25 Pesos – Argentina

Non-circulating coins

Commemoration: National Constitution Convention

Argentina

Obverse

Description:

A central field with the shields of Paraná and Santa Fe below, encircled by "Argentina Republic" above and "National Constitution" below.

Inscription:

.REPUBLICA ARGENTINA.

PARANA SANTA FE

CONSTITUCION NACIONAL

PARANA SANTA FE

CONSTITUCION NACIONAL

Translation:

Argentine Republic.

Paraná Santa Fe

National Constitution

Paraná Santa Fe

National Constitution

Script: Latin

Language: Spanish

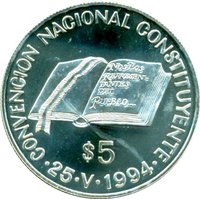

Reverse

Description:

Our Constitution coin: Features the Constitutional Preamble's start, "We the representatives of the People..." under its denomination. Edge reads "National Constituent Convention" and the date "25. V. 1994," when the convention began.

Inscription:

.CONVENCION NACIONAL CONSTITUYENTE.

$25

25.V.1994

$25

25.V.1994

Translation:

National Constituent Convention.

$25

25.V.1994

$25

25.V.1994

Script: Latin

Language: Spanish

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1994 | — | 5,000 | ||

| 1994 | — | 1,000 | Proof |

Historical background

In 1994, Argentina was in the midst of the Convertibility Plan, a monetary regime established in 1991 to end hyperinflation. The cornerstone of this plan was a currency board that fixed the Argentine peso at a one-to-one parity with the US dollar by law. This required the Central Bank to hold US dollar reserves equal to the entire monetary base, severely limiting its ability to print money and credibly guaranteeing convertibility. The initial results were celebrated: inflation plummeted from over 2,300% in 1990 to single digits by 1994, restoring stability and attracting a surge of foreign investment.

However, by 1994, underlying vulnerabilities were becoming apparent. The fixed exchange rate eliminated monetary policy as a tool for economic adjustment, making the economy highly sensitive to external shocks. When the US Federal Reserve began raising interest rates in 1994, capital flows to emerging markets like Argentina reversed, triggering the "Tequila Crisis" that started in Mexico. While Argentina withstood this initial shock better than expected, it exposed the system's rigidity. The peso's overvaluation, exacerbated by using the strong US dollar as an anchor, began to hurt export competitiveness and widened the current account deficit.

Consequently, the Argentine economy in 1994 existed in a fragile equilibrium. The currency regime had successfully delivered price stability, fostering growth and confidence. Yet, it had also locked the country into a rigid framework that depended on continuous capital inflows and fiscal discipline to sustain the peg. The external shock of 1994 served as a warning sign that the sustainability of convertibility hinged on maintaining strict economic fundamentals and avoiding future global financial turbulence—a challenge that would define the coming years.

However, by 1994, underlying vulnerabilities were becoming apparent. The fixed exchange rate eliminated monetary policy as a tool for economic adjustment, making the economy highly sensitive to external shocks. When the US Federal Reserve began raising interest rates in 1994, capital flows to emerging markets like Argentina reversed, triggering the "Tequila Crisis" that started in Mexico. While Argentina withstood this initial shock better than expected, it exposed the system's rigidity. The peso's overvaluation, exacerbated by using the strong US dollar as an anchor, began to hurt export competitiveness and widened the current account deficit.

Consequently, the Argentine economy in 1994 existed in a fragile equilibrium. The currency regime had successfully delivered price stability, fostering growth and confidence. Yet, it had also locked the country into a rigid framework that depended on continuous capital inflows and fiscal discipline to sustain the peg. The external shock of 1994 served as a warning sign that the sustainability of convertibility hinged on maintaining strict economic fundamentals and avoiding future global financial turbulence—a challenge that would define the coming years.

💎 Extremely Rare