500 rials – Yemen

Add to wishlist

Non-circulating coins

Commemoration: Sana'a 2004 the Arab Cultural Capital

Yemen

Context

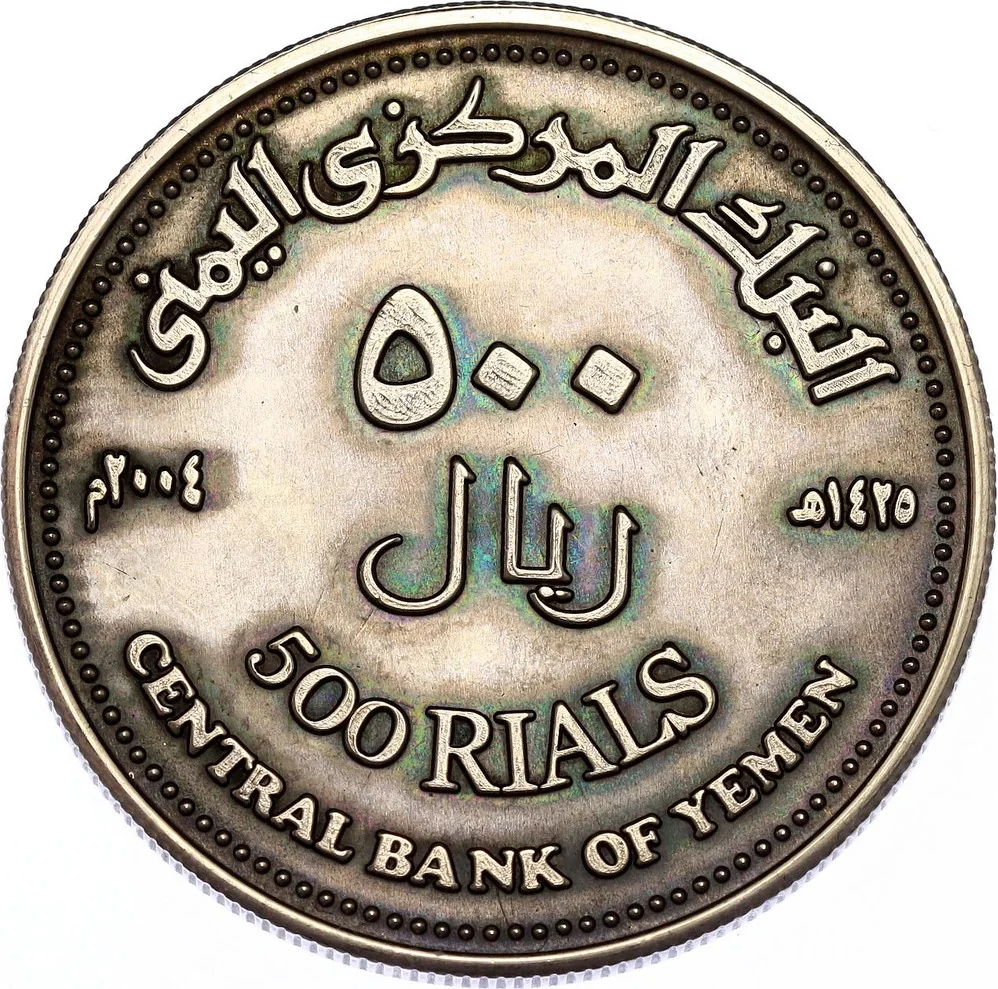

Year: 2004

Islamic (Hijri) Year:: 1425

Issuer: Yemen

Issuing organization: Central Bank of Yemen

Period:

(since 1990)

Currency:

(since 1990)

Material

Diameter: 35.2 mm

Weight: 21.25 g

Shape: Round

Composition: Nickel brass

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #55561

Value

Exchange value: 500 YER

Obverse

Reverse

Edge

Reeded

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2004 | — | — |

Historical background

In 2004, Yemen's currency, the Yemeni rial (YER), operated within a fragile economic and political context that foreshadowed the severe crises to come. The country was grappling with long-standing structural issues: declining oil production, which accounted for the majority of government revenue and exports, a rapidly growing population, widespread poverty, and significant corruption. While not yet in freefall, the rial faced persistent pressure, and the Central Bank of Yemen struggled to maintain stability through managed depreciation and limited foreign exchange reserves. The economic environment was one of underlying vulnerability, heavily dependent on a finite resource and with limited diversification.

Politically, the year was marked by rising internal tensions that would later have direct monetary consequences. The government of President Ali Abdullah Saleh was engaged in an escalating conflict with Houthi rebels in the northern Saada Governorate, a confrontation that began in 2004 and is known as the Sa'dah War. This conflict began to divert substantial public funds away from development and into military expenditures, increasing fiscal strain. Furthermore, the implementation of economic reforms mandated by international donors, including subsidy reductions and efforts to curb money laundering, often proceeded unevenly and faced public resistance, creating an uncertain policy environment.

Overall, the currency situation in 2004 can be characterized as one of managed stability masking profound fragility. The rial's value was officially maintained, but the foundations of the economy were eroding. The twin pressures of dwindling oil income and the nascent, costly conflict in the north set the stage for future instability, long before the profound shocks of the 2011 uprising and the subsequent civil war would fracture the country's financial institutions and lead to the emergence of competing central banks and multiple exchange rates in the following decade.

Politically, the year was marked by rising internal tensions that would later have direct monetary consequences. The government of President Ali Abdullah Saleh was engaged in an escalating conflict with Houthi rebels in the northern Saada Governorate, a confrontation that began in 2004 and is known as the Sa'dah War. This conflict began to divert substantial public funds away from development and into military expenditures, increasing fiscal strain. Furthermore, the implementation of economic reforms mandated by international donors, including subsidy reductions and efforts to curb money laundering, often proceeded unevenly and faced public resistance, creating an uncertain policy environment.

Overall, the currency situation in 2004 can be characterized as one of managed stability masking profound fragility. The rial's value was officially maintained, but the foundations of the economy were eroding. The twin pressures of dwindling oil income and the nascent, costly conflict in the north set the stage for future instability, long before the profound shocks of the 2011 uprising and the subsequent civil war would fracture the country's financial institutions and lead to the emergence of competing central banks and multiple exchange rates in the following decade.

💎 Extremely Rare