1 paʻanga – Tonga

Add to wishlist

Non-circulating coins

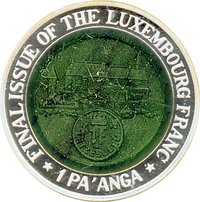

Commemoration: Final Issue of the Luxembourg Franc

Tonga

Context

Year: 2002

Issuer: Tonga

Issuing organization: National Reserve Bank of Tonga

Ruler: Tāufaʻāhau Tupou IV

Currency:

(since 1967)

Total mintage: 2,002

Material

Diameter: 40 mm

Weight: 31.1 g

Silver Weight:: 31.07 g

Shape: Round

Composition: 99.9% Silver

Standard: Silver ounce

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #71082

Value

Exchange value: 1 TOP

Bullion value: $75.61

Obverse

Reverse

Description:

1995 1 Franc coin featuring Burg Vianden, Luxembourg.

Inscription:

FINAL ISSUE OF THE LUXEMBOURG FRANC

1 PA'ANGA

1 PA'ANGA

Script: Latin

Edge

Plain

Categories

| Currency> Coin depiction |

| Building> Castle or fortification |

| Symbols> Coat of Arms |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2002 | — | 2,002 | Proof |

Historical background

In 2002, the Kingdom of Tonga was operating under a unique and long-standing currency arrangement. The national currency, the Pa'anga (TOP), was not freely convertible and was pegged to a basket of currencies, heavily weighted towards the Australian dollar, the New Zealand dollar, and the US dollar. This peg, managed by the National Reserve Bank of Tonga (NRBT), provided a crucial anchor for price stability and economic planning in a small, import-dependent island nation. However, it also meant that Tonga's monetary policy was largely reactive to the movements of these major currencies, limiting independent tools to manage domestic economic conditions.

The economy in the early 2000s was facing significant challenges that put pressure on this system. Tonga was recovering from a period of low growth and was heavily reliant on remittances from a large diaspora, export of squash, and a growing tourism sector. Fiscal deficits and a growing public debt burden were concerns, and the fixed exchange rate regime sometimes led to a perceived overvaluation of the Pa'anga. This overvaluation hurt the competitiveness of Tongan exports and encouraged imports, contributing to a persistent trade deficit. The currency peg also required careful management of foreign reserves to maintain confidence and defend the fixed rate.

Consequently, the currency situation in 2002 was one of stability on the surface, underpinned by the peg, but with underlying vulnerabilities. Discussions often centered on the sustainability of the peg in the face of external shocks and internal fiscal pressures. The focus for authorities was on maintaining sufficient foreign reserves, promoting export diversification to earn foreign exchange, and exercising fiscal discipline to support the fixed exchange rate regime—a system seen as essential for stability but requiring constant vigilance to maintain.

The economy in the early 2000s was facing significant challenges that put pressure on this system. Tonga was recovering from a period of low growth and was heavily reliant on remittances from a large diaspora, export of squash, and a growing tourism sector. Fiscal deficits and a growing public debt burden were concerns, and the fixed exchange rate regime sometimes led to a perceived overvaluation of the Pa'anga. This overvaluation hurt the competitiveness of Tongan exports and encouraged imports, contributing to a persistent trade deficit. The currency peg also required careful management of foreign reserves to maintain confidence and defend the fixed rate.

Consequently, the currency situation in 2002 was one of stability on the surface, underpinned by the peg, but with underlying vulnerabilities. Discussions often centered on the sustainability of the peg in the face of external shocks and internal fiscal pressures. The focus for authorities was on maintaining sufficient foreign reserves, promoting export diversification to earn foreign exchange, and exercising fiscal discipline to support the fixed exchange rate regime—a system seen as essential for stability but requiring constant vigilance to maintain.

✨ Legendary