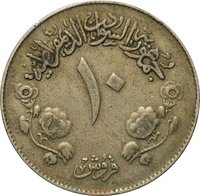

5 piastres (Revolution) – Sudan

Add to wishlist

Circulating commemorative coins

Commemoration: 2nd Anniversary of Revolution

Sudan

Context

Year: 1971

Islamic (Hijri) Year:: 1391

Issuer: Sudan

Period:

(1969—1985)

Currency:

(1956—1992)

Demonetization: 8 June 1992

Total mintage: 500,000

Material

Diameter: 23.5 mm

Weight: 5 g

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #40903

Value

Exchange value: 0.05 SDP

Obverse

Reverse

Edge

Reeded

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1971 | — | 500,000 |

Historical background

In 1971, Sudan's currency situation was intrinsically linked to the nation's post-independence economic ambitions and political turbulence. The Sudanese pound (SDG), introduced in 1956 to replace the Egyptian pound, was pegged to sterling and managed by the Currency Board. However, the government of President Gaafar Nimeiry, who came to power in a 1969 coup, sought greater economic sovereignty and control over monetary policy to fund ambitious development projects. This led to the establishment of the Bank of Sudan in February 1960, but by 1971, the underlying pressures of nationalization policies and significant public spending began to strain the currency's stability.

The year itself was marked by a profound political crisis that directly impacted economic confidence. In July 1971, a brief but intense communist coup attempt against Nimeiry was crushed, leading to a severe crackdown. This instability shook investor confidence and exacerbated existing economic weaknesses, including a growing budget deficit and inflationary pressures. While a major devaluation would not occur until 1978, the events of 1971 highlighted the vulnerability of the currency to political shocks and unsustainable fiscal policies, setting the stage for future economic challenges.

Consequently, the currency situation in 1971 was one of underlying fragility masked by a fixed exchange rate. The state-driven economic model, combined with the political fallout from the failed coup, increased reliance on deficit financing and sowed the seeds for the inflation and balance of payments problems that would escalate later in the decade. The period thus represents a critical juncture where political decisions began to directly undermine the stability of the Sudanese pound, moving the country away from the relative stability of the Currency Board era toward a more volatile and managed monetary environment.

The year itself was marked by a profound political crisis that directly impacted economic confidence. In July 1971, a brief but intense communist coup attempt against Nimeiry was crushed, leading to a severe crackdown. This instability shook investor confidence and exacerbated existing economic weaknesses, including a growing budget deficit and inflationary pressures. While a major devaluation would not occur until 1978, the events of 1971 highlighted the vulnerability of the currency to political shocks and unsustainable fiscal policies, setting the stage for future economic challenges.

Consequently, the currency situation in 1971 was one of underlying fragility masked by a fixed exchange rate. The state-driven economic model, combined with the political fallout from the failed coup, increased reliance on deficit financing and sowed the seeds for the inflation and balance of payments problems that would escalate later in the decade. The period thus represents a critical juncture where political decisions began to directly undermine the stability of the Sudanese pound, moving the country away from the relative stability of the Currency Board era toward a more volatile and managed monetary environment.

⭐ Somewhat Rare