1 Ringgit (Independence) – Malaysia

Circulating commemorative coins

Commemoration: 30th Anniversary of Independence

Malaysia

Obverse

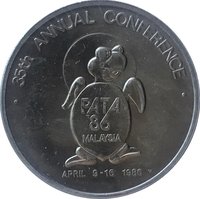

Reverse

Edge

Reeded

Categories

| Animal> Bird |

| Event> Independence |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1987 | — | 1,000,000 | ||

| 1987 | — | 20,000 | Proof |

Historical background

In 1987, Malaysia's currency situation was dominated by the aftermath of the Plaza Accord of 1985, a major international agreement that led to a significant realignment of global currencies, particularly a sharp appreciation of the Japanese yen and German mark against the US dollar. As the Malaysian Ringgit (MYR) was informally pegged to a basket of currencies heavily weighted by the US dollar, this global shift caused the Ringgit to depreciate considerably. This depreciation, while boosting export competitiveness for Malaysia's commodity-driven economy (especially palm oil and rubber), also increased the cost of servicing the nation's substantial foreign debt, which was predominantly denominated in non-US dollar currencies like the yen.

Domestically, the currency depreciation occurred against a backdrop of severe economic recession, known locally as the 1985-86 recession, triggered by a collapse in global commodity prices. Although recovery was beginning in 1987, the financial system remained fragile. The weakened Ringgit exacerbated concerns over corporate and banking sector stability. In response, Bank Negara Malaysia (the central bank) intervened actively in the foreign exchange market to manage volatility and prevent a disorderly decline, while also tightening monetary policy at times to curb inflationary pressures and support the currency.

The year 1987 was thus a transitional period of cautious stabilization. The government, under Prime Minister Mahathir Mohamad, prioritized economic recovery through export-led growth, which the weaker Ringgit facilitated. However, authorities had to carefully balance this benefit against the risks of imported inflation and financial instability. This precarious balancing act set the stage for the subsequent period, where managing the Ringgit's value and capital flows would become central to Malaysia's economic policy, culminating in the controversial fixed peg implemented a decade later during the Asian Financial Crisis.

Domestically, the currency depreciation occurred against a backdrop of severe economic recession, known locally as the 1985-86 recession, triggered by a collapse in global commodity prices. Although recovery was beginning in 1987, the financial system remained fragile. The weakened Ringgit exacerbated concerns over corporate and banking sector stability. In response, Bank Negara Malaysia (the central bank) intervened actively in the foreign exchange market to manage volatility and prevent a disorderly decline, while also tightening monetary policy at times to curb inflationary pressures and support the currency.

The year 1987 was thus a transitional period of cautious stabilization. The government, under Prime Minister Mahathir Mohamad, prioritized economic recovery through export-led growth, which the weaker Ringgit facilitated. However, authorities had to carefully balance this benefit against the risks of imported inflation and financial instability. This precarious balancing act set the stage for the subsequent period, where managing the Ringgit's value and capital flows would become central to Malaysia's economic policy, culminating in the controversial fixed peg implemented a decade later during the Asian Financial Crisis.

🌟 Uncommon