100 Rupees – Seychelles

Non-circulating coins

Commemoration: F.A.O. - World Food Day

Seychelles

Context

Year: 1981

Issuer: Seychelles

Period:

(since 1976)

Currency:

(since 1914)

Demonetized: Yes

Total mintage: 10,000

Material

References

KM: #Click to copy to clipboard45a

Numista: #77591

Value

Exchange value: 100 SCR

Bullion value: $49.75

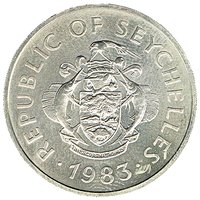

Obverse

Description:

Coat of arms with encircling legend and date beneath.

Inscription:

REPUBLIC OF SEYCHELLES

· 1981 ·

· 1981 ·

Script: Latin

Reverse

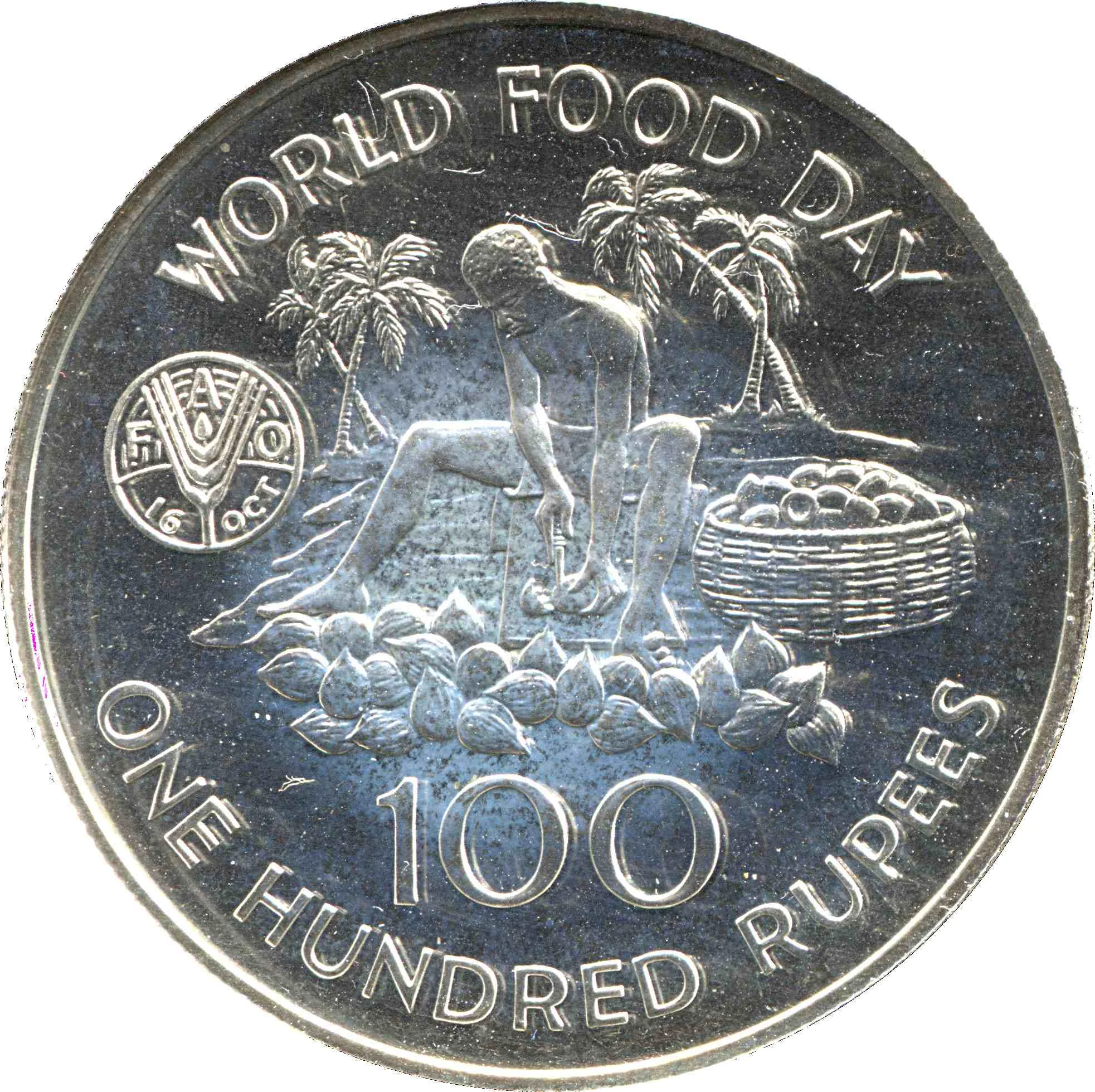

Description:

Man cutting coconuts, value below.

Inscription:

WORLD FOOD DAY

FAO

100

ONE HUNDRED RUPEES

FAO

100

ONE HUNDRED RUPEES

Script: Latin

Edge

Reeded

Categories

| Organization> FAO |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1981 | — | 10,000 | Proof |

Historical background

In 1981, the Seychelles economy was navigating a period of significant transition and strain under the one-party socialist government of France-Albert René, who had taken power in a 1977 coup. The state was pursuing a policy of economic diversification away from its traditional colonial-era plantation model, heavily investing in tourism, fisheries, and public sector expansion. However, these ambitions were constrained by a severe foreign exchange shortage, a common challenge for small island developing states. The country relied heavily on imports for food, fuel, and manufactured goods, but its export earnings from copra, cinnamon, and the nascent tourism industry were insufficient to cover the cost, leading to persistent balance of payments deficits.

The currency situation was defined by the Seychelles Rupee (SCR), which was pegged to a basket of currencies, primarily weighted towards the International Monetary Fund's Special Drawing Rights (SDR). This peg, managed by the Seychelles Monetary Authority (precursor to the Central Bank), was under constant pressure. To conserve scarce foreign reserves, the government maintained strict exchange controls, limiting the availability of foreign currency for businesses and citizens. This created a disconnect between the official exchange rate and the real value of the rupee, fostering a black market where hard currency traded at a significant premium.

Ultimately, 1981 represented a point of mounting economic tension that would intensify throughout the decade. The gap between official policy and market realities, combined with high public spending, set the stage for the more profound economic crises of the late 1980s. While not yet at the point of devaluation, the rigid controls and foreign exchange scarcity of 1981 highlighted the structural vulnerabilities of the Seychelles economy, foreshadowing the eventual move towards liberalization and a floating exchange rate many years later.

The currency situation was defined by the Seychelles Rupee (SCR), which was pegged to a basket of currencies, primarily weighted towards the International Monetary Fund's Special Drawing Rights (SDR). This peg, managed by the Seychelles Monetary Authority (precursor to the Central Bank), was under constant pressure. To conserve scarce foreign reserves, the government maintained strict exchange controls, limiting the availability of foreign currency for businesses and citizens. This created a disconnect between the official exchange rate and the real value of the rupee, fostering a black market where hard currency traded at a significant premium.

Ultimately, 1981 represented a point of mounting economic tension that would intensify throughout the decade. The gap between official policy and market realities, combined with high public spending, set the stage for the more profound economic crises of the late 1980s. While not yet at the point of devaluation, the rigid controls and foreign exchange scarcity of 1981 highlighted the structural vulnerabilities of the Seychelles economy, foreshadowing the eventual move towards liberalization and a floating exchange rate many years later.

💎 Very Rare