10 cents – South Africa

Add to wishlist

South Africa

Context

Year: 2024

Issuer: South Africa

Issuing organization: South African Reserve Bank

Period:

(since 1961)

Currency:

(since 1961)

Material

References

KM: #

Numista: #437958

Value

Exchange value: 0.10 ZAR

Bullion value: $517.18

Inflation-adjusted value: 0.11 ZAR

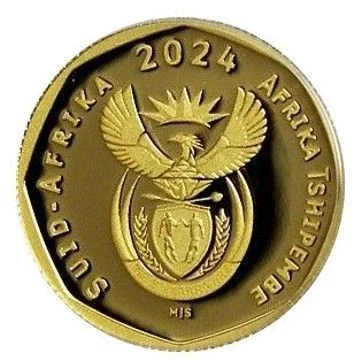

Obverse

Description:

Coat of arms with date, flanked by "South Africa" in Afrikaans and Venda.

Inscription:

2024

MJS

SUID-AFRIKA AFRIKA TSHIPEMBE

MJS

SUID-AFRIKA AFRIKA TSHIPEMBE

Translation:

SOUTH AFRICA AFRICA TSHIPEMBE

Script: Latin

Engraver: Thinus Scheepers

Reverse

Description:

A Cape honey bee in flight over the veld.

Inscription:

Au 999.9 1/10 oz

SDN

10c

SDN

10c

Script: Latin

Engraver: Thinus Scheepers

Designer: Sujay Sanan

Edge

Legend:

SARB R5 SARB R5 SARB R5 SARB R5 SARB R5 SARB R5 SARB R5 SARB R5 SARB R5 SARB R5

Categories

| Animal> Insect |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| South African Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2024 | — | — | Proof |

Historical background

In 2024, South Africa's currency, the rand, continues to face significant volatility and pressure, primarily driven by a combination of domestic structural challenges and global financial currents. The persistent issues of severe load-shedding (rolling blackouts), logistical bottlenecks at key state-owned ports and railways, and high levels of public debt have eroded investor confidence and constrained economic growth. These longstanding domestic headwinds are compounded by a precarious fiscal outlook, with concerns over the sustainability of government spending and the potential for further credit rating downgrades.

Externally, the rand remains highly sensitive to global risk sentiment and U.S. monetary policy. As a liquid emerging market currency, it weakened considerably through 2023 and into 2024 amid a "higher-for-longer" interest rate environment in advanced economies, which diverts investment away from riskier assets. Furthermore, geopolitical tensions and fluctuating commodity prices—despite South Africa's mineral exports—add layers of uncertainty. The currency's value is thus often a barometer of both international market dynamics and the perceived pace of domestic reforms.

Looking ahead, the trajectory of the rand in 2024 hinges critically on the government's ability to implement tangible reforms to stabilize energy supply, fix transport logistics, and curb fiscal deficits. Upcoming national elections also introduce a degree of political uncertainty that markets are closely monitoring. While a weaker rand benefits certain export sectors, it exacerbates imported inflation and living costs for South Africans, keeping the South African Reserve Bank in a difficult position as it balances growth concerns against its inflation-targeting mandate. The currency's stability, therefore, remains inextricably linked to concrete progress on the country's structural reforms.

Externally, the rand remains highly sensitive to global risk sentiment and U.S. monetary policy. As a liquid emerging market currency, it weakened considerably through 2023 and into 2024 amid a "higher-for-longer" interest rate environment in advanced economies, which diverts investment away from riskier assets. Furthermore, geopolitical tensions and fluctuating commodity prices—despite South Africa's mineral exports—add layers of uncertainty. The currency's value is thus often a barometer of both international market dynamics and the perceived pace of domestic reforms.

Looking ahead, the trajectory of the rand in 2024 hinges critically on the government's ability to implement tangible reforms to stabilize energy supply, fix transport logistics, and curb fiscal deficits. Upcoming national elections also introduce a degree of political uncertainty that markets are closely monitoring. While a weaker rand benefits certain export sectors, it exacerbates imported inflation and living costs for South Africans, keeping the South African Reserve Bank in a difficult position as it balances growth concerns against its inflation-targeting mandate. The currency's stability, therefore, remains inextricably linked to concrete progress on the country's structural reforms.

✨ Legendary