20 Francs (Republic) – Burundi

Non-circulating coins

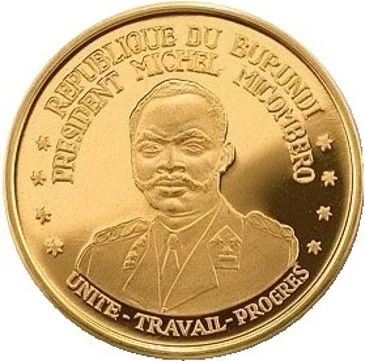

Commemoration: First Anniversary Of Republic

Burundi

Context

Material

References

KM: #Click to copy to clipboard12

Numista: #92365

Value

Exchange value: 20 BIF

Bullion value: $969.72

Categories

| Symbols> Coat of Arms |

| Person> Politician |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1967 | — | 2,000 | Proof |

Historical background

In 1967, Burundi's currency situation was fundamentally shaped by its recent independence from Belgian colonial rule in 1962. The nation was part of the African Financial Community (CFA franc zone), using the Burundian franc (FBu), which was pegged to the Belgian franc and, by extension, indirectly to the US dollar through the Bretton Woods system. This arrangement provided monetary stability but also tied Burundi's economy closely to that of its former colonial power, limiting autonomous monetary policy. The economy was overwhelmingly agrarian and fragile, with a narrow export base reliant on coffee, which accounted for the vast majority of foreign exchange earnings.

The year itself was politically turbulent, marked by a coup in July that brought Captain Michel Micombero to power, who declared the country a republic and ruled by decree. Despite this political upheaval, there was no major currency reform or devaluation in 1967. The primary monetary challenges stemmed from structural economic weaknesses: chronic trade deficits, very low foreign exchange reserves, and a severe shortage of hard currency. This scarcity constrained imports of essential goods and hampered development, fostering a reliance on foreign aid and credit from Belgium and other European partners.

Therefore, the 1967 currency situation was one of formal stability but underlying vulnerability. The fixed peg of the Burundian franc provided a nominal anchor, but the economy lacked the diversification and reserves to withstand external shocks. The state's focus was on political consolidation rather than monetary reform, leaving the fundamental constraints of a dependent, primary-commodity-based economy unaddressed. This precarious position would continue to characterize Burundi's financial landscape for decades to come.

The year itself was politically turbulent, marked by a coup in July that brought Captain Michel Micombero to power, who declared the country a republic and ruled by decree. Despite this political upheaval, there was no major currency reform or devaluation in 1967. The primary monetary challenges stemmed from structural economic weaknesses: chronic trade deficits, very low foreign exchange reserves, and a severe shortage of hard currency. This scarcity constrained imports of essential goods and hampered development, fostering a reliance on foreign aid and credit from Belgium and other European partners.

Therefore, the 1967 currency situation was one of formal stability but underlying vulnerability. The fixed peg of the Burundian franc provided a nominal anchor, but the economy lacked the diversification and reserves to withstand external shocks. The state's focus was on political consolidation rather than monetary reform, leaving the fundamental constraints of a dependent, primary-commodity-based economy unaddressed. This precarious position would continue to characterize Burundi's financial landscape for decades to come.

✨ Legendary