50 piastres – Egypt

Add to wishlist

Egypt

Context

Material

References

KM: #

Numista: #62815

Value

Exchange value: 0.50 EGP

Bullion value: $570.52

Obverse

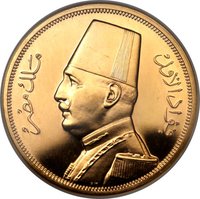

Inscription:

فؤاد الاول

ملك مصر

ملك مصر

Translation:

Fuad I

King of Egypt

King of Egypt

Script: Arabic

Language: Arabic

Engraver: Percy Metcalfe

Reverse

Edge

Mints

| Name | Mark |

|---|---|

| Royal Mint (Tower Hill) | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1930 | — | — | ||

| 1931 | — | — |

Historical background

In 1930, Egypt's currency situation was defined by its continued adherence to the gold standard, a system formalized in 1885 under British influence. The Egyptian pound (EE) was pegged to gold and, by extension, to the British pound sterling at a fixed parity. This arrangement provided significant stability and facilitated international trade, but it also tightly bound Egypt's economy to Britain's financial fortunes. The National Bank of Egypt, acting as the currency board, maintained full gold and foreign exchange backing for the notes in circulation, ensuring confidence in the currency but limiting discretionary monetary policy.

The global context, however, was one of severe strain. The onset of the Great Depression following the 1929 Wall Street Crash caused a dramatic fall in agricultural prices, particularly for cotton, which was the cornerstone of Egypt's economy. This precipitated a sharp decline in export revenues and created a severe balance of payments crisis. Deflationary pressures mounted, increasing the real burden of debt for landowners and the state, while the fixed exchange rate made Egyptian exports less competitive on the world market just as demand collapsed.

Consequently, 1930 became a year of intense debate and pressure. While some advocated for abandoning the gold standard to devalue the currency and provide economic relief, the government, led by Prime Minister Ismail Sidqi, and the financial establishment ultimately chose orthodoxy. They prioritized maintaining the pound's parity with sterling and the credibility of the gold-backed system, believing it essential for long-term stability and foreign investment. This decision meant that the adjustment to the Depression's shocks would come through painful internal deflation and austerity rather than exchange rate flexibility, a choice that had significant social and economic consequences in the years that followed.

The global context, however, was one of severe strain. The onset of the Great Depression following the 1929 Wall Street Crash caused a dramatic fall in agricultural prices, particularly for cotton, which was the cornerstone of Egypt's economy. This precipitated a sharp decline in export revenues and created a severe balance of payments crisis. Deflationary pressures mounted, increasing the real burden of debt for landowners and the state, while the fixed exchange rate made Egyptian exports less competitive on the world market just as demand collapsed.

Consequently, 1930 became a year of intense debate and pressure. While some advocated for abandoning the gold standard to devalue the currency and provide economic relief, the government, led by Prime Minister Ismail Sidqi, and the financial establishment ultimately chose orthodoxy. They prioritized maintaining the pound's parity with sterling and the credibility of the gold-backed system, believing it essential for long-term stability and foreign investment. This decision meant that the adjustment to the Depression's shocks would come through painful internal deflation and austerity rather than exchange rate flexibility, a choice that had significant social and economic consequences in the years that followed.

💎 Extremely Rare