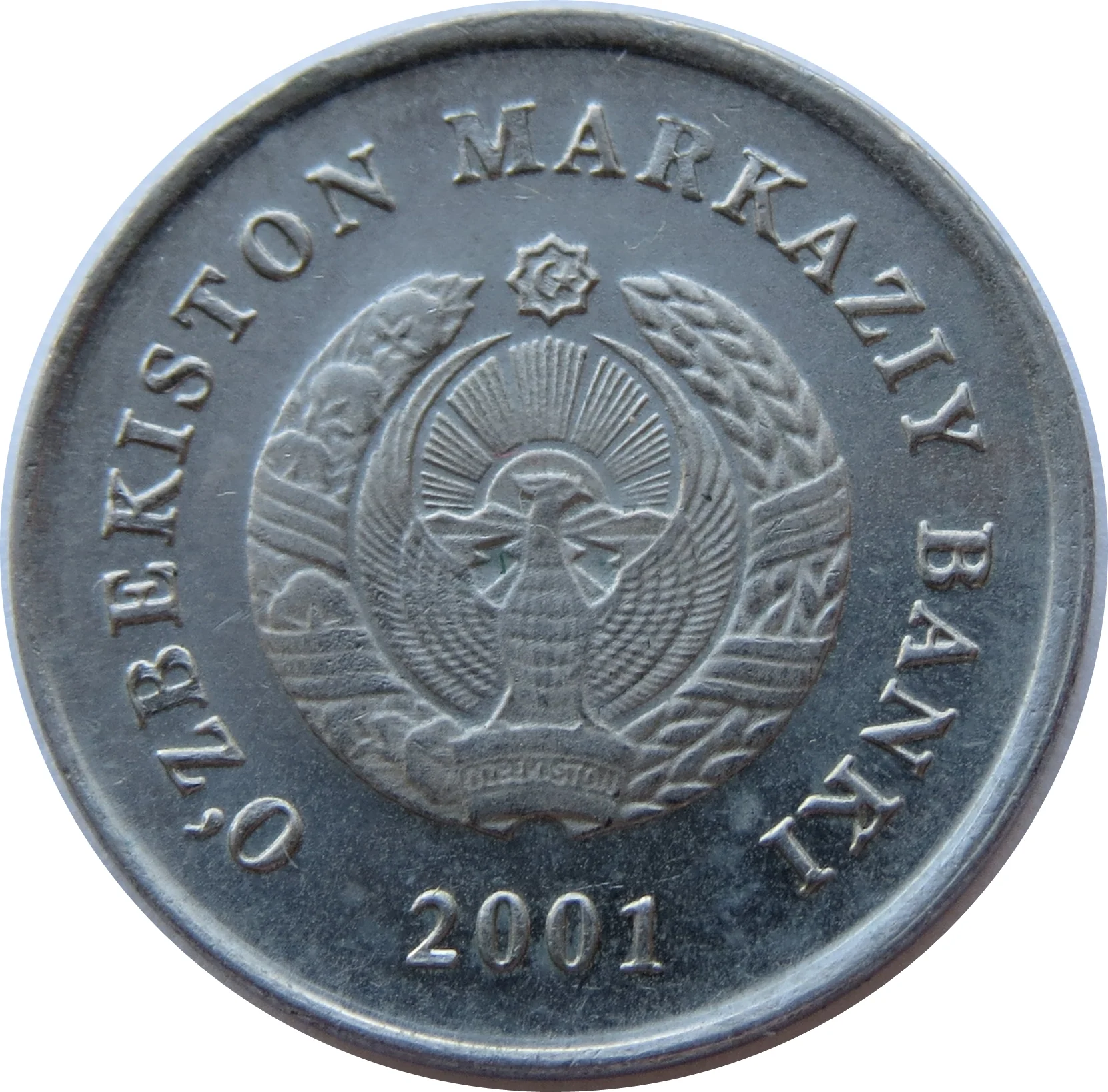

10 Soʻm – Uzbekistan

Uzbekistan

Context

Year: 2001

Issuer: Uzbekistan

Period:

(since 1991)

Currency:

(since 1994)

Demonetization: 1 March 2020

Material

References

KM: #Click to copy to clipboard14

Numista: #5555

Value

Exchange value: 10 UZS

Obverse

Reverse

Edge

Plain

Categories

| Animal> Bird |

| Mythology> Fantastic animal |

| Symbols> Coat of Arms |

| Map |

| Symbol> Sun |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2001 | — | — |

Historical background

In 2001, Uzbekistan's currency situation was characterized by a complex and restrictive system of multiple exchange rates, a legacy of the post-Soviet transition. The official exchange rate of the Uzbekistani som (UZS) was set by the Central Bank of Uzbekistan at an artificially high level, approximately 325 som to the US dollar. However, this rate was largely inaccessible for most citizens and businesses. A thriving black market existed where the som traded at a significantly depreciated rate, often around 1,000 to 1,200 som per dollar, reflecting the currency's true market value and the scarcity of hard currency.

This multi-tiered system created severe economic distortions. It discouraged foreign investment, as profits could not be repatriated at a realistic rate, and crippled legitimate import-export activity. The gap between the official and black-market rates fostered widespread corruption, as access to dollars at the official rate became a lucrative privilege. Furthermore, the government maintained strict currency controls, requiring most hard currency earnings from key exports like cotton and gold to be surrendered to the state at the unfavorable official rate, stifling economic growth and creating shortages of goods.

The year 2001 did not see a major reform of this system, as the government prioritized stability and control over liberalization. However, international financial institutions, notably the IMF, continued to pressure Tashkent to unify its exchange rates and move towards convertibility as a prerequisite for broader economic reform and assistance. The entrenched currency regime remained a primary obstacle to Uzbekistan's integration into the global economy, perpetuating an inefficient and opaque economic environment that would persist for several more years before incremental reforms began.

This multi-tiered system created severe economic distortions. It discouraged foreign investment, as profits could not be repatriated at a realistic rate, and crippled legitimate import-export activity. The gap between the official and black-market rates fostered widespread corruption, as access to dollars at the official rate became a lucrative privilege. Furthermore, the government maintained strict currency controls, requiring most hard currency earnings from key exports like cotton and gold to be surrendered to the state at the unfavorable official rate, stifling economic growth and creating shortages of goods.

The year 2001 did not see a major reform of this system, as the government prioritized stability and control over liberalization. However, international financial institutions, notably the IMF, continued to pressure Tashkent to unify its exchange rates and move towards convertibility as a prerequisite for broader economic reform and assistance. The entrenched currency regime remained a primary obstacle to Uzbekistan's integration into the global economy, perpetuating an inefficient and opaque economic environment that would persist for several more years before incremental reforms began.

🌱 Very Common