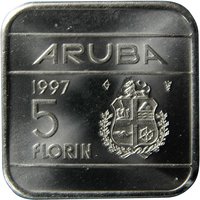

5 florin – Aruba

Add to wishlist

Netherlands

Context

Years: 2005–2013

Country: Netherlands

Issuer: Aruba

Ruler: Beatrix

Currency:

(since 1986)

Total mintage: 1,003,500

Material

Diameter: 23.45 mm

Weight: 8.4 g

Thickness: 2.7 mm

Shape: Round

Composition: Aluminium bronze

Magnetic: No

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #

Numista: #9341

Value

Exchange value: 5 AWG

Inflation-adjusted value: 7.74 AWG

Obverse

Description:

Aruban Coat of Arms, date above, value left.

Inscription:

ARUBA

2006

5

FLORIN

2006

5

FLORIN

Translation:

ARUBA

2006

5

FLORIN

2006

5

FLORIN

Script: Latin

Languages: Papiamento, English

Engraver: Evelino Fingal

Reverse

Description:

Queen Beatrix in profile, crowned, within an engraved frame.

Inscription:

Beatrix

KONINGIN

DER

NEDERLANDEN

KONINGIN

DER

NEDERLANDEN

Translation:

Beatrix

Queen

of the

Netherlands

Queen

of the

Netherlands

Script: Latin

Language: Dutch

Engraver: Evelino Fingal

Edge

Security edge with inscripted lettering

Legend:

GOD ZIJ MET ONS

Translation:

God be with us

Language: Dutch

Categories

| Symbols> Coat of Arms |

| Person> Monarch |

Mints

| Name | Mark |

|---|---|

| Royal Dutch Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2005 | — | 827,500 | ||

| 2006 | — | 102,000 | ||

| 2007 | — | 52,000 | ||

| 2008 | — | 22,000 | ||

| 2009 | — | — | ||

| 2010 | — | — | ||

| 2011 | — | — | ||

| 2012 | — | — | ||

| 2013 | — | — |

Historical background

In 2005, Aruba's currency situation was defined by its long-standing and stable peg to the United States dollar. Since 1986, the Aruban florin (AWG) had been fixed at a rate of 1.79 florin to 1 US dollar. This monetary policy, managed by the Central Bank of Aruba (CBA), provided a crucial anchor for the island's tourism-dependent economy, offering predictability for importers, exporters, and the vital hospitality sector, which primarily transacted in dollars. The peg was supported by adequate foreign exchange reserves and was considered a cornerstone of Aruba's economic stability, helping to control inflation and foster investor confidence.

The year 2005, however, fell within a period of notable economic challenge for the island. Aruba was still navigating the aftermath of a severe recession triggered earlier in the decade by the collapse of its major industry, tourism, following the September 11, 2001 attacks. While recovery was underway, public debt levels were high, exceeding 70% of GDP, placing fiscal pressure on the government. Despite this strain, the currency peg itself remained robust and was not under immediate threat, as the Central Bank maintained its commitment to the fixed exchange rate as a non-negotiable element of financial policy.

Consequently, the monetary landscape in 2005 was one of stability in the exchange rate regime amidst broader economic fragility. The Central Bank's focus was on maintaining the peg while managing the side effects, such as limited independent monetary policy tools to stimulate the economy. Discussions in financial circles occasionally touched on the pros and cons of dollarization, but the official stance was firmly in favor of retaining the managed florin. Thus, the currency situation reflected a strategic choice to prioritize exchange rate stability as a foundation for continued economic recovery and growth.

The year 2005, however, fell within a period of notable economic challenge for the island. Aruba was still navigating the aftermath of a severe recession triggered earlier in the decade by the collapse of its major industry, tourism, following the September 11, 2001 attacks. While recovery was underway, public debt levels were high, exceeding 70% of GDP, placing fiscal pressure on the government. Despite this strain, the currency peg itself remained robust and was not under immediate threat, as the Central Bank maintained its commitment to the fixed exchange rate as a non-negotiable element of financial policy.

Consequently, the monetary landscape in 2005 was one of stability in the exchange rate regime amidst broader economic fragility. The Central Bank's focus was on maintaining the peg while managing the side effects, such as limited independent monetary policy tools to stimulate the economy. Discussions in financial circles occasionally touched on the pros and cons of dollarization, but the official stance was firmly in favor of retaining the managed florin. Thus, the currency situation reflected a strategic choice to prioritize exchange rate stability as a foundation for continued economic recovery and growth.

🌱 Common