½ Dollar – United States

Non-circulating coins

Commemoration: Greatest Generation

United States

Context

Year: 2024

Issuer: United States

Period:

(since 1776)

Currency:

(since 1785)

Subdivision: ½ Dollar = 50 Cents

Material

References

KM: #Click to copy to clipboard794

Numista: #394414

Value

Exchange value: ½ USD = $0.50

Inflation-adjusted value: 0.53 USD

Obverse

Description:

The obverse reimagines the WWII Victory Medal, depicting Liberation holding a broken sword to symbolize the war's end.

Inscription:

LIBERTY

IN GOD

WE TRUST

WORLD WAR

II

2024

WE ANSWERED THE CALL

IN GOD

WE TRUST

WORLD WAR

II

2024

WE ANSWERED THE CALL

Script: Latin

Engraver: Craig Campbell

Designer: Elana Hagler

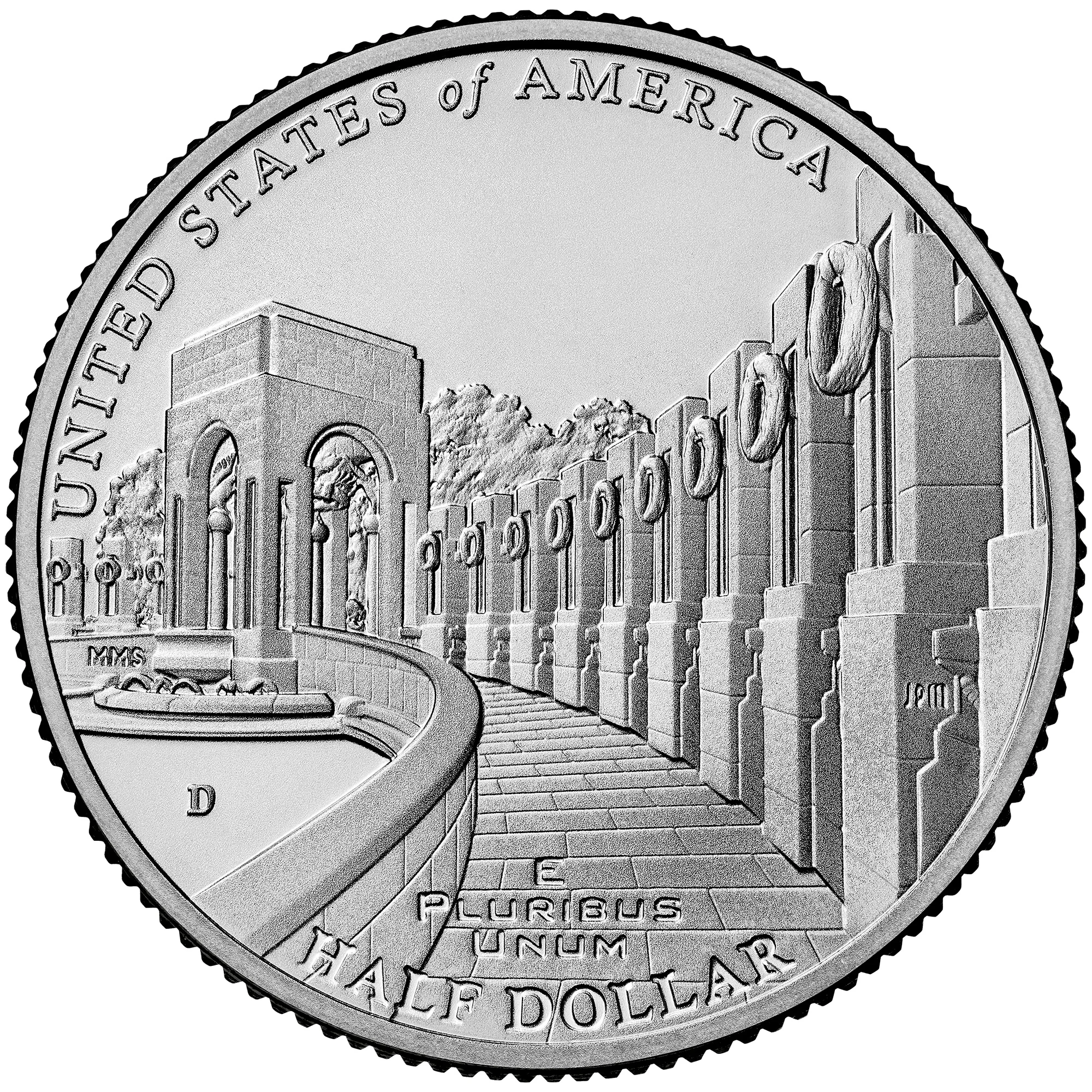

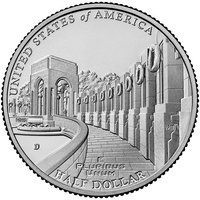

Reverse

Description:

The reverse (tails) shows the WWII Memorial as seen from the ascending ramp toward a tower.

Inscription:

UNITED STATES OF AMERICA

E PLURIBUS UNUM

HALF DOLLAR

E PLURIBUS UNUM

HALF DOLLAR

Translation:

UNITED STATES OF AMERICA

OUT OF MANY, ONE

HALF DOLLAR

OUT OF MANY, ONE

HALF DOLLAR

Script: Latin

Engraver: John McGraw

Designer: Matt Swaim

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| United States Mint of Denver | D |

| United States Mint of San Francisco | S |

Historical background

The United States enters 2024 navigating a complex currency landscape defined by the Federal Reserve's ongoing battle against inflation. After aggressive interest rate hikes throughout 2022 and 2023, inflation has moderated from its four-decade peak but remains stubbornly above the Fed's 2% target. This has led to a "higher-for-longer" interest rate posture, strengthening the U.S. dollar (USD) through much of the period. A strong dollar has global repercussions, making imports cheaper for Americans but increasing debt burdens for foreign nations and companies that borrow in USD, while also weighing on the earnings of U.S. multinational corporations.

Domestically, the primary focus remains on the dollar's purchasing power and its impact on consumers. While wage growth has recently outpaced price increases, providing some relief, the cumulative effect of high inflation since 2021 continues to strain household budgets, particularly for essentials like housing, food, and transportation. This economic pressure is a central issue in the 2024 presidential election, with debates centering on fiscal policy, government spending, and the appropriate timeline for potential rate cuts by the Fed to avoid triggering a recession.

Looking forward, the dollar's trajectory hinges on the Fed's policy decisions amid competing risks. Markets are closely watching economic data for signals that could prompt a shift toward rate cuts, which would likely weaken the dollar. However, persistent inflation or unexpected economic strength could delay such easing. Furthermore, the U.S. dollar's status as the world's dominant reserve currency remains unchallenged in the near term, bolstered by geopolitical instability and the lack of a credible alternative, but long-term concerns about the nation's rising debt levels and the use of the dollar as a geopolitical tool continue to simmer in the background.

Domestically, the primary focus remains on the dollar's purchasing power and its impact on consumers. While wage growth has recently outpaced price increases, providing some relief, the cumulative effect of high inflation since 2021 continues to strain household budgets, particularly for essentials like housing, food, and transportation. This economic pressure is a central issue in the 2024 presidential election, with debates centering on fiscal policy, government spending, and the appropriate timeline for potential rate cuts by the Fed to avoid triggering a recession.

Looking forward, the dollar's trajectory hinges on the Fed's policy decisions amid competing risks. Markets are closely watching economic data for signals that could prompt a shift toward rate cuts, which would likely weaken the dollar. However, persistent inflation or unexpected economic strength could delay such easing. Furthermore, the U.S. dollar's status as the world's dominant reserve currency remains unchallenged in the near term, bolstered by geopolitical instability and the lack of a credible alternative, but long-term concerns about the nation's rising debt levels and the use of the dollar as a geopolitical tool continue to simmer in the background.

💎 Very Rare