⅕ Crown (American Numismatic Association) – Isle of Man

Non-circulating coins

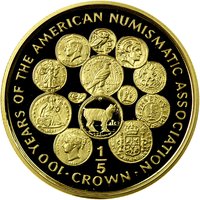

Commemoration: 100th Anniversary of the American Numismatic Association

Context

Year: 1991

Country: British Crown dependencies

Issuer: Isle of Man

Ruler: Elizabeth II

Currency:

(since 1970)

Material

References

KM: #Click to copy to clipboard290

Numista: #454572

Value

Bullion value: $1034.02

Obverse

Description:

Queen Elizabeth II facing right, wearing the George IV State Diadem, surrounded by legend and date.

Inscription:

ELIZABETH II ISLE OF MAN · 1991

RDM

PM

RDM

PM

Translation:

ELIZABETH II ISLE OF MAN · 1991

By the grace of God, Queen, Defender of the Faith

By the grace of God, Queen, Defender of the Faith

Script: Latin

Languages: English, Latin abbreviation

Designer: Raphael David Maklouf

Reverse

Description:

Cat encircled by coins.

Inscription:

100 YEARS OF THE AMERICAN NUMISMATIC ASSOCIATION

· 1/5 CROWN ·

· 1/5 CROWN ·

Script: Latin

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Pobjoy Mint | (PM) |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1991 | PM | — | Proof |

Historical background

In 1991, the Isle of Man's currency situation was defined by its unique constitutional position as a British Crown Dependency, which granted it autonomy in issuing its own money while maintaining a close link to the United Kingdom. The island's government, through the Isle of Man Treasury, issued its own distinct banknotes and coins, known as Manx pounds. These notes, featuring local landmarks and historical figures, were legal tender on the island but, crucially, were not automatically accepted elsewhere. Their value was pegged at par with sterling, meaning one Manx pound equaled one pound sterling, a relationship underpinned by the island's substantial reserves of UK currency and gilts held in its Currency Fund.

This system presented a practical duality for residents and businesses. While Manx currency circulated locally, UK sterling notes and coins were also universally accepted on the island, creating a de facto dual circulation. However, the reverse was not true; Manx notes were often refused by businesses in the UK, requiring travelers to exchange them at banks. This occasionally caused minor inconvenience but was generally accepted as a feature of the island's semi-independent status. The stability of the peg was never in serious doubt, as the Isle of Man's economy was robust and its fiscal reserves were strong, ensuring full confidence in the currency's parity.

The year 1991 fell within a period of monetary stability for the island, following the significant modernization of its coinage in the 1970s and 1980s. There were no major currency crises or reforms that year; instead, the situation reflected a settled and functional system. The key theme was one of managed dependency: the Isle of Man exercised its right to a symbolic national currency, while its economic reality remained firmly anchored to the British sterling zone, a arrangement that balanced political identity with economic pragmatism.

This system presented a practical duality for residents and businesses. While Manx currency circulated locally, UK sterling notes and coins were also universally accepted on the island, creating a de facto dual circulation. However, the reverse was not true; Manx notes were often refused by businesses in the UK, requiring travelers to exchange them at banks. This occasionally caused minor inconvenience but was generally accepted as a feature of the island's semi-independent status. The stability of the peg was never in serious doubt, as the Isle of Man's economy was robust and its fiscal reserves were strong, ensuring full confidence in the currency's parity.

The year 1991 fell within a period of monetary stability for the island, following the significant modernization of its coinage in the 1970s and 1980s. There were no major currency crises or reforms that year; instead, the situation reflected a settled and functional system. The key theme was one of managed dependency: the Isle of Man exercised its right to a symbolic national currency, while its economic reality remained firmly anchored to the British sterling zone, a arrangement that balanced political identity with economic pragmatism.

✨ Legendary