1 real (Central Bank) – Brazil

Add to wishlist

Circulating commemorative coins

Commemoration: 40th Anniversary of Central Bank

Brazil

Context

Material

References

KM: #

Numista: #6439

Value

Exchange value: 1 BRL

Inflation-adjusted value: 3.00 BRL

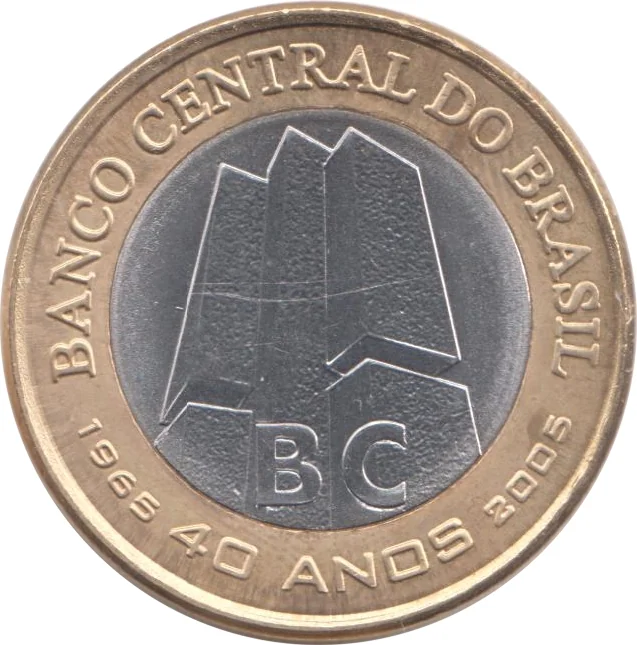

Obverse

Description:

Brazil's Central Bank building in Brasília, angled view showing "BC" inscription.

Inscription:

BANCO CENTRAL DO BRASIL

BC

1965 40 ANOS 2005

BC

1965 40 ANOS 2005

Translation:

CENTRAL BANK OF BRAZIL

BC

1965 40 YEARS 2005

BC

1965 40 YEARS 2005

Script: Latin

Language: Portuguese

Engraver: Glória A. Ferreira Dias

Reverse

Description:

Left: Diagonal lines highlight the face value, "REAL," and the year. Right: A sphere and belt with the Southern Cross allude to the national flag.

Inscription:

1

REAL

2005

REAL

2005

Script: Latin

Edge

Segmented reeding

Categories

| Building |

Mints

| Name | Mark |

|---|---|

| Casa da Moeda do Brasil | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2005 | — | 40,000,000 |

Historical background

In 2005, Brazil's currency situation was characterized by a period of significant appreciation of the Brazilian Real (BRL) against the US Dollar, continuing a strong trend that began in 2003. This appreciation was driven by a combination of high domestic interest rates, which attracted substantial foreign capital seeking yield, and a robust surge in global commodity prices that boosted Brazil's export revenues and trade surplus. The administration of President Luiz Inácio Lula da Silva maintained a commitment to fiscal discipline and inflation targeting, which bolstered investor confidence and further encouraged capital inflows.

However, this appreciation presented a complex policy dilemma for Brazilian authorities. While a stronger Real helped to curb imported inflation—a key goal for the Central Bank of Brazil (BCB) under its inflation-targeting regime—it also threatened the competitiveness of the country's manufacturing and export sectors by making Brazilian goods more expensive abroad. This "Dutch disease" dynamic sparked concern among industrial leaders and policymakers about potential deindustrialization. In response, the government implemented a series of capital controls and the BCB intervened in foreign exchange markets through direct purchases of dollars and the use of swap contracts to accumulate reserves and temper the pace of the Real's rise.

By the end of 2005, the Real had appreciated approximately 20% against the dollar over the previous two years. The overall situation was seen as a symptom of Brazil's successful macroeconomic stabilization but also highlighted its vulnerability to global financial flows. The accumulated foreign exchange reserves, which grew substantially during this period, provided a stronger buffer against external shocks, setting a precedent for active management of the currency that would continue in the years to follow.

However, this appreciation presented a complex policy dilemma for Brazilian authorities. While a stronger Real helped to curb imported inflation—a key goal for the Central Bank of Brazil (BCB) under its inflation-targeting regime—it also threatened the competitiveness of the country's manufacturing and export sectors by making Brazilian goods more expensive abroad. This "Dutch disease" dynamic sparked concern among industrial leaders and policymakers about potential deindustrialization. In response, the government implemented a series of capital controls and the BCB intervened in foreign exchange markets through direct purchases of dollars and the use of swap contracts to accumulate reserves and temper the pace of the Real's rise.

By the end of 2005, the Real had appreciated approximately 20% against the dollar over the previous two years. The overall situation was seen as a symptom of Brazil's successful macroeconomic stabilization but also highlighted its vulnerability to global financial flows. The accumulated foreign exchange reserves, which grew substantially during this period, provided a stronger buffer against external shocks, setting a precedent for active management of the currency that would continue in the years to follow.

🌱 Very Common