100 escudos – Cape Verde

Add to wishlist

Circulating commemorative coins

Commemoration: Bird Fauna of Cabo Verde Islands Series - Raso Lark

Cape Verde

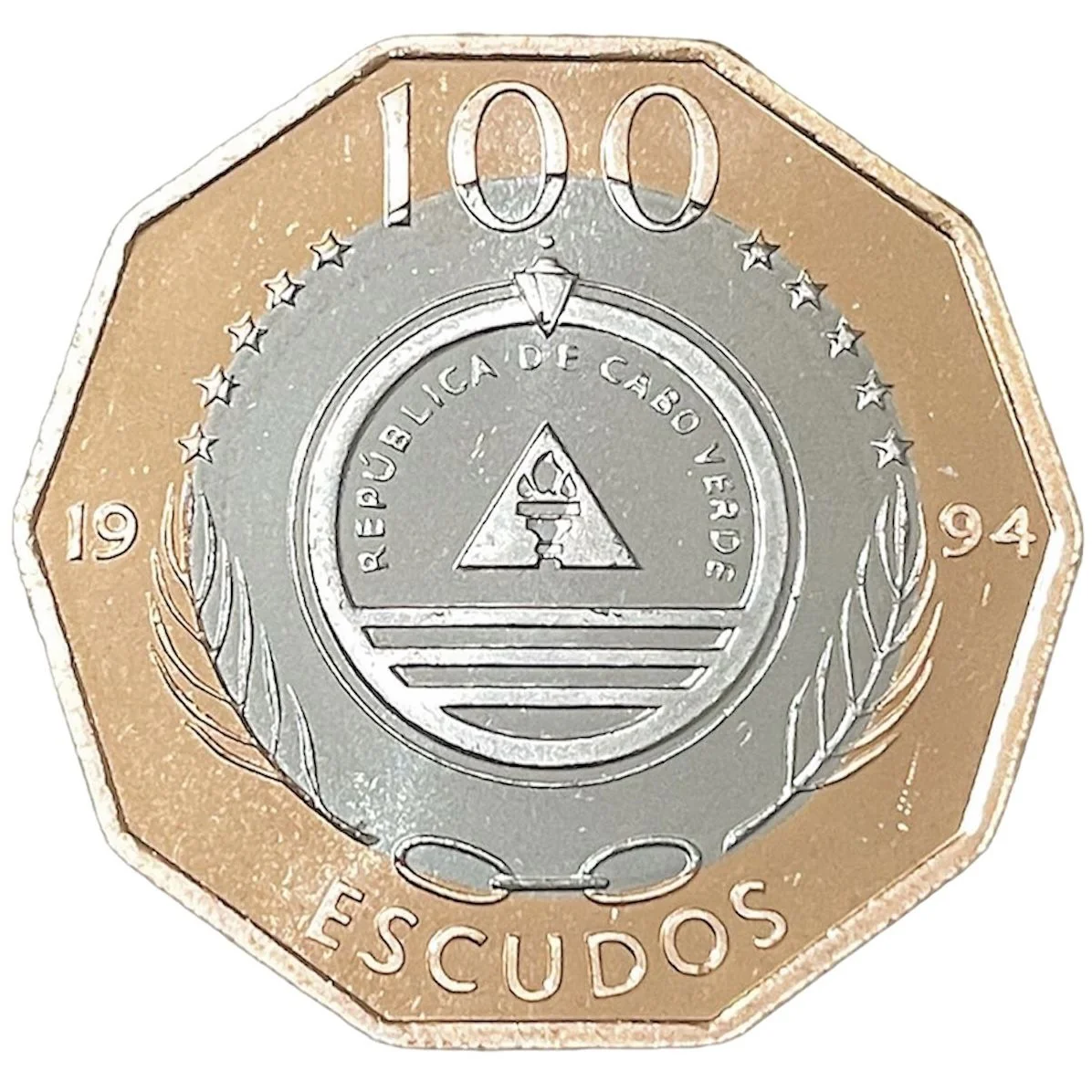

Obverse

Description:

National emblem divides date and denomination above, value below.

Inscription:

100

REPÚBLICA DE CABO VERDE

19 94

ESCUDOS

REPÚBLICA DE CABO VERDE

19 94

ESCUDOS

Translation:

Republic of Cape Verde

19 94

Escudos

19 94

Escudos

Script: Latin

Language: Portuguese

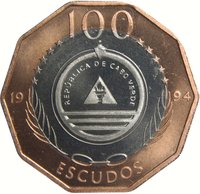

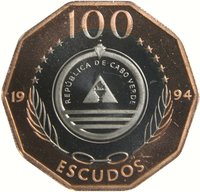

Reverse

Description:

Raza Lark circled.

Inscription:

Alauda razae Alexander

CALHANDRA DO ILHÉU RASO

CALHANDRA DO ILHÉU RASO

Translation:

The Lark of Raso Island Alexander

Script: Latin

Language: Portuguese

Edge

Reeded

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1994 | — | — |

Historical background

In 1994, the currency situation in Cape Verde was defined by stability and a firm peg to an international basket, a notable achievement for a small, resource-scarce island nation. The country's currency, the Cape Verdean escudo (CVE), was not freely convertible and its value was officially fixed by the Banco de Cabo Verde. This peg was not to a single currency but to a weighted basket of currencies belonging to its main trading partners, with the Portuguese escudo holding a predominant share. This linkage provided a crucial anchor for prices and trade, fostering macroeconomic stability in an economy heavily dependent on imports, tourism, and remittances.

This monetary framework was a legacy of the country's historical ties to Portugal and a deliberate policy choice following independence in 1975. The fixed exchange rate regime required disciplined fiscal and monetary policies to maintain, as the central bank had to hold sufficient foreign exchange reserves to defend the peg. By 1994, this approach had largely succeeded in controlling inflation and building confidence, both domestically and with international financial institutions. However, it also meant Cape Verde relinquished independent monetary policy, and its economy remained vulnerable to external shocks affecting its anchor currencies and trade flows.

The context of 1994 was one of cautious economic liberalization and engagement with the global community. The currency peg was seen as a cornerstone for attracting foreign investment and development aid, which were vital for growth. While the system provided stability, it also imposed constraints, implicitly setting the stage for future discussions about monetary policy flexibility. Within a decade, these discussions would lead to a significant shift, as Cape Verde would later move to peg the escudo solely to the euro, reflecting Portugal's own adoption of the single European currency and the deepening of EU-Cape Verde relations.

This monetary framework was a legacy of the country's historical ties to Portugal and a deliberate policy choice following independence in 1975. The fixed exchange rate regime required disciplined fiscal and monetary policies to maintain, as the central bank had to hold sufficient foreign exchange reserves to defend the peg. By 1994, this approach had largely succeeded in controlling inflation and building confidence, both domestically and with international financial institutions. However, it also meant Cape Verde relinquished independent monetary policy, and its economy remained vulnerable to external shocks affecting its anchor currencies and trade flows.

The context of 1994 was one of cautious economic liberalization and engagement with the global community. The currency peg was seen as a cornerstone for attracting foreign investment and development aid, which were vital for growth. While the system provided stability, it also imposed constraints, implicitly setting the stage for future discussions about monetary policy flexibility. Within a decade, these discussions would lead to a significant shift, as Cape Verde would later move to peg the escudo solely to the euro, reflecting Portugal's own adoption of the single European currency and the deepening of EU-Cape Verde relations.

🌱 Common