20000 Bolivars (Port of Maracay) – Venezuela

Non-circulating coins

Commemoration: 300th Anniversary of the Port of Maracay

Venezuela

Context

Year: 2001

Issuer: Venezuela

Period:

(since 1999)

Currency:

(1879—2007)

Demonetized: Yes

Total mintage: 1,000

Material

References

Y: #Click to copy to clipboardA85

Numista: #37255

Value

Exchange value: 20000 VEB

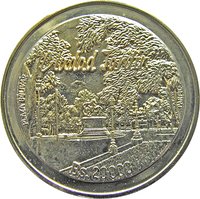

Obverse

Description:

Venezuela map, Aragua state.

Inscription:

Maracay

300 Años

5 de Marzo 1701

REPÚBLICA BOLIVARIANA DE VENEZUELA

300 Años

5 de Marzo 1701

REPÚBLICA BOLIVARIANA DE VENEZUELA

Translation:

Maracay

300 Years

March 5, 1701

Bolivarian Republic of Venezuela

300 Years

March 5, 1701

Bolivarian Republic of Venezuela

Script: Latin

Language: Spanish

Designer: Rita Panfili

Reverse

Description:

Plaza Bolívar, Maracay.

Inscription:

Plaza Bolivar

Ciudad Jardin

Bs. 20000

PANFILI

Ciudad Jardin

Bs. 20000

PANFILI

Script: Latin

Designer: Rita Panfili

Edge

Grained

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2001 | — | 1,000 |

Historical background

In 2001, Venezuela's currency situation was characterized by relative stability on the surface, but growing underlying pressures that foreshadowed the profound economic crises to come. The country operated under a fixed exchange rate regime, with the bolivar pegged at 717 to the US dollar under a system known as the "Bandas Cambiarias" (exchange bands). This peg, established in 1996, had successfully tamed hyperinflation and provided a decade of monetary stability, but it was increasingly maintained through heavy central bank intervention and the sustained inflow of dollars from high oil prices.

However, this stability was fragile and masked significant vulnerabilities. The economy was overly dependent on oil revenues, which accounted for roughly 80% of export earnings and half of government revenue. A sharp decline in oil prices in 1998 had exposed this weakness, leading to a recession. Although prices recovered by 2001, the government of President Hugo Chávez, who took office in 1999, was financing expansive social programs and facing capital flight due to political uncertainty following his election and the passage of a new constitution. These factors put persistent downward pressure on international reserves, which were being depleted to defend the fixed parity.

Consequently, 2001 marked the beginning of the end for the bolivar's stability. Market skepticism about the sustainability of the peg grew, leading to a widening gap between the official rate and an emerging black-market rate. In response, the government took initial steps toward stricter currency controls, including a transaction tax on foreign currency purchases. These measures, combined with growing fiscal imbalances and political polarization, set the stage for the severe exchange controls that would be fully implemented in 2003, ending the era of a freely convertible bolivar and initiating a long period of complex, multi-tiered currency systems.

However, this stability was fragile and masked significant vulnerabilities. The economy was overly dependent on oil revenues, which accounted for roughly 80% of export earnings and half of government revenue. A sharp decline in oil prices in 1998 had exposed this weakness, leading to a recession. Although prices recovered by 2001, the government of President Hugo Chávez, who took office in 1999, was financing expansive social programs and facing capital flight due to political uncertainty following his election and the passage of a new constitution. These factors put persistent downward pressure on international reserves, which were being depleted to defend the fixed parity.

Consequently, 2001 marked the beginning of the end for the bolivar's stability. Market skepticism about the sustainability of the peg grew, leading to a widening gap between the official rate and an emerging black-market rate. In response, the government took initial steps toward stricter currency controls, including a transaction tax on foreign currency purchases. These measures, combined with growing fiscal imbalances and political polarization, set the stage for the severe exchange controls that would be fully implemented in 2003, ending the era of a freely convertible bolivar and initiating a long period of complex, multi-tiered currency systems.

✨ Legendary