50 Zlotys (Poland Regaining Independence) – Poland

Non-circulating coins

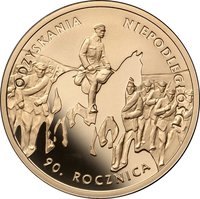

Commemoration: 90th Anniversary of Regaining Independence by Poland

Poland

Context

Material

Diameter: 18 mm

Weight: 3.13 g

Gold weight: 3.13 g

Shape: Round

Composition: 99.99% Gold

Standard: Gold tenth ounce

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

Y: #Click to copy to clipboard652

Numista: #88619

Value

Exchange value: 50 PLN = $13.99

Bullion value: $521.81

Inflation-adjusted value: 93.30 PLN

Obverse

Inscription:

RZECZPOSPOLITA POLSKA 2008

mw

ZŁ 50 ZŁ

mw

ZŁ 50 ZŁ

Translation:

REPUBLIC OF POLAND 2008

50 ZŁOTYCH 50 ZŁ

50 ZŁOTYCH 50 ZŁ

Script: Latin

Language: Polish

Designer: Ewa Olszewska-Borys

Reverse

Inscription:

ODZYSKANIA NIEPODLEGŁOŚCI

90. ROCZNICA

90. ROCZNICA

Translation:

90th Anniversary of Regaining Independence

Script: Latin

Language: Polish

Designer: Ewa Olszewska-Borys

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Mint of Poland | (MW) |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2008 | MW | 8,800 | Proof |

Historical background

In 2008, Poland's currency situation was dominated by the strength of the Polish złoty (PLN), which had been on a multi-year appreciation trend against both the euro and the US dollar. This was driven by Poland's robust economic growth, significant inflows of foreign direct investment (FDI) and portfolio investment, and rising interest rates that attracted carry-trade investors. The strong złoty was a double-edged sword: it helped contain inflation by making imports cheaper but simultaneously hurt the competitiveness of Polish exports, a crucial pillar of the economy, and increased the burden of foreign-currency-denominated loans held by many Polish households and businesses.

The global financial crisis, which intensified in the latter half of 2008, dramatically reversed this trend. As risk aversion spiked worldwide, investors began a rapid withdrawal of capital from emerging markets like Poland. This triggered a sharp and sudden depreciation of the złoty, which lost approximately 30% of its value against the euro between July and early 2009. The currency's plunge created immediate financial instability, severely straining borrowers with Swiss franc or euro-denominated mortgages, whose repayment costs skyrocketed in złoty terms.

In response, Poland's central bank (NBP) initially intervened in the foreign exchange market to support the currency and later embarked on a cycle of interest rate cuts starting in November 2008 to stimulate the faltering economy. Unlike many of its regional peers, Poland avoided a formal recession in 2009, but the year ended with the currency situation having flipped from a problem of excessive strength to one of destabilizing weakness, exposing the vulnerabilities created by earlier foreign currency borrowing.

The global financial crisis, which intensified in the latter half of 2008, dramatically reversed this trend. As risk aversion spiked worldwide, investors began a rapid withdrawal of capital from emerging markets like Poland. This triggered a sharp and sudden depreciation of the złoty, which lost approximately 30% of its value against the euro between July and early 2009. The currency's plunge created immediate financial instability, severely straining borrowers with Swiss franc or euro-denominated mortgages, whose repayment costs skyrocketed in złoty terms.

In response, Poland's central bank (NBP) initially intervened in the foreign exchange market to support the currency and later embarked on a cycle of interest rate cuts starting in November 2008 to stimulate the faltering economy. Unlike many of its regional peers, Poland avoided a formal recession in 2009, but the year ended with the currency situation having flipped from a problem of excessive strength to one of destabilizing weakness, exposing the vulnerabilities created by earlier foreign currency borrowing.

✨ Legendary