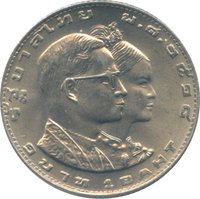

1 Baht (Princess Mother) – Thailand

Circulating commemorative coins

Commemoration: 75th Anniversary of birth of Princess Mother

Thailand

Context

Year: 1975

Thai Year: 2518

Issuer: Thailand

Ruler: Bhumibol Adulyadej

Currency:

(since 1897)

Demonetized: Yes

Total mintage: 9,000,000

Material

Diameter: 25 mm

Weight: 7 g

Thickness: 1.85 mm

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Medal alignment

flip

References

Y: #Click to copy to clipboard107

Numista: #9433

Value

Exchange value: 1 THB = $0.03

Obverse

Reverse

Edge

Reeded

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1975 | — | 9,000,000 |

Historical background

In 1975, Thailand's currency situation was characterized by a managed exchange rate system under the control of the Bank of Thailand, with the baht pegged to a basket of currencies weighted heavily towards the US dollar. This period followed the 1973 collapse of the Bretton Woods system, which had previously tied the baht directly to the dollar at a fixed rate of 20.80 baht per dollar. The shift to a basket peg provided more flexibility to buffer against international monetary fluctuations, but the baht's value remained tightly controlled and was not freely traded on open capital markets.

The Thai economy in the mid-1970s faced significant inflationary pressures and external shocks, which put strain on the currency's stability. The 1973 oil crisis had dramatically increased import costs, leading to persistent trade deficits and drawing down foreign reserves. Concurrently, domestic political turbulence following the 1973 student uprising and the subsequent shift to a democratic government created an environment of uncertainty. These factors combined to create pressure on the baht, necessitating careful management by monetary authorities to maintain the peg and control capital flows.

Despite these challenges, the baht remained relatively stable in 1975 due to conservative fiscal and monetary policies. The government, under Prime Minister Kukrit Pramoj, pursued austerity measures and secured international loans to bolster reserves. Furthermore, Thailand's growing agricultural exports and the beginnings of tourism and foreign direct investment provided essential sources of foreign exchange. Thus, while underlying economic vulnerabilities were present, the managed peg held firm throughout the year, setting a precedent for the tightly controlled exchange rate regime that would define Thai monetary policy for the next two decades until the Asian Financial Crisis of 1997.

The Thai economy in the mid-1970s faced significant inflationary pressures and external shocks, which put strain on the currency's stability. The 1973 oil crisis had dramatically increased import costs, leading to persistent trade deficits and drawing down foreign reserves. Concurrently, domestic political turbulence following the 1973 student uprising and the subsequent shift to a democratic government created an environment of uncertainty. These factors combined to create pressure on the baht, necessitating careful management by monetary authorities to maintain the peg and control capital flows.

Despite these challenges, the baht remained relatively stable in 1975 due to conservative fiscal and monetary policies. The government, under Prime Minister Kukrit Pramoj, pursued austerity measures and secured international loans to bolster reserves. Furthermore, Thailand's growing agricultural exports and the beginnings of tourism and foreign direct investment provided essential sources of foreign exchange. Thus, while underlying economic vulnerabilities were present, the managed peg held firm throughout the year, setting a precedent for the tightly controlled exchange rate regime that would define Thai monetary policy for the next two decades until the Asian Financial Crisis of 1997.

🌱 Common