1 lev – Bulgaria

Add to wishlist

Non-circulating coins

Commemoration: Bulgarian Iconography

Bulgaria

Context

Material

Diameter: 24.5 mm

Weight: 15.55 g

Gold Weight:: 15.53 g

Shape: Round

Composition: 99.9% Gold

Standard: Silver half ounce

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #60933

Value

Exchange value: 1 BGN

Bullion value: $2381.40

Obverse

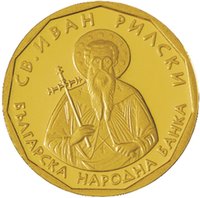

Description:

This coin, issued September 2, 2002, honors St. Ivan Rilsky (c. 876–946), Bulgaria’s first hermit and founder of its grandest monastery.

Inscription:

СВ. ИВАН РИЛСКИ

БЪЛГАРСКА НАРОДНА БАНКА

БЪЛГАРСКА НАРОДНА БАНКА

Translation:

ST. JOHN OF RILA

BULGARIAN NATIONAL BANK

BULGARIAN NATIONAL BANK

Script: Cyrillic

Language: Bulgarian

Engraver: Petar Stoikov

Reverse

Description:

Denomination, date.

Inscription:

1

2002

ЛЕВ

2002

ЛЕВ

Translation:

One Lev

2002

2002

Script: Cyrillic

Engraver: Petar Stoikov

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Bulgarian Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2002 | — | 2,000 |

Historical background

In 2002, Bulgaria was in a period of significant monetary stability, anchored by its unique currency board arrangement established in 1997 following a severe financial and hyperinflation crisis. The national currency, the lev (BGN), was firmly pegged at a fixed rate of 1,000 "old" lev to 1 Deutsche Mark, a parity that was seamlessly transferred to 1.95583 new lev per euro upon Germany's adoption of the common European currency in 1999. This currency board strictly mandated that every lev in circulation be fully backed by foreign reserves, primarily euros, eliminating the central bank's discretionary monetary policy and imposing rigorous fiscal discipline.

This framework had successfully tamed inflation and restored confidence, but by 2002 it also presented specific challenges and debates. While the economy was stabilizing and growing, the rigid peg limited tools for adjusting to economic shocks and kept interest rates higher than the eurozone average. Furthermore, the country's strategic goal of European Union accession—achieved in 2007—made eventual Eurozone membership a key objective. Therefore, the central discussion in 2002 was not about the stability of the lev, which was unquestioned, but about the pathway and timing for eventually replacing it with the euro.

Consequently, the currency situation in 2002 was one of a successful but transitional stability. The lev operated as a de facto proxy for the euro, providing a bedrock for economic planning and foreign investment. The focus for policymakers had shifted from crisis management to long-term integration, laying the technical and institutional groundwork to meet the Maastricht criteria and prepare for the future adoption of the euro, a process that would, however, take nearly two more decades to complete.

This framework had successfully tamed inflation and restored confidence, but by 2002 it also presented specific challenges and debates. While the economy was stabilizing and growing, the rigid peg limited tools for adjusting to economic shocks and kept interest rates higher than the eurozone average. Furthermore, the country's strategic goal of European Union accession—achieved in 2007—made eventual Eurozone membership a key objective. Therefore, the central discussion in 2002 was not about the stability of the lev, which was unquestioned, but about the pathway and timing for eventually replacing it with the euro.

Consequently, the currency situation in 2002 was one of a successful but transitional stability. The lev operated as a de facto proxy for the euro, providing a bedrock for economic planning and foreign investment. The focus for policymakers had shifted from crisis management to long-term integration, laying the technical and institutional groundwork to meet the Maastricht criteria and prepare for the future adoption of the euro, a process that would, however, take nearly two more decades to complete.

💎 Extremely Rare