200 kroner (Henrik Wergeland) – Norway

Add to wishlist

Non-circulating coins

Commemoration: 200th Anniversary of the Birth of Henrik Wergeland

Norway

Context

Material

References

KM: #

Numista: #52129

Value

Exchange value: 200 NOK

Bullion value: $38.90

Inflation-adjusted value: 320.72 NOK

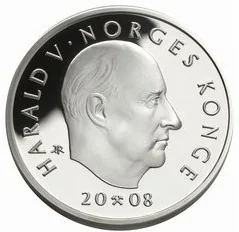

Obverse

Description:

King Harald V bust facing right. Engraver's initials behind bust. Inscription surrounds. Date split by mintmark below. Solid rim ring.

Inscription:

HARALD V · NORGES KONGE

IAR

20 ⚒ 08

IAR

20 ⚒ 08

Translation:

Harald V, Norway's King

IAR

20 08

IAR

20 08

Script: Latin

Engraver: Ingrid Austlid Rise

Reverse

Description:

Henrik Wergeland's glasses and signature. The coin's surface is split, with one part resembling billowing paper. Value under glasses, designer's initials below, signature on right. Solid rim.

Inscription:

Henrik Wergeland

200 KR

EF.

200 KR

EF.

Scripts: Latin, Latin (cursive)

Engraver: Ingrid Austlid Rise

Designer: Enzo Finger

Edge

Plain

Categories

| Event> Birth anniversary |

Mints

| Name | Mark |

|---|---|

| Norwegian Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2008 | — | 29,646 | Proof |

Historical background

In 2008, Norway's currency situation was defined by its stark contrast to the global financial crisis unfolding elsewhere. While many economies faced severe distress, Norway entered the period with exceptional fundamental strengths: vast sovereign wealth from oil and gas exports (the Government Pension Fund Global), large budget and current account surpluses, low public debt, and a robustly capitalized banking system. Consequently, the Norwegian krone (NOK) was traditionally seen as a stable and resilient currency, often influenced more by oil prices and domestic interest rate decisions than by global financial panic.

However, the krone experienced significant volatility as the crisis intensified in the autumn of 2008. Following the collapse of Lehman Brothers, a global rush for liquidity and safe-haven assets led to a dramatic appreciation of currencies like the US dollar and Japanese yen. The NOK, considered a riskier commodity currency, sold off sharply despite Norway's strong fundamentals. From September to October, the krone depreciated by approximately 30% against the euro, reflecting the extreme risk aversion and deleveraging in international markets that overwhelmed Norway's positive economic backdrop.

In response, Norges Bank, the country's central bank, took aggressive action to stabilize markets and the economy. It implemented a series of emergency interest rate cuts, slashing its key policy rate from 5.75% in September to a historic low of 1.25% by June 2009. Additionally, it provided extraordinary liquidity to ensure the functioning of the domestic money and foreign exchange markets. These measures, combined with a swift government fiscal stimulus and the eventual calming of global markets, helped the krone recover a substantial portion of its losses by the end of 2009, underscoring the temporary nature of the shock to Norway's otherwise solid financial position.

However, the krone experienced significant volatility as the crisis intensified in the autumn of 2008. Following the collapse of Lehman Brothers, a global rush for liquidity and safe-haven assets led to a dramatic appreciation of currencies like the US dollar and Japanese yen. The NOK, considered a riskier commodity currency, sold off sharply despite Norway's strong fundamentals. From September to October, the krone depreciated by approximately 30% against the euro, reflecting the extreme risk aversion and deleveraging in international markets that overwhelmed Norway's positive economic backdrop.

In response, Norges Bank, the country's central bank, took aggressive action to stabilize markets and the economy. It implemented a series of emergency interest rate cuts, slashing its key policy rate from 5.75% in September to a historic low of 1.25% by June 2009. Additionally, it provided extraordinary liquidity to ensure the functioning of the domestic money and foreign exchange markets. These measures, combined with a swift government fiscal stimulus and the eventual calming of global markets, helped the krone recover a substantial portion of its losses by the end of 2009, underscoring the temporary nature of the shock to Norway's otherwise solid financial position.

⭐ Rare