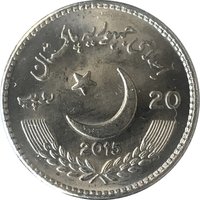

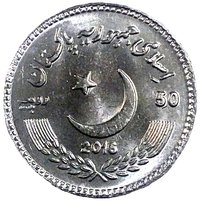

20 Rupees – Pakistan

Non-circulating coins

Commemoration: Pakistan-China Year of Friendly Exchange

Pakistan

Context

Material

Diameter: 27.5 mm

Weight: 10 g

Thickness: 2.35 mm

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #Click to copy to clipboard76

Numista: #71144

Value

Exchange value: 20 PKR

Obverse

Description:

Crescent, star, and date.

Inscription:

اسلامی جمہوریہ پاکستان

20 روپیہ

2015

20 روپیہ

2015

Translation:

Islamic Republic of Pakistan

20 Rupees

2015

20 Rupees

2015

Language: Urdu

Reverse

Description:

Flags of China and Pakistan centered, encircled by text, with a dot below.

Inscription:

YEAR OF FRIENDLY EXCHANGE 2015

Edge

Reeded

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2015 | — | 50,000 |

Historical background

In 2015, Pakistan's currency, the Pakistani Rupee (PKR), operated under a managed float regime but faced significant downward pressure. The year was characterized by relative stability in the exchange rate against the US Dollar, with the State Bank of Pakistan (SBP) actively intervening to curb excessive volatility. The PKR traded in a narrow band, closing the year at approximately PKR 104.5-105.5 per USD, a modest depreciation from around PKR 101 at the start of the year. This stability was largely artificial, propped up by SBP interventions and inflows from multilateral institutions, rather than being driven by strong economic fundamentals.

Underlying this superficial calm were persistent structural weaknesses that threatened the currency's value. Key challenges included a widening trade deficit, sluggish export growth, and declining foreign exchange reserves, which fell to concerning levels by mid-year. Political uncertainty and ongoing security operations also dampened investor confidence. However, these pressures were partially offset by several positive developments, most notably the sharp decline in global oil prices, which substantially reduced the import bill and the current account deficit. Furthermore, the commencement of the China-Pakistan Economic Corridor (CPEC) project began to attract anticipated investment flows, providing psychological support to the currency.

Consequently, 2015 represented a period of contained fragility. The SBP successfully maintained exchange rate stability in the short term, but this came at the cost of depleting reserves and masking deeper economic vulnerabilities. The situation created a policy dilemma, setting the stage for future adjustments. The managed stability of 2015 was ultimately unsustainable, as the accumulating pressures would lead to a more pronounced depreciation of the rupee in the subsequent years when reserves could no longer support the interventionist policy.

Underlying this superficial calm were persistent structural weaknesses that threatened the currency's value. Key challenges included a widening trade deficit, sluggish export growth, and declining foreign exchange reserves, which fell to concerning levels by mid-year. Political uncertainty and ongoing security operations also dampened investor confidence. However, these pressures were partially offset by several positive developments, most notably the sharp decline in global oil prices, which substantially reduced the import bill and the current account deficit. Furthermore, the commencement of the China-Pakistan Economic Corridor (CPEC) project began to attract anticipated investment flows, providing psychological support to the currency.

Consequently, 2015 represented a period of contained fragility. The SBP successfully maintained exchange rate stability in the short term, but this came at the cost of depleting reserves and masking deeper economic vulnerabilities. The situation created a policy dilemma, setting the stage for future adjustments. The managed stability of 2015 was ultimately unsustainable, as the accumulating pressures would lead to a more pronounced depreciation of the rupee in the subsequent years when reserves could no longer support the interventionist policy.

🌱 Fairly Common