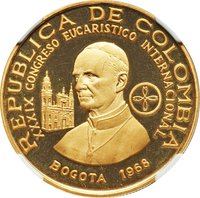

300 Pesos – Colombia

Non-circulating coins

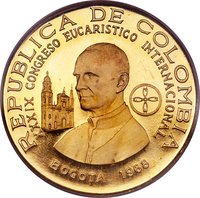

Commemoration: International Eucharistic Congress

Colombia

Obverse

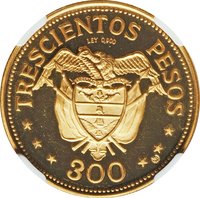

Reverse

Edge

Categories

| Building> Religious building |

| Symbols> Coat of Arms |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1968 | — | 62,000 | ||

| 1968 | — | 8,000 | Proof |

Historical background

In 1968, Colombia's currency situation was characterized by a managed exchange rate system under significant pressure. The country operated a fixed but adjustable peg to the U.S. dollar, a regime maintained by the Banco de la República. However, this system was strained by persistent balance of payments deficits, driven by a combination of factors including high inflation relative to trading partners and structural trade imbalances. The government frequently resorted to a complex system of exchange controls and multiple implicit rates for different transactions (such as for imports, exports, and financial flows) to manage the demand for foreign currency and protect international reserves, which created distortions in the economy.

The macroeconomic context was one of moderate growth but underlying fragility. While the National Front government pursued development plans, fiscal deficits were common, often financed by money creation from the central bank. This contributed to an inflationary environment that eroded the peso's real value and created constant tension with the official fixed exchange rate. The situation was further complicated by a decline in the growth of coffee exports—a traditional source of vital foreign exchange—which limited the inflow of dollars needed to support the currency peg and finance imports.

Recognizing these systemic issues, the government enacted a profound constitutional and economic reform in 1968. A key element was the granting of greater autonomy to the Banco de la República, aiming to insulate monetary policy from direct fiscal financing and political cycles. While a major devaluation would not occur until 1970, the reforms of 1968 laid the institutional groundwork for a more independent central bank, setting the stage for future adjustments to the exchange rate regime and attempts to achieve greater macroeconomic stability in the following decade.

The macroeconomic context was one of moderate growth but underlying fragility. While the National Front government pursued development plans, fiscal deficits were common, often financed by money creation from the central bank. This contributed to an inflationary environment that eroded the peso's real value and created constant tension with the official fixed exchange rate. The situation was further complicated by a decline in the growth of coffee exports—a traditional source of vital foreign exchange—which limited the inflow of dollars needed to support the currency peg and finance imports.

Recognizing these systemic issues, the government enacted a profound constitutional and economic reform in 1968. A key element was the granting of greater autonomy to the Banco de la República, aiming to insulate monetary policy from direct fiscal financing and political cycles. While a major devaluation would not occur until 1970, the reforms of 1968 laid the institutional groundwork for a more independent central bank, setting the stage for future adjustments to the exchange rate regime and attempts to achieve greater macroeconomic stability in the following decade.

✨ Legendary