2 piastres – Egypt

Add to wishlist

Egypt

Context

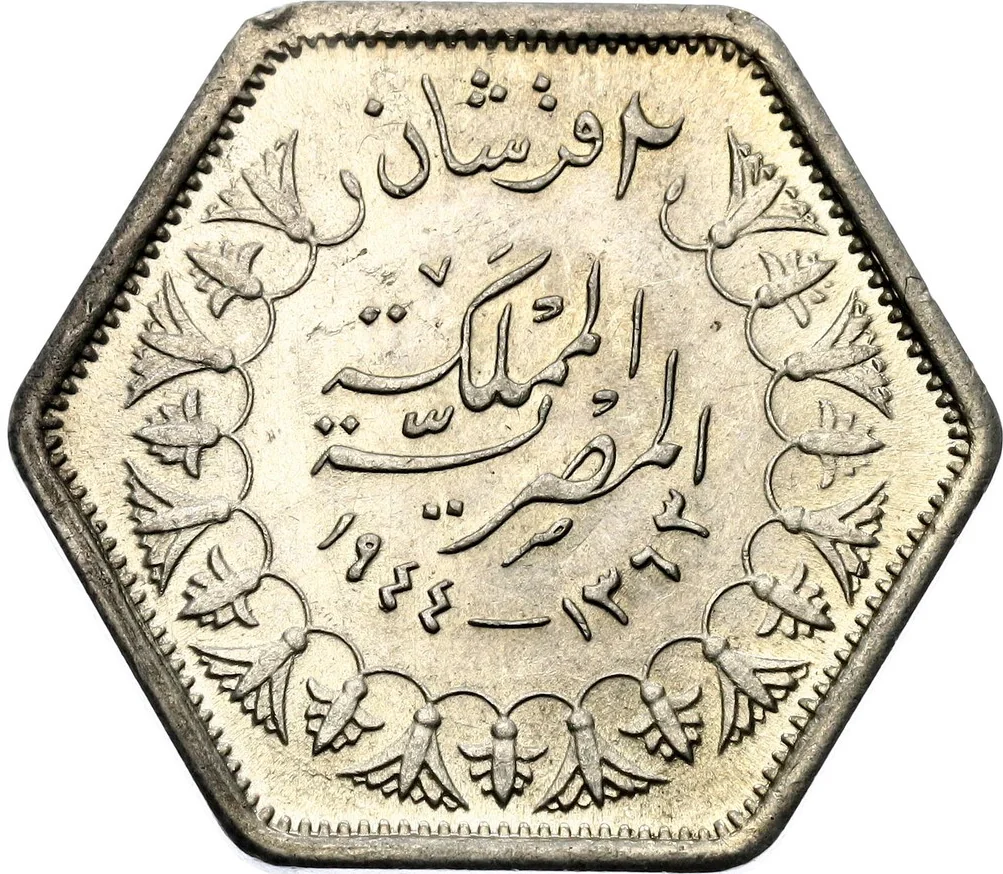

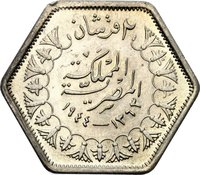

Year: 1944

Islamic (Hijri) Year:: 1363

Issuer: Egypt

Ruler: Farouk I

Currency:

(since 1916)

Demonetized: Yes

Total mintage: 32,000,000

Material

References

KM: #

Numista: #8677

Value

Exchange value: 0.02 EGP

Bullion value: $3.58

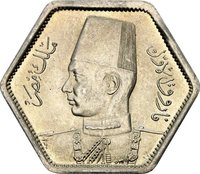

Obverse

Description:

King Farouk I of Egypt

Inscription:

فاروق الأول

ملك مصر

PM

ملك مصر

PM

Translation:

Farouk the First

King of Egypt

King of Egypt

Script: Arabic

Language: Arabic

Engraver: Percy Metcalfe

Reverse

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Pretoria | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1944 | — | 32,000,000 |

Historical background

In 1944, Egypt's currency situation was defined by its integration into the Sterling Area and the enduring legacy of the Egyptian Pound (EE) as a strong, gold-backed currency. Since 1885, the Egyptian pound had been pegged to gold and was effectively on a sterling standard, meaning its value was maintained through a fixed exchange rate with the British pound. This stability, managed by the National Bank of Egypt, made the Egyptian pound a trusted and convertible currency in international trade, particularly crucial for a cotton-exporting economy. However, this formal arrangement was underpinned by significant British economic and political influence, a reality solidified by the 1939 Sterling Area agreement which required Egypt to hold its foreign exchange reserves in London.

The Second World War profoundly strained this system. Egypt became a major Allied base, leading to a massive influx of British military spending in the form of sterling credits. This created a huge accumulation of sterling balances in London—essentially British IOUs—which far exceeded Egypt's normal reserve levels. While this boosted Egypt's nominal foreign assets, it also caused severe domestic inflation. The sterling balances were not immediately convertible into goods due to wartime shortages, leading to excess liquidity in the Egyptian economy and sharp rises in the cost of living, creating social and economic pressures.

Consequently, by 1944, Egypt faced a paradoxical currency position: it possessed immense foreign reserves on paper, but these were largely frozen and illiquid sterling claims. The stability of the Egyptian pound's external value masked growing internal economic distortions and a dependence on British economic policy. This situation set the stage for post-war negotiations, where Egypt would seek to utilize these blocked balances for development, and would eventually lead to a re-evaluation of its monetary sovereignty following the 1947 sterling crisis and, ultimately, the 1952 revolution.

The Second World War profoundly strained this system. Egypt became a major Allied base, leading to a massive influx of British military spending in the form of sterling credits. This created a huge accumulation of sterling balances in London—essentially British IOUs—which far exceeded Egypt's normal reserve levels. While this boosted Egypt's nominal foreign assets, it also caused severe domestic inflation. The sterling balances were not immediately convertible into goods due to wartime shortages, leading to excess liquidity in the Egyptian economy and sharp rises in the cost of living, creating social and economic pressures.

Consequently, by 1944, Egypt faced a paradoxical currency position: it possessed immense foreign reserves on paper, but these were largely frozen and illiquid sterling claims. The stability of the Egyptian pound's external value masked growing internal economic distortions and a dependence on British economic policy. This situation set the stage for post-war negotiations, where Egypt would seek to utilize these blocked balances for development, and would eventually lead to a re-evaluation of its monetary sovereignty following the 1947 sterling crisis and, ultimately, the 1952 revolution.

🌱 Very Common