10 dollars – United States

Add to wishlist

Non-circulating coins

Commemoration: First Spouse series - Lou Hoover

United States

Context

Material

Diameter: 26.5 mm

Weight: 15.55 g

Gold Weight:: 15.55 g

Thickness: 1.88 mm

Shape: Round

Composition: 99.99% Gold

Standard: Silver half ounce

Magnetic: No

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #

Numista: #95330

Value

Exchange value: 10 USD = $10.00

Bullion value: $2382.39

Inflation-adjusted value: 13.78 USD

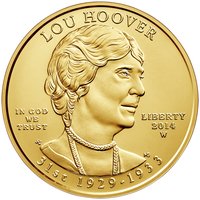

Obverse

Description:

Portrait of Lou Hoover

Inscription:

LOU HOOVER

IN GOD WE TRUST

LIBERTY

2014

W

31ST 1929-1933

IN GOD WE TRUST

LIBERTY

2014

W

31ST 1929-1933

Script: Latin

Engravers: Susan Gamble, Michael Gaudioso

Reverse

Description:

A 1920s-style radio commemorating First Lady Lou Henry Hoover’s first public radio address on April 19, 1929.

Inscription:

· UNITED STATES OF AMERICA ·

·E PLURIBUS UNUM ·

$10 · 1/2 Oz. .9999 FINE GOLD

·E PLURIBUS UNUM ·

$10 · 1/2 Oz. .9999 FINE GOLD

Script: Latin

Engravers: Richard Masters, Jim Licaretz

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| United States Mint of West Point | W |

Historical background

In 2014, the United States currency situation was characterized by a period of cautious normalization following the extraordinary measures of the Great Recession. The Federal Reserve, under Chair Janet Yellen, was in the process of winding down its quantitative easing (QE) program—a massive bond-buying initiative designed to suppress long-term interest rates and stimulate the economy. The "taper" of these purchases, announced in late 2013 and continued throughout 2014, signaled growing confidence in the economic recovery, with unemployment falling steadily. However, inflation remained persistently below the Fed's 2% target, creating a complex policy environment where strengthening growth coexisted with subdued price pressures.

The U.S. dollar itself embarked on a significant appreciation trend in the latter half of the year. This strength was driven by the diverging monetary policy paths between the Fed and other major central banks, like the European Central Bank and the Bank of Japan, which were moving toward further easing. As investors anticipated the first U.S. interest rate hikes since 2006, capital flowed into dollar-denominated assets, boosting the currency's value. A stronger dollar had mixed implications: it helped hold down inflation by making imports cheaper but also posed a headwind for U.S. exporters by making their goods more expensive abroad.

Overall, 2014 was a transitional year where the foundational concerns shifted from crisis-era stimulus to the timing and pace of policy normalization. The currency dynamics reflected a U.S. economy outperforming its developed-world peers, yet policymakers remained attentive to global risks and stubbornly low inflation. The stage was being set for the pivotal debates of 2015, which would ultimately lead to the first post-crisis rate hike in December of that year.

The U.S. dollar itself embarked on a significant appreciation trend in the latter half of the year. This strength was driven by the diverging monetary policy paths between the Fed and other major central banks, like the European Central Bank and the Bank of Japan, which were moving toward further easing. As investors anticipated the first U.S. interest rate hikes since 2006, capital flowed into dollar-denominated assets, boosting the currency's value. A stronger dollar had mixed implications: it helped hold down inflation by making imports cheaper but also posed a headwind for U.S. exporters by making their goods more expensive abroad.

Overall, 2014 was a transitional year where the foundational concerns shifted from crisis-era stimulus to the timing and pace of policy normalization. The currency dynamics reflected a U.S. economy outperforming its developed-world peers, yet policymakers remained attentive to global risks and stubbornly low inflation. The stage was being set for the pivotal debates of 2015, which would ultimately lead to the first post-crisis rate hike in December of that year.

✨ Legendary