50 centavos (General San Martin's Death) – Argentina

Add to wishlist

Non-circulating coins

Commemoration: 150th Anniversary of General San Martin's Death

Argentina

Context

Material

Diameter: 25.2 mm

Weight: 5.8 g

Thickness: 1.8 mm

Shape: Round

Composition: Aluminium bronze

Magnetic: No

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #365227

Value

Exchange value: 0.50 ARS

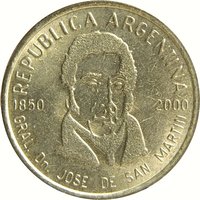

Obverse

Description:

Bust of General San Martín, front view.

Inscription:

REPUBLICA ARGENTINA

1850 2000

GRAL. Dn. JOSE DE SAN MARTIN

1850 2000

GRAL. Dn. JOSE DE SAN MARTIN

Translation:

Argentine Republic

1850 2000

General Don Jose de San Martin

1850 2000

General Don Jose de San Martin

Script: Latin

Language: Spanish

Engraver: Carlos Pedro Rodríguez Dufour

Reverse

Description:

San Carlos Convent's bell gable, with the monogram "VIVA LA PATRIA" beside the bell. Date and face value.

Inscription:

LA PATRIA AL LIBERTADOR 2000

50

CTVS.

50

CTVS.

Translation:

The Homeland to the Liberator 2000

50

Centavos.

50

Centavos.

Script: Latin

Language: Spanish

Engraver: Carlos Pedro Rodríguez Dufour

Edge

Plain

Categories

| Event> Death anniversary |

| Person> Politician |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2000 | — | 5,000 |

Historical background

Argentina entered the year 2000 trapped in the rigid constraints of its Convertibility Plan, established in 1991 to halt hyperinflation. This law pegged the Argentine peso at a one-to-one parity with the U.S. dollar, making the Central Bank effectively a currency board that could only issue new pesos if backed by an equal amount of dollar reserves. Initially successful in stabilizing prices and attracting foreign investment, the system created a profound loss of monetary sovereignty. The government could no longer print money to finance deficits, and the peso's value was entirely dependent on the maintenance of full foreign exchange reserves.

However, by 2000, the structural flaws of convertibility had become critical. A series of external shocks, including the 1997 Asian Financial Crisis and the 1999 Brazilian devaluation, severely damaged Argentina's export competitiveness. Stuck with an overvalued peso, the economy sank into a deep and prolonged recession beginning in 1998. Tax revenues plummeted while public debt, much of it denominated in dollars, ballooned. The government resorted to severe austerity and borrowed heavily from the International Monetary Fund (IMF), but confidence evaporated. A growing perception that the dollar peg was unsustainable led to capital flight, steadily draining the very reserves that backed the currency.

Thus, the currency situation in 2000 was one of acute vulnerability and impending crisis. The fixed exchange rate, once a pillar of stability, had become a straitjacket that prevented economic adjustment and fueled a vicious cycle of recession, deflation, and rising debt burdens. Despite massive IMF bailouts, the drain on reserves continued unabated, setting the stage for the catastrophic collapse of convertibility that would occur at the end of 2001.

However, by 2000, the structural flaws of convertibility had become critical. A series of external shocks, including the 1997 Asian Financial Crisis and the 1999 Brazilian devaluation, severely damaged Argentina's export competitiveness. Stuck with an overvalued peso, the economy sank into a deep and prolonged recession beginning in 1998. Tax revenues plummeted while public debt, much of it denominated in dollars, ballooned. The government resorted to severe austerity and borrowed heavily from the International Monetary Fund (IMF), but confidence evaporated. A growing perception that the dollar peg was unsustainable led to capital flight, steadily draining the very reserves that backed the currency.

Thus, the currency situation in 2000 was one of acute vulnerability and impending crisis. The fixed exchange rate, once a pillar of stability, had become a straitjacket that prevented economic adjustment and fueled a vicious cycle of recession, deflation, and rising debt burdens. Despite massive IMF bailouts, the drain on reserves continued unabated, setting the stage for the catastrophic collapse of convertibility that would occur at the end of 2001.

⭐ Rare