1 rupee (JayaPrakash Narayan) – India

Add to wishlist

Circulating commemorative coins

Commemoration: 100th Anniversary Birth of JayaPrakash Narayan

India

Material

Diameter: 25 mm

Weight: 4.95 g

Thickness: 1.5 mm

Shape: Round

Composition: Stainless steel

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #5680

Value

Exchange value: 1 INR

Inflation-adjusted value: 4.22 INR

Obverse

Description:

Asoka lion with denomination.

Inscription:

भारत INDIA

सत्यमेव जयते

रुपया 1 RUPEE

सत्यमेव जयते

रुपया 1 RUPEE

Translation:

INDIA

Truth Alone Triumphs

1 RUPEE

Truth Alone Triumphs

1 RUPEE

Scripts: Devanagari, Latin

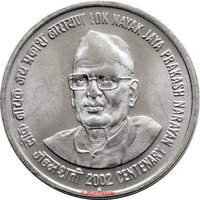

Reverse

Description:

Jayaprakash Narayan bust.

Inscription:

लोक नायक जय प्रकाश नारायण

LOK NAYAK JAYA PRAKASH NARAYAN

जन्मशती 2002 CENTENARY

LOK NAYAK JAYA PRAKASH NARAYAN

जन्मशती 2002 CENTENARY

Translation:

Lok Nayak Jaya Prakash Narayan

Centenary 2002

Centenary 2002

Scripts: Devanagari, Latin

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Mumbai / Bombay | — |

| Hyderabad | ★ |

| Mumbai / Bombay | ♦ |

| Mumbai / Bombay | M |

Historical background

In 2002, India's currency landscape was characterized by a period of relative stability and consolidation following a decade of significant economic reforms. The Indian Rupee (INR) was on a managed float system, with its value broadly determined by market forces but with the Reserve Bank of India (RBI) actively intervening to curb excessive volatility. This year saw the rupee trading in a range of approximately 47 to 49 against the US dollar, reflecting a gentle depreciation pressure. This was largely influenced by global factors, including a strengthening dollar in the aftermath of the 9/11 attacks and heightened geopolitical tensions, as well as domestic concerns like a widening current account deficit and the fiscal impact of a severe drought.

The period was also notable for the continuing efforts to modernize the financial system and promote currency stability. The RBI maintained a focus on building foreign exchange reserves, which grew steadily throughout the year, providing a robust buffer against external shocks. This reserve accumulation was aided by strong inflows from software exports and remittances from non-resident Indians (NRIs). Furthermore, 2002 fell within a multi-year phase of "capital account convertibility" being a topic of careful debate, with authorities proceeding cautiously to liberalize controls on foreign investment while safeguarding against sudden capital flight.

Overall, 2002 represented a year of cautious management rather than dramatic change. The currency regime successfully navigated external uncertainties without a crisis, providing a stable platform for economic growth. The focus remained on maintaining macroeconomic stability, controlling inflation, and gradually integrating with the global economy—a steady approach that laid groundwork for the stronger growth and significant foreign investment inflows that would follow in the coming years.

The period was also notable for the continuing efforts to modernize the financial system and promote currency stability. The RBI maintained a focus on building foreign exchange reserves, which grew steadily throughout the year, providing a robust buffer against external shocks. This reserve accumulation was aided by strong inflows from software exports and remittances from non-resident Indians (NRIs). Furthermore, 2002 fell within a multi-year phase of "capital account convertibility" being a topic of careful debate, with authorities proceeding cautiously to liberalize controls on foreign investment while safeguarding against sudden capital flight.

Overall, 2002 represented a year of cautious management rather than dramatic change. The currency regime successfully navigated external uncertainties without a crisis, providing a stable platform for economic growth. The focus remained on maintaining macroeconomic stability, controlling inflation, and gradually integrating with the global economy—a steady approach that laid groundwork for the stronger growth and significant foreign investment inflows that would follow in the coming years.

🌱 Common