Obverse

Description:

Mexican coat of arms with a golden eagle on a cactus, eating a snake, flanked by oak and laurel branches. "Estados Unidos Mexicanos" arches above; denomination and year are below.

Inscription:

ESTADOS UNIDOS MEXICANOS

·UN PESO 1963·

·UN PESO 1963·

Translation:

UNITED MEXICAN STATES

·ONE PESO 1963·

·ONE PESO 1963·

Script: Latin

Language: Spanish

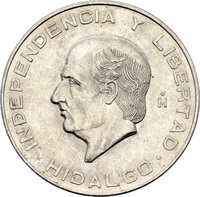

Reverse

Description:

Portrait of Jose Morelos facing right, mintmark Mo left of head.

Inscription:

O

M

M

Script: Latin

Edge

Plain with lettering

Legend:

INDEPENDENCIA Y LIBERTAD

Translation:

Independence and Liberty

Language: Spanish

Categories

| Animal> Bird> Eagle |

| Animal> Reptile |

| Event> Independence |

| Person> Religious figure |

Mints

| Name | Mark |

|---|---|

| Mexican Mint | (Mo) |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1957 | Mo | 28,273,000 | ||

| 1958 | Mo | 41,899,000 | ||

| 1959 | Mo | 27,369,000 | ||

| 1960 | Mo | 26,259,000 | ||

| 1961 | Mo | 52,601,000 | ||

| 1962 | Mo | 61,094,000 | ||

| 1963 | Mo | 26,394,000 | ||

| 1964 | Mo | 15,615,000 | ||

| 1965 | Mo | 5,004,000 | ||

| 1966 | Mo | 30,998,000 | ||

| 1967 | Mo | 9,308,000 |

Historical background

In 1957, Mexico's currency situation was characterized by a period of relative stability under the Bretton Woods system, but with underlying pressures that foreshadowed future devaluations. The Mexican peso was pegged to the U.S. dollar at a fixed rate of 12.50 pesos per dollar, a parity established in 1954 following a significant devaluation from the previous rate of 8.65. This "devaluation of 1954," orchestrated by the administration of President Adolfo Ruiz Cortines, was a corrective measure to address a chronic balance of payments deficit, restore international reserves, and curb inflation. By 1957, this adjustment had largely achieved its goals, fostering a climate of renewed confidence and a period known as "Desarrollo Estabilizador" (Stabilizing Development).

This stability, however, was maintained through strict fiscal and monetary discipline, coupled with capital controls. The government, led by the dominant Institutional Revolutionary Party (PRI), prioritized low inflation and a stable exchange rate as the cornerstones of economic policy. This environment successfully attracted foreign investment and supported steady industrialization. Nevertheless, the fixed exchange rate began to create distortions. As the economy grew, the peso gradually became overvalued, making Mexican exports more expensive and imports cheaper, which over time threatened the country's trade balance and industrial competitiveness.

Consequently, while 1957 itself was not a year of currency crisis, it represented the calm before the storm. The rigid peg, while successful in the short term, masked growing structural imbalances. The policies that provided stability also discouraged necessary adjustments, leading to a reliance on foreign borrowing and setting the stage for the severe balance of payments problems and the eventual devaluation of the peso in 1976, which marked the end of the long era of fixed parity and "Desarrollo Estabilizador."

This stability, however, was maintained through strict fiscal and monetary discipline, coupled with capital controls. The government, led by the dominant Institutional Revolutionary Party (PRI), prioritized low inflation and a stable exchange rate as the cornerstones of economic policy. This environment successfully attracted foreign investment and supported steady industrialization. Nevertheless, the fixed exchange rate began to create distortions. As the economy grew, the peso gradually became overvalued, making Mexican exports more expensive and imports cheaper, which over time threatened the country's trade balance and industrial competitiveness.

Consequently, while 1957 itself was not a year of currency crisis, it represented the calm before the storm. The rigid peg, while successful in the short term, masked growing structural imbalances. The policies that provided stability also discouraged necessary adjustments, leading to a reliance on foreign borrowing and setting the stage for the severe balance of payments problems and the eventual devaluation of the peso in 1976, which marked the end of the long era of fixed parity and "Desarrollo Estabilizador."

🌱 Very Common