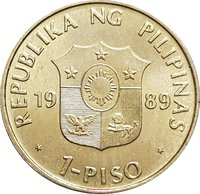

1 peso – Philippines

Add to wishlist

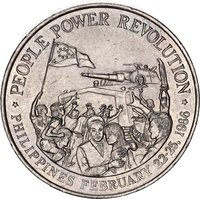

Circulating commemorative coins

Commemoration: Philippine Culture Decade

Philippines

Context

Year: 1989

Issuer: Philippines

Period:

(since 1946)

Currency:

(since 1967)

Demonetization: 1 May 2020

Total mintage: 10,005,000

Material

Diameter: 28.5 mm

Weight: 9.5 g

Thickness: 1.9 mm

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #6138

Value

Exchange value: 1 PHP

Obverse

Reverse

Edge

Reeded

Categories

| Geography> Mountain |

| Transportation> Watercraft |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| BSP Security Plant Complex | (PI) |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1989 | — | 10,000,000 | ||

| 1989 | — | 5,000 | Matte |

Historical background

In 1989, the Philippines was navigating a fragile economic recovery under the presidency of Corazon Aquino, following the turbulent Marcos dictatorship. The currency, the Philippine Peso (PHP), was managed under a controlled floating exchange rate system, heavily influenced by the Central Bank of the Philippines (CBP). However, the peso faced significant downward pressure, trading at approximately ₱21.50 to US$1 by year's end, a continuation of a long depreciation trend from ₱2 to the dollar in the early 1970s. This weakness stemmed from deep-seated structural issues: a massive external debt burden, persistent trade deficits, and low investor confidence due to political instability, including a series of coup attempts against the Aquino administration.

The Central Bank's policy was caught in a difficult balancing act. To defend the peso, it maintained high interest rates and intervened in the foreign exchange market, depleting international reserves. These tight monetary policies, however, stifled economic growth and made servicing the country's enormous foreign debt more expensive. Furthermore, the economy was still characterized by protectionist policies and crony capitalism, which limited competitiveness and foreign direct investment. Inflation remained a concern, eroding purchasing power and adding another layer of complexity to monetary management.

Ultimately, the currency situation of 1989 was a symptom of the broader post-Marcos economic challenges. While the government was implementing reforms under agreements with the International Monetary Fund (IMF) and World Bank, progress was slow. The peso's vulnerability reflected lingering doubts about the nation's political stability and its ability to achieve sustainable, export-led growth. This period set the stage for the more decisive liberalization and reforms of the 1990s, which aimed to stabilize the currency and integrate the Philippines more fully into the global economy.

The Central Bank's policy was caught in a difficult balancing act. To defend the peso, it maintained high interest rates and intervened in the foreign exchange market, depleting international reserves. These tight monetary policies, however, stifled economic growth and made servicing the country's enormous foreign debt more expensive. Furthermore, the economy was still characterized by protectionist policies and crony capitalism, which limited competitiveness and foreign direct investment. Inflation remained a concern, eroding purchasing power and adding another layer of complexity to monetary management.

Ultimately, the currency situation of 1989 was a symptom of the broader post-Marcos economic challenges. While the government was implementing reforms under agreements with the International Monetary Fund (IMF) and World Bank, progress was slow. The peso's vulnerability reflected lingering doubts about the nation's political stability and its ability to achieve sustainable, export-led growth. This period set the stage for the more decisive liberalization and reforms of the 1990s, which aimed to stabilize the currency and integrate the Philippines more fully into the global economy.

🌱 Common