200 kroner (Norwegian Olympic and Paralympic Committee and Confederation of Sports) – Norway

Add to wishlist

Non-circulating coins

Commemoration: 150th Anniversary of the Norwegian Olympic and Paralympic Committee and Confederation of Sports

Norway

Context

Material

References

KM: #

Numista: #52126

Value

Exchange value: 200 NOK

Bullion value: $39.12

Inflation-adjusted value: 295.32 NOK

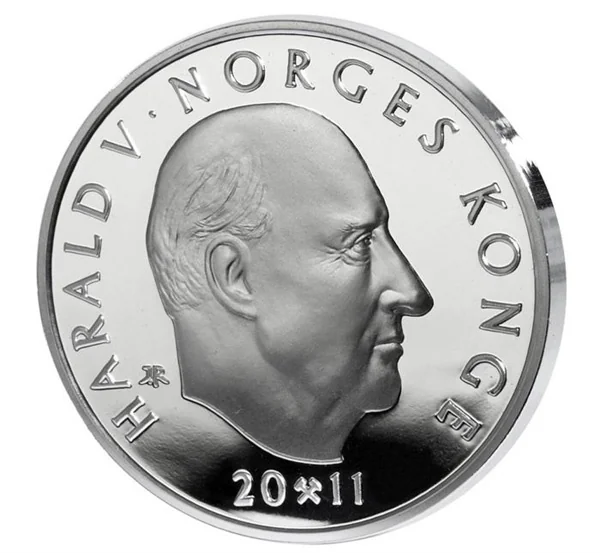

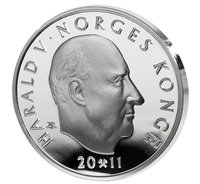

Obverse

Description:

King Harald V bust facing right. Engraver's initials behind bust. Inscription surrounds. Date split by mintmark below. Solid rim ring.

Inscription:

HARALD V · NORGES KONGE

IAR

20 ⚒ 11

IAR

20 ⚒ 11

Translation:

Harald V, Norway's King

IAR

20 11

IAR

20 11

Script: Latin

Engraver: Ingrid Austlid Rise

Reverse

Description:

The coin’s surface is split: a running track below, five sports above. Inscription top, designer's initials right, value bottom. Solid ring on the rim.

Inscription:

NORSK IDRETT 150 ÅR

IVK

200 KR

IVK

200 KR

Translation:

Norwegian Sports 150 Years

IVK

200 KR

IVK

200 KR

Script: Latin

Language: Norwegian

Engraver: Ingrid Austlid Rise

Designer: Ina Viktoria Kristiansen

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Norwegian Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2011 | — | 11,948 | Proof |

Historical background

In 2011, Norway's currency situation was dominated by the remarkable strength of the Norwegian krone (NOK), which reached its highest levels in decades against both the euro and a trade-weighted index. This surge was fundamentally driven by high global oil and gas prices, as Norway is a major energy exporter. The resulting large trade surpluses and substantial foreign currency inflows created sustained upward pressure on the krone, a phenomenon often referred to as "petro-currency" strength.

This strong krone presented a significant policy challenge, creating a pronounced two-speed economy. While the booming offshore energy sector and related industries thrived, the traditional export-oriented and tourism sectors, such as manufacturing and seafood, faced severe competitive pressure in international markets. Domestic industries also struggled against cheaper imports. Consequently, Norges Bank, the country's central bank, faced a complex balancing act: it needed to raise interest rates to cool a overheating domestic housing market and contain inflation, but higher rates would further attract foreign capital and strengthen the krone, exacerbating the problems for non-oil exporters.

In response, Norges Bank adopted a cautious and gradual approach to monetary tightening throughout 2011, often signalling that future rate hikes would be slower than previously anticipated to temper krone appreciation. Furthermore, the government continued its strict adherence to the "fiscal rule," which mandates that only the expected real return from the massive Government Pension Fund Global (the oil fund) be spent in the state budget. This self-imposed fiscal discipline helped to sterilize a portion of the petroleum revenues from the domestic economy, mitigating inflationary pressures and moderating, though not eliminating, the krone's ascent.

This strong krone presented a significant policy challenge, creating a pronounced two-speed economy. While the booming offshore energy sector and related industries thrived, the traditional export-oriented and tourism sectors, such as manufacturing and seafood, faced severe competitive pressure in international markets. Domestic industries also struggled against cheaper imports. Consequently, Norges Bank, the country's central bank, faced a complex balancing act: it needed to raise interest rates to cool a overheating domestic housing market and contain inflation, but higher rates would further attract foreign capital and strengthen the krone, exacerbating the problems for non-oil exporters.

In response, Norges Bank adopted a cautious and gradual approach to monetary tightening throughout 2011, often signalling that future rate hikes would be slower than previously anticipated to temper krone appreciation. Furthermore, the government continued its strict adherence to the "fiscal rule," which mandates that only the expected real return from the massive Government Pension Fund Global (the oil fund) be spent in the state budget. This self-imposed fiscal discipline helped to sterilize a portion of the petroleum revenues from the domestic economy, mitigating inflationary pressures and moderating, though not eliminating, the krone's ascent.

💎 Very Rare