5 Hryven – Ukraine

Ukraine

Context

Year: 2013

Issuer: Ukraine

Issuing organization: National Bank of Ukraine

Period:

(since 1991)

Currency:

(since 1996)

Total mintage: 5,000

Material

References

KM: #Click to copy to clipboard696

Numista: #97241

Value

Exchange value: 5 UAH

Bullion value: $44.54

Obverse

Description:

The obverse features Ukraine's Small Coat of Arms and the National Bank inscription. The central design, reflecting a scientific worldview, combines a globe, a silicon crystal lattice, a human figure, and a light burst symbolizing new life. Below are the denomination "5 hryvnias" and the year 2013.

Inscription:

НАЦІОНАЛЬНИЙ БАНК УКРАЇНИ

П'ЯТЬ ГРИВЕНЬ

2013

П'ЯТЬ ГРИВЕНЬ

2013

Translation:

NATIONAL BANK OF UKRAINE

FIVE HRYVNIAS

2013

FIVE HRYVNIAS

2013

Script: Cyrillic

Language: Ukrainian

Engravers: Anatolii Demianenko, Volodymyr Atamanchuk

Designers: Oleksandr Kuzmin, Maria Skoblikova

Reverse

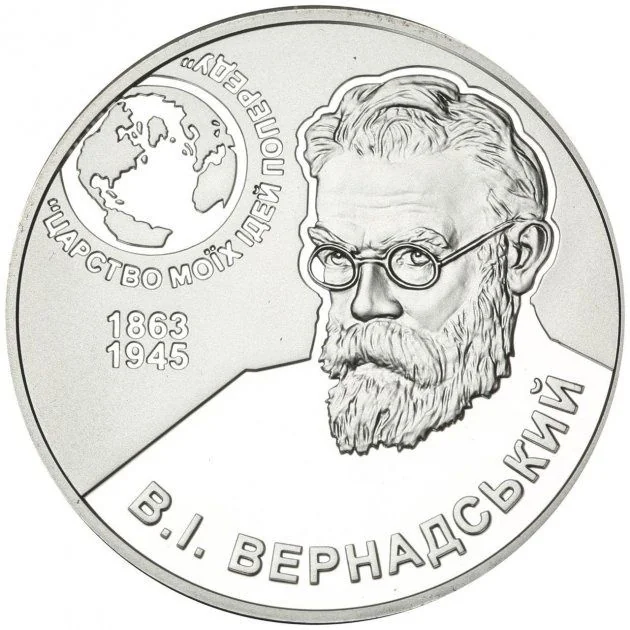

Description:

A portrait of Volodymyr Vernadsky is on the right. To the left, a globe bears his dictum "ЦАРСТВО МОЇХ ІДЕЙ ПОПЕРЕДУ" (1863/1945) and below it, the inscription "В. І. ВЕРНАДСЬКИЙ".

Inscription:

ЦАРСТВО МОЇХ ІДЕЙ ПОПЕРЕДУ

1863-1945

В. І. ВЕРНАДСЬКИЙ

1863-1945

В. І. ВЕРНАДСЬКИЙ

Translation:

THE KINGDOM OF MY IDEAS IS AHEAD

1863-1945

V. I. VERNADSKY

1863-1945

V. I. VERNADSKY

Script: Cyrillic

Language: Ukrainian

Engravers: Anatolii Demianenko, Volodymyr Atamanchuk

Edge

Smooth with in-depth legends

Mints

| Name | Mark |

|---|---|

| National Bank of Ukraine Banknote Printing and Minting Works | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2013 | — | 5,000 | Special Uncirculated |

Historical background

In 2013, Ukraine's currency, the hryvnia (UAH), was under significant strain due to a combination of deep-seated economic vulnerabilities and immediate political pressures. The country was grappling with a large current account deficit, dwindling foreign exchange reserves, and heavy reliance on expensive gas imports from Russia. These structural weaknesses were exacerbated by the government's refusal to implement critical economic reforms advocated by the International Monetary Fund (IMF), particularly regarding domestic gas subsidies. Consequently, investor confidence was low, and the National Bank of Ukraine (NBU) was engaged in a costly and ultimately unsustainable effort to maintain a de facto peg to the U.S. dollar, which had been in place since 2010.

The political dimension was paramount. President Viktor Yanukovych's sudden decision in November 2013 to reject an Association Agreement with the European Union in favor of closer ties with Russia triggered the Euromaidan protests. This political crisis created immediate capital flight and market panic, placing immense speculative pressure on the hryvnia. The NBU was forced to intervene heavily, spending billions from its reserves to defend the currency's value, which fell from approximately 8 UAH/USD at the start of the year to nearly 8.5 by year's end on the official market, with a much wider gap on the black market.

By December 2013, Ukraine's currency situation was precarious and on the brink of collapse. Foreign reserves had plummeted to a critically low level, covering less than two months of imports. The economy was sliding into recession, and the government faced an urgent need for external financing to avoid default. The stage was set for the severe currency crisis that would erupt in early 2014 following the revolution and Russia's annexation of Crimea, leading to a sharp devaluation where the hryvnia would lose over half of its value within a year.

The political dimension was paramount. President Viktor Yanukovych's sudden decision in November 2013 to reject an Association Agreement with the European Union in favor of closer ties with Russia triggered the Euromaidan protests. This political crisis created immediate capital flight and market panic, placing immense speculative pressure on the hryvnia. The NBU was forced to intervene heavily, spending billions from its reserves to defend the currency's value, which fell from approximately 8 UAH/USD at the start of the year to nearly 8.5 by year's end on the official market, with a much wider gap on the black market.

By December 2013, Ukraine's currency situation was precarious and on the brink of collapse. Foreign reserves had plummeted to a critically low level, covering less than two months of imports. The economy was sliding into recession, and the government faced an urgent need for external financing to avoid default. The stage was set for the severe currency crisis that would erupt in early 2014 following the revolution and Russia's annexation of Crimea, leading to a sharp devaluation where the hryvnia would lose over half of its value within a year.

✨ Legendary