50 dinars (Constitution of the State of Kuwait) – Kuwait

Add to wishlist

Non-circulating coins

Commemoration: 50th Anniversary of the Enactment of the Constitution of the State of Kuwait (11th November 2012)

Kuwait

Context

Material

References

Numista: #100785

Value

Exchange value: 50 KWD

Obverse

Description:

Central Bank of Kuwait logo (a dhow sailing left). Kuwaiti flag and constitution. Signature of Emir Sheikh Sabah.

Inscription:

دَولَة الكوَيت بنكـ الكوَيت المركَزي

الذكرى الخَمسُون لِلمُصَادَقةِ عَلى دستُور دَولَة الكُويت

١٩٦٢ ~ ٢٠١١

أمير الكويت

صباح الأحمد الجابر الصباح

الدستور

٥٠

عَاماً

اليوبيل الذهَبي ١١ نوفمبر ٢٠١٢

الذكرى الخَمسُون لِلمُصَادَقةِ عَلى دستُور دَولَة الكُويت

١٩٦٢ ~ ٢٠١١

أمير الكويت

صباح الأحمد الجابر الصباح

الدستور

٥٠

عَاماً

اليوبيل الذهَبي ١١ نوفمبر ٢٠١٢

Translation:

State of Kuwait Central Bank of Kuwait

The Fiftieth Anniversary of the ratification of the Constitution of the State of Kuwait

1962 ~ 2011

The Amir of Kuwait

Sabah Al-Ahmad Al-Jaber Al-Sabah

The Constitution

50

Years

The Golden Jubilee 11 November 2012

The Fiftieth Anniversary of the ratification of the Constitution of the State of Kuwait

1962 ~ 2011

The Amir of Kuwait

Sabah Al-Ahmad Al-Jaber Al-Sabah

The Constitution

50

Years

The Golden Jubilee 11 November 2012

Language: Arabic

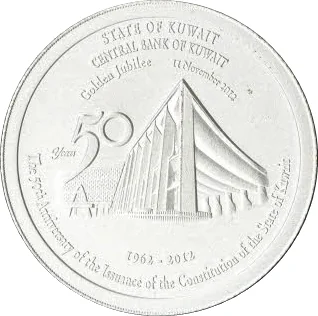

Reverse

Description:

Kuwait's National Assembly building

Inscription:

STATE OF KUWAIT

CENTRAL BANK OF KUWAIT

Golden Jubilee 11 November 2012

50

years

1962 - 2012

The 50th Anniversary of the Issuance of the Constitution of the State of Kuwait

CENTRAL BANK OF KUWAIT

Golden Jubilee 11 November 2012

50

years

1962 - 2012

The 50th Anniversary of the Issuance of the Constitution of the State of Kuwait

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Monnaie de Paris | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2012 | — | — | Proof |

Historical background

In 2012, Kuwait's currency situation was characterized by stability and strength, underpinned by its substantial oil wealth and massive sovereign wealth fund. The Kuwaiti Dinar (KWD) remained pegged to a weighted currency basket, a policy adopted in 2007 after abandoning its previous peg to the U.S. dollar. This basket, undisclosed in its exact composition but believed to be heavily weighted toward the dollar, provided the Central Bank of Kuwait (CBK) with greater flexibility to manage inflation and mitigate imported price pressures, which had been a significant concern during the earlier dollar-only peg period.

The primary monetary policy focus for the CBK in 2012 was maintaining low inflation and ensuring dinar stability amidst global economic uncertainty. Inflation was a manageable 3.2% for the year, allowing the CBK to keep its key discount rate at a historic low of 1.5% to support domestic economic activity. The dinar's strength was evident, as it consistently traded as one of the world's highest-valued currency units. This robust valuation was a direct reflection of Kuwait's persistent budget and current account surpluses, fueled by high average oil prices above $100 per barrel throughout the year.

However, the currency's stability existed within a broader context of regional monetary discussions. The long-stalled project for a single Gulf Cooperation Council (GCC) currency remained a topic of dialogue, though by 2012 it was effectively dormant due to political and economic divergences among member states, notably Oman and the UAE's withdrawal from the project. Consequently, Kuwait continued to prioritize its independent basket peg, which had successfully provided a buffer against external shocks, over any immediate moves toward regional monetary union. The overall picture in 2012 was one of a wealthy, oil-rich state successfully utilizing its monetary policy tools to ensure price stability and confidence in its national currency.

The primary monetary policy focus for the CBK in 2012 was maintaining low inflation and ensuring dinar stability amidst global economic uncertainty. Inflation was a manageable 3.2% for the year, allowing the CBK to keep its key discount rate at a historic low of 1.5% to support domestic economic activity. The dinar's strength was evident, as it consistently traded as one of the world's highest-valued currency units. This robust valuation was a direct reflection of Kuwait's persistent budget and current account surpluses, fueled by high average oil prices above $100 per barrel throughout the year.

However, the currency's stability existed within a broader context of regional monetary discussions. The long-stalled project for a single Gulf Cooperation Council (GCC) currency remained a topic of dialogue, though by 2012 it was effectively dormant due to political and economic divergences among member states, notably Oman and the UAE's withdrawal from the project. Consequently, Kuwait continued to prioritize its independent basket peg, which had successfully provided a buffer against external shocks, over any immediate moves toward regional monetary union. The overall picture in 2012 was one of a wealthy, oil-rich state successfully utilizing its monetary policy tools to ensure price stability and confidence in its national currency.

✨ Legendary