2½ azadi – Iran

Add to wishlist

Iran

Context

Year: 2008

Iranian - Persian Year:: 1387

Issuer: Iran

Issuing organization: Central Bank of the Islamic Republic of Iran

Period:

(since 1979)

Material

References

Numista: #403131

Value

Bullion value: $2774.71

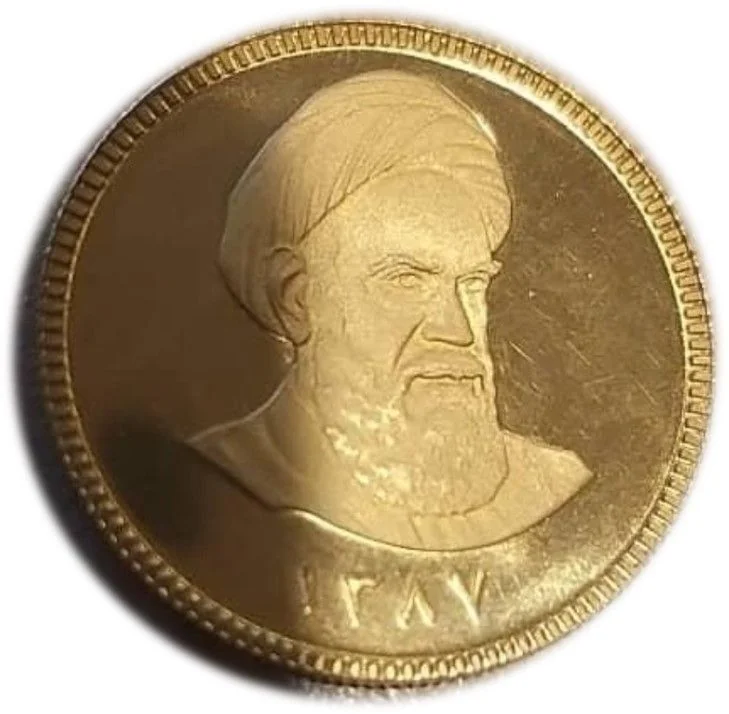

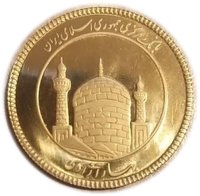

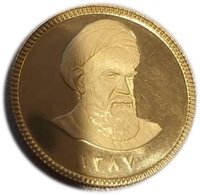

Obverse

Description:

Mosque.

Inscription:

بانک مرکزی جمهوری اسلامی ایران

بهار آزادی

بهار آزادی

Translation:

Central Bank of the Islamic Republic of Iran

The Spring of Freedom

The Spring of Freedom

Script: Persian (nastaliq)

Language: Persian

Reverse

Edge

Reeded

Categories

| Person> Politician |

Mints

| Name | Mark |

|---|---|

| Tehran | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2008 | — | — |

Historical background

In 2008, Iran's currency situation was characterized by mounting external pressures and significant domestic economic vulnerabilities. The year began with the Iranian rial (IRR) under a managed float, but it faced severe downward pressure due to a combination of international sanctions—primarily over the nuclear program—and a dramatic fall in global oil prices in the latter half of the year. As Iran's economy is heavily dependent on hydrocarbon exports, the plunge from over $140 per barrel to near $30 by year's end drastically reduced government revenue and foreign exchange reserves, creating a major balance of payments crisis.

Domestically, these external shocks exposed profound structural weaknesses, including high inflation, estimated at around 25%, and excessive liquidity growth fueled by expansive government spending during the earlier oil boom. President Mahmoud Ahmadinejad's administration, reluctant to adjust official subsidy and spending policies, maintained an artificially strong official exchange rate, which diverged sharply from the rate in the growing black market. This multi-tiered exchange rate system, with the Central Bank of Iran (CBI) prioritizing imports of essential goods at a subsidized rate, led to widespread rent-seeking, corruption, and a critical shortage of hard currency for other businesses.

Consequently, by the close of 2008, Iran was grappling with a severe currency overvaluation and a growing gap between the official rate (around 9,430 rials to the US dollar) and the unofficial market rate, which had begun its long-term depreciation. The situation strained the CBI's ability to defend the rial and marked the beginning of a protracted period of currency instability, setting the stage for more severe economic crises and a contentious move towards subsidy reforms in the following years. The events of 2008 fundamentally undermined confidence in the rial and highlighted the economy's acute sensitivity to both geopolitical isolation and volatile oil markets.

Domestically, these external shocks exposed profound structural weaknesses, including high inflation, estimated at around 25%, and excessive liquidity growth fueled by expansive government spending during the earlier oil boom. President Mahmoud Ahmadinejad's administration, reluctant to adjust official subsidy and spending policies, maintained an artificially strong official exchange rate, which diverged sharply from the rate in the growing black market. This multi-tiered exchange rate system, with the Central Bank of Iran (CBI) prioritizing imports of essential goods at a subsidized rate, led to widespread rent-seeking, corruption, and a critical shortage of hard currency for other businesses.

Consequently, by the close of 2008, Iran was grappling with a severe currency overvaluation and a growing gap between the official rate (around 9,430 rials to the US dollar) and the unofficial market rate, which had begun its long-term depreciation. The situation strained the CBI's ability to defend the rial and marked the beginning of a protracted period of currency instability, setting the stage for more severe economic crises and a contentious move towards subsidy reforms in the following years. The events of 2008 fundamentally undermined confidence in the rial and highlighted the economy's acute sensitivity to both geopolitical isolation and volatile oil markets.

✨ Legendary