial exchange rate stability, dwindling reserves, and lack of structural reforms—laid the crucial groundwork for the severe financial turmoil that would follow.

Series: Eastern calendar

💎 Extremely Rare