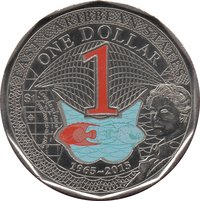

1 dollar (Eastern Caribbean Currency) – Eastern Caribbean States

Add to wishlist

Circulating commemorative coins

Commemoration: 50th Anniversary of Eastern Caribbean Currency

Context

Year: 2015

Issuer: Eastern Caribbean States

Issuing organization: Eastern Caribbean Central Bank

Ruler: Elizabeth II

Currency:

(since 1965)

Total mintage: 1,000,000

Material

References

KM: #

Numista: #78374

Value

Exchange value: 1 XCD

Obverse

Description:

Queen Elizabeth II facing right.

Inscription:

QUEEN ELIZABETH THE SECOND

IRB

IRB

Script: Latin

Engraver: Ian Rank-Broadley

Reverse

Description:

Red denomination above two fish. Queen Elizabeth II at lower right.

Inscription:

EAST CARIBBEAN STATES

ONE DOLLAR

$1

LEWARD ISLANDS

WINDWARD ISLANDS

1965-2015

ONE DOLLAR

$1

LEWARD ISLANDS

WINDWARD ISLANDS

1965-2015

Script: Latin

Edge

Alternating reeded and plain segments (4 each)

Mints

| Name | Mark |

|---|---|

| Royal Canadian Mint of Winnipeg | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2015 | — | 1,000,000 |

Historical background

In 2015, the eight member states of the Eastern Caribbean Currency Union (ECCU)—Anguilla, Antigua and Barbuda, Dominica, Grenada, Montserrat, Saint Kitts and Nevis, Saint Lucia, and Saint Vincent and the Grenadines—maintained their long-standing and stable peg of the Eastern Caribbean Dollar (XCD) at EC$2.70 to US$1. This fixed exchange rate regime, managed by the Eastern Caribbean Central Bank (ECCB) since 1976, provided a crucial anchor for price stability and investor confidence in these small, open, and tourism-dependent economies. The system's credibility was underscored by the backing of a foreign reserve pool, which historically held coverage well above the statutory minimum of 60% of demand liabilities.

The year saw the region continuing its recovery from the lingering effects of the 2008-09 global financial crisis and major natural disasters, with growth averaging approximately 2%. However, the currency union faced persistent structural challenges. Public debt levels remained critically high, averaging around 85% of GDP, constraining fiscal policy and posing a latent risk to the currency peg. Furthermore, the ECCB continued to advocate for deeper economic integration and structural reforms under its "Growth Agenda," emphasizing the need for improved competitiveness, debt reduction, and private sector development to ensure the long-term sustainability of the fixed exchange rate arrangement.

Despite these fiscal pressures, the XCD itself exhibited no signs of speculative pressure or devaluation in 2015. The ECCB maintained its strong commitment to the peg, which was widely viewed as a non-negotiable pillar of economic stability. The primary focus for monetary authorities was not on the exchange rate itself, but on fostering the economic resilience necessary to support it. Consequently, the year was characterized by monetary stability but underscored by ongoing concerns about fiscal vulnerabilities and the slow pace of growth-enhancing reforms within the currency union.

The year saw the region continuing its recovery from the lingering effects of the 2008-09 global financial crisis and major natural disasters, with growth averaging approximately 2%. However, the currency union faced persistent structural challenges. Public debt levels remained critically high, averaging around 85% of GDP, constraining fiscal policy and posing a latent risk to the currency peg. Furthermore, the ECCB continued to advocate for deeper economic integration and structural reforms under its "Growth Agenda," emphasizing the need for improved competitiveness, debt reduction, and private sector development to ensure the long-term sustainability of the fixed exchange rate arrangement.

Despite these fiscal pressures, the XCD itself exhibited no signs of speculative pressure or devaluation in 2015. The ECCB maintained its strong commitment to the peg, which was widely viewed as a non-negotiable pillar of economic stability. The primary focus for monetary authorities was not on the exchange rate itself, but on fostering the economic resilience necessary to support it. Consequently, the year was characterized by monetary stability but underscored by ongoing concerns about fiscal vulnerabilities and the slow pace of growth-enhancing reforms within the currency union.

🌟 Uncommon