25 satangs – Thailand

Add to wishlist

Thailand

Context

Year: 1929

Thai Year:: 2472

Issuer: Thailand

Ruler: Phra Pok Klao

Currency:

(since 1897)

Demonetized: Yes

Material

References

Y: #

Numista: #35127

Value

Exchange value: 0.25 THB

Bullion value: $6.18

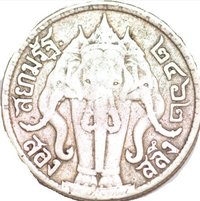

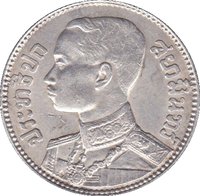

Obverse

Reverse

Edge

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1929 | — | — |

Historical background

In 1929, Thailand, then known as Siam, operated under a unique silver-based currency system that was on the brink of a severe crisis. The nation's monetary standard was the "Baht," defined as a fixed weight of pure silver (15 grams). Unlike many countries which had adopted the gold standard, Siam maintained a silver exchange standard, where the value of its currency was directly tied to the international price of silver. This system had functioned adequately for decades, but it left the kingdom highly vulnerable to global commodity price shocks.

The trigger for crisis came with the collapse of the global silver market in late 1929, a direct consequence of the Great Depression. As major economies contracted, demand for silver plummeted, causing its price to fall dramatically on world markets. Because the Siamese Baht was a physical silver coin, its intrinsic metal value began to drop below its official face value. This situation created a powerful incentive for arbitrage and speculation: individuals could export silver Baht coins, melt them down, and sell the bullion abroad for more than the coins were nominally worth in Siam. This led to a rapid and alarming drain of the nation's silver currency reserves, threatening economic stability.

Faced with this hemorrhage, the government of King Prajadhipok (Rama VII) was forced to take drastic action. In April 1930, it announced the immediate abandonment of the silver standard. The authorities demonetized the old silver Baht and introduced a new, fiduciary currency—notes and coins not redeemable for silver—thereby de-linking the Baht from the volatile commodity market. This decisive move, though necessary, was socially disruptive, causing confusion and loss of public confidence during an already difficult time, and marked a pivotal moment where Siam's currency transitioned from a tangible commodity to a government-managed instrument.

The trigger for crisis came with the collapse of the global silver market in late 1929, a direct consequence of the Great Depression. As major economies contracted, demand for silver plummeted, causing its price to fall dramatically on world markets. Because the Siamese Baht was a physical silver coin, its intrinsic metal value began to drop below its official face value. This situation created a powerful incentive for arbitrage and speculation: individuals could export silver Baht coins, melt them down, and sell the bullion abroad for more than the coins were nominally worth in Siam. This led to a rapid and alarming drain of the nation's silver currency reserves, threatening economic stability.

Faced with this hemorrhage, the government of King Prajadhipok (Rama VII) was forced to take drastic action. In April 1930, it announced the immediate abandonment of the silver standard. The authorities demonetized the old silver Baht and introduced a new, fiduciary currency—notes and coins not redeemable for silver—thereby de-linking the Baht from the volatile commodity market. This decisive move, though necessary, was socially disruptive, causing confusion and loss of public confidence during an already difficult time, and marked a pivotal moment where Siam's currency transitioned from a tangible commodity to a government-managed instrument.

⭐ Somewhat Rare