200 rupees (Bank of Mauritius) – Mauritius

Add to wishlist

Non-circulating coins

Commemoration: 40th Anniversary of the Bank of Mauritius

Mauritius

Context

Material

References

KM: #

Numista: #89541

Value

Exchange value: 200 MUR

Bullion value: $66.88

Obverse

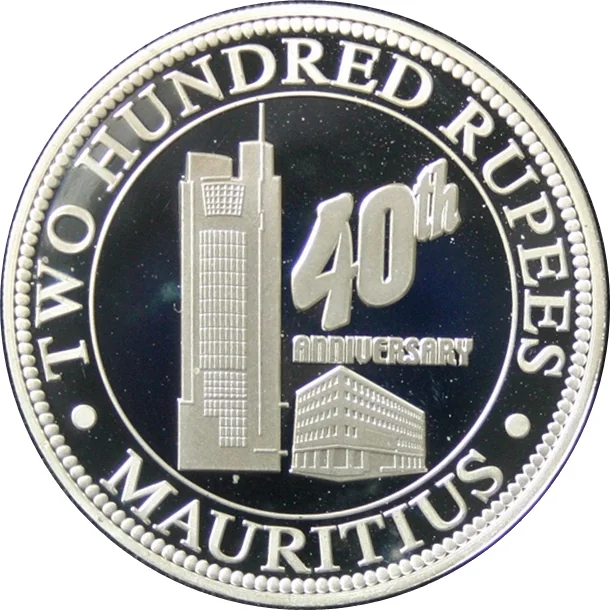

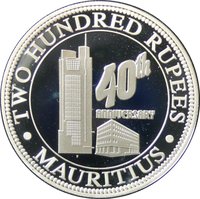

Reverse

Description:

Denomination above, 40-centre building, country below.

Inscription:

· TWO HUNDRED RUPPEES ·

MAURITIUS

40th

ANNIVERSARY

MAURITIUS

40th

ANNIVERSARY

Script: Latin

Edge

Milled

Mints

| Name | Mark |

|---|---|

| Monnaie de Paris | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2007 | — | 1,000 | Proof |

Historical background

In 2007, the Mauritian economy was undergoing a significant structural transformation, shifting from a reliance on sugar and textiles towards services, particularly tourism and financial services. This transition, coupled with strong global economic growth, placed considerable pressure on the Mauritian rupee (MUR). The year was characterized by a persistent and concerning trend of depreciation against major currencies, especially the US dollar and the euro. This depreciation was primarily driven by a widening current account deficit, as the cost of imports (including oil and capital goods) far exceeded the earnings from exports and tourism receipts.

In response to the rupee's decline, the Bank of Mauritius (BoM), the country's central bank, faced a complex policy dilemma. Its primary tool was direct intervention in the foreign exchange market, selling US dollars from its reserves to support the rupee. However, these interventions were costly and depleting foreign reserves. The BoM also tightened monetary policy, raising the Key Repo Rate by 50 basis points in June 2007 to 8.75%, aiming to curb inflation—which was being stoked by higher import prices—and to attract capital inflows to support the currency.

The currency situation in 2007 was a central challenge for policymakers, reflecting the growing pains of an open, island economy integrating into global markets. While the depreciation made Mauritian exports and tourism more competitive, it simultaneously increased the cost of living and business inputs, contributing to inflationary pressures. The year thus set the stage for ongoing debates about exchange rate management, reserve adequacy, and the broader economic reforms needed to ensure stability during the country's continued economic evolution.

In response to the rupee's decline, the Bank of Mauritius (BoM), the country's central bank, faced a complex policy dilemma. Its primary tool was direct intervention in the foreign exchange market, selling US dollars from its reserves to support the rupee. However, these interventions were costly and depleting foreign reserves. The BoM also tightened monetary policy, raising the Key Repo Rate by 50 basis points in June 2007 to 8.75%, aiming to curb inflation—which was being stoked by higher import prices—and to attract capital inflows to support the currency.

The currency situation in 2007 was a central challenge for policymakers, reflecting the growing pains of an open, island economy integrating into global markets. While the depreciation made Mauritian exports and tourism more competitive, it simultaneously increased the cost of living and business inputs, contributing to inflationary pressures. The year thus set the stage for ongoing debates about exchange rate management, reserve adequacy, and the broader economic reforms needed to ensure stability during the country's continued economic evolution.

✨ Legendary