30000 forint (Executions of Lajos Batthyány and the 13 Martyrs of Arad) – Hungary

Add to wishlist

Non-circulating coins

Commemoration: 175th anniversary of the executions of Lajos Batthyány and the 13 Martyrs of Arad

Hungary

Context

Year: 2024

Issuer: Hungary

Issuing organization: Magyar Pénzverő

Period:

(since 1989)

Currency:

(since 1946)

Total mintage: 6,000

Material

References

Numista: #436434

Value

Exchange value: 30000 HUF

Bullion value: $177.64

Inflation-adjusted value: 31788.00 HUF

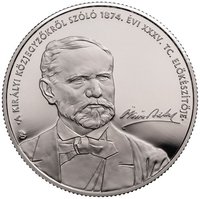

Obverse

Inscription:

MAGYARORSZÁG

30000 FORINT

BP.

Batthyány Lajos

30000 FORINT

BP.

Batthyány Lajos

Translation:

HUNGARY

30000 FORINT

BUDA

Lajos Batthyány

30000 FORINT

BUDA

Lajos Batthyány

Scripts: Latin, Latin (cursive)

Language: Hungarian

Designer: István Kósa

Reverse

Inscription:

ARADI VÉRTANÚK

1849

DESSEWFFY

ARISZTID

LÁZÁR

VILMOS

SCHWEIDEL

JÓZSEF

KISS

ERNŐ

POELTENBERG

ERNŐ

TÖRÖK

IGNÁC

LÁHNER

GYÖRGY

KNEZIĆ

KÁROLY

NAGYSÁNDOR

JÓZSEF

LEININGEN-WESTERBURG

KÁROLY

AULICH

LAJOS

DAMJANICH

JÁNOS

VÉCSEY

KÁROLY

2024

Ki

1849

DESSEWFFY

ARISZTID

LÁZÁR

VILMOS

SCHWEIDEL

JÓZSEF

KISS

ERNŐ

POELTENBERG

ERNŐ

TÖRÖK

IGNÁC

LÁHNER

GYÖRGY

KNEZIĆ

KÁROLY

NAGYSÁNDOR

JÓZSEF

LEININGEN-WESTERBURG

KÁROLY

AULICH

LAJOS

DAMJANICH

JÁNOS

VÉCSEY

KÁROLY

2024

Ki

Translation:

Martyrs of Arad

1849

Arisztid Dessewffy

Vilmos Lázár

József Schweidel

Ernő Kiss

Ernő Poeltenberg

Ignác Török

György Láhner

Károly Knezić

József Nagysándor

Károly Leiningen-Westerburg

Lajos Aulich

János Damjanich

Károly Vécsey

2024

Who

1849

Arisztid Dessewffy

Vilmos Lázár

József Schweidel

Ernő Kiss

Ernő Poeltenberg

Ignác Török

György Láhner

Károly Knezić

József Nagysándor

Károly Leiningen-Westerburg

Lajos Aulich

János Damjanich

Károly Vécsey

2024

Who

Script: Latin

Language: Hungarian

Designer: István Kósa

Edge

Reeded

Categories

| Event> Death anniversary |

Mints

| Name | Mark |

|---|---|

| Hungarian mint | BP. |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2024 | BP. | 6,000 | Proof |

Historical background

In 2024, Hungary's currency situation remains defined by the persistent weakness of the Hungarian Forint (HUF) against major currencies like the Euro and US Dollar. The primary pressure stems from a significant interest rate differential, as the National Bank of Hungary (MNB) has executed one of the EU's most aggressive monetary easing cycles. Starting in late 2023, the MNB rapidly cut its base rate from 13% to 7.75% by mid-2024 to stimulate a stagnant economy, despite inflation remaining above the central bank's target. This created a wide gap with higher interest rates in the Eurozone and US, reducing the yield appeal of forint-denominated assets and leading to sustained selling pressure.

This monetary policy stance exists against a backdrop of lingering structural concerns. Hungary's economy continues to grapple with high budget and current account deficits, which have eroded investor confidence. Furthermore, the prolonged delay in accessing billions in frozen EU recovery funds due to rule-of-law concerns has deprived the country of a key source of foreign currency and a credibility anchor. While the forint has experienced periods of stabilization, often following verbal interventions or hints of a slower pace of cuts from the MNB, these recoveries have proven fragile and short-lived.

Consequently, the forint's volatility remains a central challenge for policymakers and businesses. A weak currency complicates the MNB's inflation fight by making imports more expensive, yet a stronger forint could further hinder economic growth. The government and central bank are therefore walking a tightrope, attempting to balance growth stimulation with currency and price stability. The outlook for the remainder of 2024 hinges on the pace of further MNB rate cuts, the potential unlocking of EU funds, and global risk sentiment, with the currency likely to remain sensitive to both domestic policy signals and international market shifts.

This monetary policy stance exists against a backdrop of lingering structural concerns. Hungary's economy continues to grapple with high budget and current account deficits, which have eroded investor confidence. Furthermore, the prolonged delay in accessing billions in frozen EU recovery funds due to rule-of-law concerns has deprived the country of a key source of foreign currency and a credibility anchor. While the forint has experienced periods of stabilization, often following verbal interventions or hints of a slower pace of cuts from the MNB, these recoveries have proven fragile and short-lived.

Consequently, the forint's volatility remains a central challenge for policymakers and businesses. A weak currency complicates the MNB's inflation fight by making imports more expensive, yet a stronger forint could further hinder economic growth. The government and central bank are therefore walking a tightrope, attempting to balance growth stimulation with currency and price stability. The outlook for the remainder of 2024 hinges on the pace of further MNB rate cuts, the potential unlocking of EU funds, and global risk sentiment, with the currency likely to remain sensitive to both domestic policy signals and international market shifts.

💎 Extremely Rare