100 Pesos – Mexico

Non-circulating coins

Commemoration: Bullion Coinage - Pre-Columbian Teotihuacan Series

Mexico

Context

Material

Diameter: 34.5 mm

Weight: 31.1 g

Gold weight: 31.07 g

Shape: Round

Composition: 99.9% Gold

Standard: Silver ounce

Magnetic: No

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #Click to copy to clipboard626

Numista: #57095

Value

Exchange value: 100 MXN = $5.82

Bullion value: $5180.13

Inflation-adjusted value: 517.28 MXN

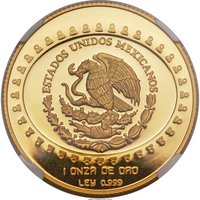

Obverse

Reverse

Edge

Reeded

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1997 | Mo | 500 | ||

| 1997 | Mo | 206 | Proof |

Historical background

In 1997, Mexico's currency, the peso, was in a period of relative stability, a notable achievement following the profound Tequila Crisis of 1994-1995. That earlier crisis had forced a sudden devaluation, led to a deep recession, and required a massive $50 billion international bailout. By 1997, the economy was recovering, with growth returning and inflation beginning to decline from its crisis peak. This stability was underpinned by a floating exchange rate regime, adopted in late 1994, which allowed the peso's value to be set by the market, and a new monetary policy framework focused on inflation targeting, established by an increasingly autonomous Bank of Mexico.

However, this stability remained fragile and was tested by external shocks. The Asian Financial Crisis, which erupted in mid-1997, triggered volatility in emerging markets worldwide. While Mexico was not as directly exposed as Asian economies, investor nervousness led to capital outflows and pressure on the peso. The government and central bank were forced to defend the currency through interest rate hikes, which raised borrowing costs and threatened to slow the ongoing economic recovery. This period highlighted Mexico's continued vulnerability to global capital flow reversals despite its improved fundamentals.

Ultimately, the policies established after the 1994 crisis proved resilient. The floating peso acted as a shock absorber, adjusting to market pressures without exhausting foreign reserves in a futile defense of a fixed rate. The commitment to fiscal discipline and transparent monetary policy, communicated by the newly independent central bank, helped maintain investor confidence. Consequently, while experiencing volatility, Mexico avoided a repeat of the catastrophic devaluation of 1994, navigating the 1997 turbulence and setting a foundation for the inflation-targeting regime that would define its monetary policy in the coming decades.

However, this stability remained fragile and was tested by external shocks. The Asian Financial Crisis, which erupted in mid-1997, triggered volatility in emerging markets worldwide. While Mexico was not as directly exposed as Asian economies, investor nervousness led to capital outflows and pressure on the peso. The government and central bank were forced to defend the currency through interest rate hikes, which raised borrowing costs and threatened to slow the ongoing economic recovery. This period highlighted Mexico's continued vulnerability to global capital flow reversals despite its improved fundamentals.

Ultimately, the policies established after the 1994 crisis proved resilient. The floating peso acted as a shock absorber, adjusting to market pressures without exhausting foreign reserves in a futile defense of a fixed rate. The commitment to fiscal discipline and transparent monetary policy, communicated by the newly independent central bank, helped maintain investor confidence. Consequently, while experiencing volatility, Mexico avoided a repeat of the catastrophic devaluation of 1994, navigating the 1997 turbulence and setting a foundation for the inflation-targeting regime that would define its monetary policy in the coming decades.

✨ Legendary